This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Many observers of the venturecapital industry have questioned whether its best days are behind it. Looking ahead at the next decade I am excited by what I believe will be viewed as one of the best and most rational investment periods for venturecapital due to seven discrete factors: 1. The Funding Problem.

In this three-part series I will explore the ways that the VentureCapital industry has changed over the past 5 years that I would argue are a direct result of changes in the software industry, not the other way around. So it’s unsurprising that typical “A rounds&# of venturecapital were $5-10 million.

I was on This Week in VentureCapital (TWiVC) again this week with Jason Calacanis. I don’t believe that search is the only answer in 2010 as it was in 2000. mm in Series A; IdealLab ( Bill Gross ), Index Ventures ( Danny Rimer ), Revolution LLC ( Steve Case ), First Round Capital , BetaWorks , Jason Calcanis.

We have previously raised funds in 1996 ($200 million), 2000 ($400 million) and 2008/9 ($200 million). Perhaps the biggest piece of new news is that after 17 years of operations we’ve changed our name from GRP Partners to Upfront Ventures. Well, the venturecapital industry has changed a lot in the past 20 years … and we have too.

We received so much positive feedback from our This Week in VentureCapital show walking through valuation calculations & term sheets that we decided to do a Q&A show this week to address topics that entrepreneurs want to learn about. In fact, far better if you haven’t raised venturecapital. Most are not.

Jersey Shore Ventures anyone?). Until you realize that vetting and helping companies is actually really hard--or did you not notice all the news that venturecapital as an asset class doesn't beat the market. Who wouldn't want in on the next Union Square Ventures or First Round Capital funds? I certainly would!

If you read this blog often you'll know that I'm a huge fan of First Round Capital. One example is that they introduced a program where their founders can pool together shares from their company and exchange them for a small portfolio of other First Round Capital companies. I'm a huge fan of this innovation. and Half.com. and Half.com.

We had a special edition of This Week in VentureCapital this week shooting out of the Next New Networks offices in New York. Our guest was Mo Koyfman of Spark Capital. The Spark Capital website (it’s one of my favorites). Current round: $10mm in Series B by Norwest (lead), Storm Ventures and Adams Capital.

I am so proud and humbled to be able to formally announce that Upfront Ventures has raised its 6th venturecapital fund in the past 21 years. A huge thank you to all of the Limited Partners who have entrusted us with your capital, time and reputations. This brings our combined funds under management to nearly $2 billion.

Back in 2009, I wrote a post called The VentureCapital Math Problem. This 2009 piece from @fredwilson (literally the best in the biz) predicted significant venture industry contraction when in fact the last 10yrs have seen massive expansion. So what did I get wrong in my attempt to solve the venturecapital math problem?

But VC is an “illiquid asset&# so funds didn’t disappear quickly - In 2000/01 the stock market quickly adjusted punishing investors in the NASDAQ and in individual public technology stocks. side note: our last fund at GRP Partners is currently ranked as the 5th best performing fund of the year 2000. Others will, too.

Sam Altman of YC recently pointed out that pulling back during the downturn in 2008 would result in several big misses: In October of 2008, Sequoia Capital—arguably the best-ever in the business—gave the famous “RIP Good Times” presentation (I was there). These sound fundamentals drive the venturecapital market over the long term.

This is a story of one of the risks of venturecapital. But some companies have entrepreneurs that seem talented on paper, are in a space that seems interesting to investors and are able to raise venturecapital early in the company’s existence. True story.) 2 weeks later and we may never have raised any more VC.

We moved into the legal process and final due diligence in January and February of 2000. Our final closure was the first week of March 2000. It quickly became impossible to raise venturecapital. It isn’t even a story about raising venturecapital or M&A. They accepted my argument. Any deal.

Andy Areitio is a partner at the early-stage fund TheVentureCity , a new venture and acceleration model that helps diverse founders achieve global impact. When you’re running your own venture — especially if it’s your first — it’s unlikely you will find the time to deep dive into how venturecapital firms work.

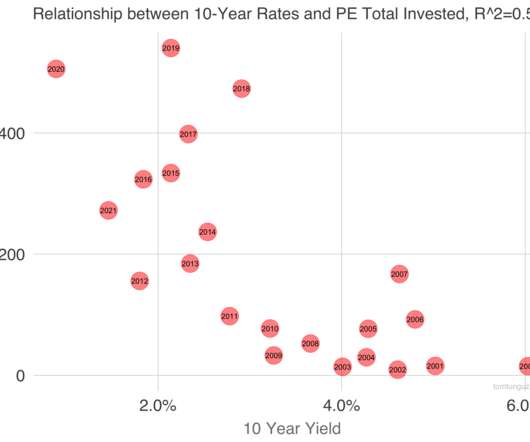

What does it mean for venturecapital and Startupland? Let’s examine the relationship between total venturecapital investment and the 10 year Treasury in some detail. The y-axis tracks enture capital investment by year and the year of the data point resides in the reddish circle.

Amy Cortese published “VentureCapital, Withering & Dying” in the New York Times on Oct 21, 2001. So far this year, 29 venture-backed companies have tried initial offerings, compared with 252 in 2000. Venturecapital funds lost 18.2 Venturecapital funds lost 18.2

These notes graciously provided by Adam Besvinick , who is a summer associate at ff ventures run by the affable John Frankel , who will also be on the show soon. This week I sat down with Chris Dixon, co-founder / CEO of Hunch and Partner at Founder Collective in the most recent installment of This Week in VentureCapital.

Just as an additional disclosure, these are my thoughts, not that of First Round Capital, my employer. The other day, Adeo Ressi wrote in TechCrunch about how we need more venture funds, because. More entrepreneurs get to try out their ideas with smaller amounts of capital, but the bar remains the same to get to the bigger rounds.

Even more interesting is that at GRP Partners (the VC firm where I’m a partner) our two most successful returns from our previous fund [which is ranked as the top performing fund in the country for its 2000 vintage according to Prequin] were both run by women! But then the truth sets in.

This is part of my series on Understanding VentureCapital. It’s also meaningless if they had four $200 million funds and the last one they closed was in 2000. I’m writing this series because if you better understand how VC firms work you can better target which firms make sense for you to speak with.

This is part of my ongoing series on Raising VentureCapital. Not so in venturecapital. My chips were down in late 2000 / early 2001. I often tell people that raising money is worse than getting married. I have to be careful in how that sounds because I love my wife and am happily married. My story briefly.

Next Wednesday we’ll have Dana Settle of Greycroft Partners, a New York / LA early-stage venturecapital fund. 6mm in Series A: Investors: Union Square Ventures (Brad Burnham) (lead), Ron Conway, Chris Dixon, Caterina Fake, Naval Ravikant, Nirav Tolia, Joshua Schachter, Micah Siegel, Bob Pasker – Read more: VentureBeat.

What a pleasure that I got to spend an hour talking with both Om Malik (whom I’ve always respected his views) and Paul Jozefak , a venturecapital partner at Neuhaus Partners in Germany (and formerly the head of Europe for SAP Ventures). Paul discussed his perspective having been at SAP Ventures. 406 Ventures.

This simple and short blog post by the folks at Correlation Ventures contains the key to venturecapital returns – the hit rate. What is important is this chart from the Correlation post: I guess they have a keen eye for correlation at Correlation Ventures. More capital means more businesses get funded.

We raised a seed round of capital in 1999 and our first venturecapital round was the first week of March 2000 (e.g. But this was early 2000 and our US competitors had already closed rounds North of $45 million. We had a $40 million round lined up to close in the Autumn of 2000. We were based in London.

I know that most people who are close to them tend to deny their existence, as we saw in the great housing bubble of 2002-2007 and the dot com bubble of 1997-2000. I guess that makes USV, Spark Capital, Foundry Group, Accel, Benchmark, Revolution (along with several others) pretty happy right now. source: Capital IQ.

The framework of his book has profoundly altered how I think about the technology market and affects how I thought about building my businesses and how I think about investing in venturecapital. In 1999-2000 they weren’t doing enterprise-wide installations at Merrill Lynch, Dell and Cisco. Enter Salesforce.com.

What you’ll see if you watch the video is an unscripted and unfiltered look into how Scott Kupor & I see some of the changes and challenges of the venture industry. Venture is a returns based and I believe has different characteristics. tl;dr version. I don’t totally agree with that view.

I was clueless about startup operations, financing and venturecapital, but I didn’t need to be an economist to realize that most of the companies I worked for lacked solid fundamentals. ” What can the 2000 dot-com crash teach us about the 2022 tech downturn? ‘The macroeconomic market is just noise’.

Coupled with my participating preferred from 1999 and 2000 I had more than $55 million of liquidation preferences. Otherwise, what incentive exists for the VC to put in more capital or to have the founders earn money. Tags: Pitching VCs Start-up Advice VC Industry startup technology vc venturecapital.

I'd say just about everyone in my LinkedIn network , all 2000 of them, are people who I've at least had the equivilant of a 1:1 lunch with. I like to think about who the most influential and accomplished people will be in the NYC innovation community in ten years, because I plan on having a long and productive venturecapital career.

And so it happened that between 2000-2008 I was the biggest buzz kill at dinner parties. They have marked-up paper gains propped up by an over excited venturecapital market that has validated their investments. For venture capitalists this isn’t troubling. It is slowly becoming Florida Condos.

I recently read a blog post by Beezer Clarkson, Managing Director of Sapphire Ventures about why entrepreneurs should care about from whom their VC funds raise their capital. I spent a bunch of time thinking about this position — especially since Beezer is an investor in Upfront Ventures. Beezer did. We lived that first hand.

I never would have paid for music back in 1999 or 2000 when I was sporting my 64mb Creative Nomad, powered completely ilegally by Napster. Tags: First Round CapitalVentureCapital & Technology. Remember when they said that people wouldn't pay for music? Because it was a tremendous pain in the ass.

Deals are getting done with a lot less capital which is creating a healthy debate in the industry. Retail investors were burned in IPOs in 2000, Consumers getting burned by services disappearing) Minutes 31-35. Tags: This Week in VentureCapital. .&# It’s self selecting. Minutes 8 – 10. Minutes 36- 38. o Tuenti.

Lux Capital, known for investing in life science and frontier tech startups, is back in the market to fundraise for its latest vehicle — but this time without a dedicated late-stage entity. The firm was founded in 2000 and has raised $4 billion across nine previous funds. million to the fund. million to the fund.

By now you will likely have read Andy Dunn’s scathing post about Venture Capitalists in which he decries the industry’s masses. “I don’t know the exact math, but I hear it again and again: the top 2% of firms generate 98% of the returns in venturecapital.” So let’s look at the main assertions.

If there’s a jobs startup within 2000 miles of NYC, I will see it. There’s nothing more demoralizing to try and change the face of human capital to have to sell a job post when you know it doesn’t work. Everyone sends me startups in this space because of my experience with Path 101 and my passion for helping people with their careers.

Look more modern than our previous website, which had a very 2000 feel to it. We liked this idea so much we decided to steal it from True Ventures. I wanted to be whimsical and have a blog as cool as Spark Capital. Anything that works well was her implementation. I did anything that seems kludged – I assure you.

Conventional wisdom dictated that they made reckless investments in very early-stage ventures mostly doomed to fail. In addition, angels were up against a selection problem: All the best entrepreneurs and opportunities would naturally gravitate to the best venturecapital funds, leaving only the “scraps” for angel investors.

I’m just pointing out my gut feel for approximate ranges of deals that I’ve seen with Silicon Valley having the highest valuations, NY / LA / Boston / Boulder / Seattle having valuations in a slightly lower range but comparable and sometimes significantly lower prices in markets that don’t have a healthy venture market.

Most venture capitalists who have been in this business for a long time foresaw this correction and have been talking about it privately for the better part of the last year or two. Many experienced partners are funds have 7-10 boards and most of these will need more capital. That’s the beauty of markets and of capitalism.

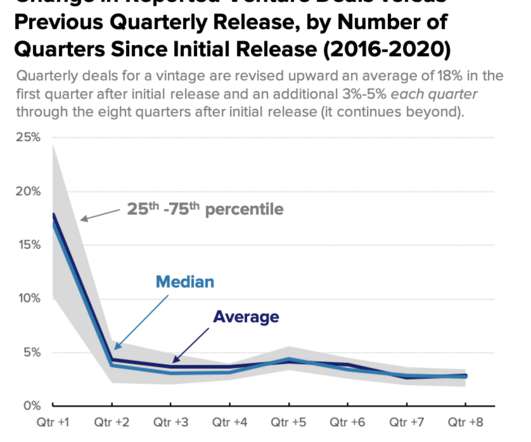

Last month, I published an analysis of venture deal activity in the United States during the COVID-19 pandemic, which demonstrated that despite early warnings of an impending collapse, the pace of venture deal activity in the first half of 2020 was more or less on par with 2019. We now have fresh data to extend that analysis.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content