This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Yes, it’s true that FOMO (fear of missing out) is driving some irrational behavior and valuations amongst uber competitive deals and well-financed VCs. In 1998 there were around 850 VC funds and by 2000 there were 2,300. By 2000 the total LP commitments had mushroomed to more than $100 billion. The Funding Problem.

Many people bandy about the definitions of “disruptive technology&# or “the innovator’s dilemma&# without ever having read the book and almost universally misunderstand the concepts. What is “disruptive&# is that is also dramatically less expensive. It is often LESS performant. Enter Salesforce.com.

I know that most people who are close to them tend to deny their existence, as we saw in the great housing bubble of 2002-2007 and the dot com bubble of 1997-2000. Or worse yet they may never get financed. Raise at “ the top end of normal &# but not so high that future financings in a corrected market become impossible.

The key question he poses is: has the industry become so large that it needs to be disrupted? 2018 and 2019 exceeded the heady days of 2000 in terms of dollars deployed. Also, more venture firms and startups are choosing debt as a non-dilutive financing alternative. in the New Yorker.

And so it happened that between 2000-2008 I was the biggest buzz kill at dinner parties. That would mean that the increased number of new business startups will lead to a “funding gap&# of deals that can’t get financed. I’m looking at how the digital living room will change media consumption.

Today, disruption is rather slow-paced. Startups are known to disrupt the markets, and this disruption usually ends up in developing totally new demand for its offerings. Such demand and other metrics of a disruptive startup, when represented in the form of a graph, form a shape of a hockey stick.

I have experienced two major financial disruptions in my career: the bubble burst in 2000 and the financial crisis of 2008. In the past decade, we lived through an unprecedented run of optimism and climbing valuations, and the gut check we’re seeing now has been long in coming.

The investment firm Flagship Pioneering has incubated a lot of life sciences companies since it was founded in 2000. But because of the scale of the opportunity that we saw ahead of us with Valo, we actually started out by bringing in external financing partners as part of a Series A that was right around $100 million.

Sparked by a pair of scissors, some pantyhose and a party where founder, Sara Blakely , wanted to look her best, Spanx officially began production in 2000 and changed women’s fashion and fit forever. Peeler isn’t just changing the world of student aid, she’s also redefining the role of women entrepreneurs in finance and education.

That conversation hasn’t disappeared, but it has certainly gotten quieter, with many investors now telling me that there’s a super surge of financing on the way. billion in financing for startups that use its own platform. We’re less than one month away from TechCrunch Disrupt, and I’m already emotional. Well, kind of.

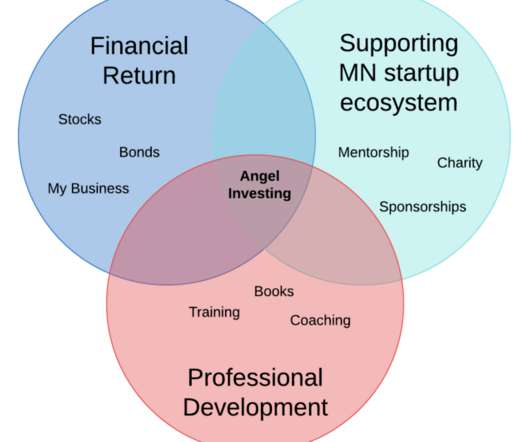

THE ORIGIN I was the Founder & CEO of InboxDollars from 2000 to 2019. I learned something new with each pitch deck, each conversation with a Founder, each term sheet, each stock purchase agreement, each follow on financing, each exit event… Of course I expected that by angel investing I would learn about angel investing.

Independent sponsors (groups seeking to acquire a company which do not have the equity financing needed in advance) earn nothing upfront, but earn 20% of the deals they facilitate. Similarly, certain Revenue-Based Finance investors (e.g., Methods in between are a tradeoff of compensation and carry.” Anthos Capital. Class Global.

Between 2000 and 2015, for example, spending on education in the US grew 15%, but test scores have been stagnating. Furthermore, the disruptions the world faces, whether social, economic, health or education- related, affect us all. We’re proud to be partnered with Social Finance Israel, a global leader in impact advisory.

2014 will be the third largest year in VC fundraising since 2000. The financing markets are a train and the IPO market and M&A markets are the locomotive, setting pricing multiples and valuations. But at the moment, founders are building impressively large, disruptive companies. What would cause a change in the environment?

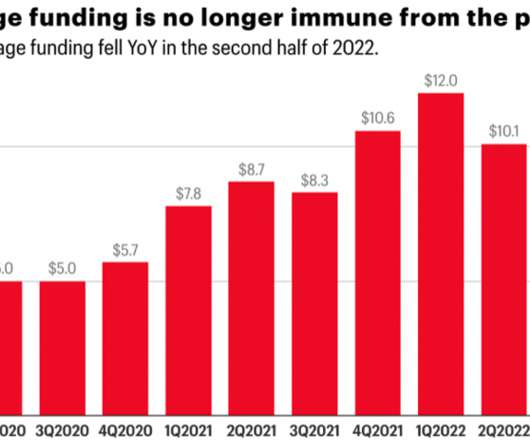

Major capital market disruptions often bring a “VC Reset,” as venture firms rethink fundamentals, often pressured to do so by limited partners. FIGURE 17: NUMBER OF COMPANIES ANNOUNCING NEW FINANCING ROUNDS Source: Crunchbase In 2022 the demand for capital outstripped the supply and this gap worsened as the year progressed.

Founded in 2000 by Vikas Jain, Rahul Sharma, Sumit Kumar Arora and Rajesh Agarwal, Micromax first started life as a small IT firm, making its first move into phones only in 2008. A shift to urban mobility from mobile phones would not be the first time that Micromax reinvented itself.

On June 18, Aswath Damodaran , a finance professor at NYU’s Stern School of Business, published an article on FiveThirtyEight titled “ Uber Isn’t Worth $17 Billion. This post was a shortened version of a more detailed post he had written for his own blog titled “ A Disruptive Cab Ride to Riches: The Uber Payoff.” Different Economics.

Terrorism at scale can only occur when these organizations can move money around to finance people who make bombs, buy guns, train recruits and so forth. Trust Between 1998–2000 the world became enamored with the “new economy” and Internet companies that were going public on NASDAQ in the United States. Regulation will come.

They procured additional financing at a 66% discount to their previous round … ouchie … but at least they did not have to halt withdrawals. It has been around since the 2000 dot.com bubble and has traded at some pretty astronomical P/E ratios. NFTs will not perish, and their disruption to the economics of culture will be profound.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content