This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

And so it happened that between 2000-2008 I was the biggest buzz kill at dinner parties. The dinner parties now are filled with self-righteous angel investors bragging about how many deals they are in on. They have marked-up paper gains propped up by an over excited venture capital market that has validated their investments.

We received so much positive feedback from our This Week in Venture Capital show walking through valuation calculations & term sheets that we decided to do a Q&A show this week to address topics that entrepreneurs want to learn about. In fact, far better if you haven’t raised venture capital. This is minutes 8-11.

Assume you have the right factors to get angelinvestment: experienced team, good product-market fit, growth potential, defensibility, and a reasonable shot at a successful exit. This might seem awkward on this site, suggesting that you don’t want angelinvestment. But angelinvestment isn’t for everybody.

Alomar, who led startups through the dotcom bust of 2000 and the Great Recession of 2008, will talk about whether investors are still prioritizing growth over profits, and identify which proof points founding teams must define before their next raise. 3 tips for biotech startups seeking non-dilutive capital to weather the downturn.

This week I sat down with Chris Dixon, co-founder / CEO of Hunch and Partner at Founder Collective in the most recent installment of This Week in Venture Capital. The firm focuses on early stage companies in the Northeast but occasionally invests in California startups. Such that during that time, Chris “learned how to learn.”.

I’m sharing my thought process because perhaps it will nudge some of you to angelinvest too! I consider myself a furiously curious person, and angelinvesting is one of the most rewarding ways I’ve experienced to satisfy this curiosity. THE ORIGIN I was the Founder & CEO of InboxDollars from 2000 to 2019.

I began studying angelinvesting returns about 10 years ago as a result of a problem I couldn’t resolve: The investing world seemed certain that angel investors were rubes. Conventional wisdom dictated that they made reckless investments in very early-stage ventures mostly doomed to fail. So which is it?

Next Wednesday we’ll have Dana Settle of Greycroft Partners, a New York / LA early-stage venture capital fund. We spoke about the changes to an “accredited investor&# proposed by Chris Dodd – This would be bad for angelinvesting. Invidi is based in New York and founded in 2000. Short answer: no.

Hans Severiens winners Tony Shipley, left, of Queen City Angels and Dan Rosen , right, of the Aliance of Angels. The Hans Severiens Award recognizes personal impact on the advancement of angelinvesting globally and highlights the special relationship that angels and entrepreneurs build to innovate, create jobs, and drive the economy.

If they are not achieved within the expected time, the reasons must be analyzed and acted upon to avoid loss of capital beyond plan or expectation. My favorite story of a fast failure was of a technology incubator started in the year 2000 with optimistic money from a number of angelinvestments, including mine.

This is part of a series on building your career in venture capital: Reading list for working in private equity/venture capital , including all of the major online communities, programs, and educational options for people studying VC. How to get a job in venture capital. Syllabus for how to launch, manage, and invest a VC fund.

If they are not achieved within the expected time, the reasons must be analyzed by you and by your board and acted upon to avoid loss of capital beyond plan or expectation. Reduce further expenditures of remaining capital and protect the assets purchased with the original investment.

By: Emily Angold, ACA Marketing Manager As an entrepreneur and seasoned angel investor, Bill Payne understands the critical importance of education to make well-informed decisions that determine the success or failure of a startup. In your opinion, what are the most important takeaways from ACA Angel University’s Valuation Workshop?

By: Dan Rosen, Alliance of Angels To: The Angel Community After publishing my companion piece, “ How Startups Survive the COVID-19 Economic Crisis ,” I have received a number of comments about how this impacts angels and angelinvesting. Here are my rules for Angels during this downturn: Stay in the Game.

If they are not achieved within the expected time, the reasons must be analyzed by you and by your board and acted upon to avoid loss of capital beyond plan or expectation. Reduce further expenditures of remaining capital and protect the assets purchased with the original investment. A personal story of failing fast.

If they are not achieved within the expected time, the reasons must be analyzed by you and by your board and acted upon to avoid loss of capital beyond plan or expectation. Reduce further expenditures of remaining capital and protect the assets purchased with the original investment. A personal story of failing fast.

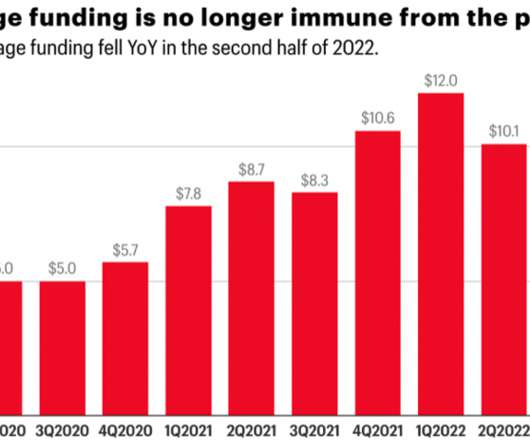

This is Part 2 of a two-part examination of the state of the startup capital market during the past two years. From an investor’s perspective, 2022 witnessed a sudden market reversal from an extreme equity seller’s market to an equity buyer’s market, causing dislocations throughout angel, VC, and startup ecosystems.

It’s a new startup backed by eFounders that wants to bring community-driven, AngelList-style angelinvestments to European startups. The company has built a platform that simplifies the administrative, legal and financial challenges that come with angelinvestments. Money continues to flow into new venture capital funds.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content