This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

And so it happened that between 2000-2008 I was the biggest buzz kill at dinner parties. They have marked-up paper gains propped up by an over excited venture capital market that has validated their investments. Logic tells me the following: It is hard to make money angel investing. It was an investment management class.

My partner Albert told me that when you factor in the financing costs of this swap, the average home in the Northeast United States could save $1000 to $2000 a year by doing this swap. It has gotten less expensive to do this swap out as solar and heat pump costs have come down.

Looking ahead at the next decade I am excited by what I believe will be viewed as one of the best and most rational investment periods for venture capital due to seven discrete factors: 1. In 1998 there were around 850 VC funds and by 2000 there were 2,300. By 2000 the total LP commitments had mushroomed to more than $100 billion.

The VC industry grew dramatically as a result of the Internet bubble - Before the Internet bubble the people who invested in VC funds (called LPs or Limited Partners) put about $50 billion into the industry and by 2001 this had grown precipitously to around $250 billion. So the people who invest in VC funds have two problems.

When I made my first angel investment in 2000, I wish I knew then what I know today. As a newly minted angel, I assumed that angel investing would be easy to jump into and become successful at. Experience is what you get, when you don’t get what you want. I was partially right… it was easy to jump into.

Those companies would have not only returned any fund that invested in them, but would likely return an entire career''s worth of investing over the course of several funds. Why invest at top dollar in the last round, when you can offer liquidity to early investors at a huge discount to the last round? But at what valuation?

Instead, ask a question specific to their approach to investing—something simple enough like what’s going on at their stage. 4) Don’t push for me to say yes or no right then—because I see 2000 things in a year and do 8-10 of them. or asking a generalist, “What areas are you interested in?” Why would you do that?

million which closed the first week of March 2000 – a week before the market crashed. Quick aside: how can VC’s invest in online businesses, digital media, social networks or mobile applications if they don’t actually use the products actively themselves? True story.) million were enormous.

We have previously raised funds in 1996 ($200 million), 2000 ($400 million) and 2008/9 ($200 million). Like many modern VCs, we’re committed to investing in the community and in our portfolio companies. Let’s start with the fund. This month we closed our 4th fund of $200 million. See what we did there?

It’s also meaningless if they had four $200 million funds and the last one they closed was in 2000. VC’s don’t invest 100% of their own money. Unfortunately over the period of 2000-2010 the VC industry hasn’t performed well and therefore the number of funds going forward is likely to reduce greatly.

I will argue that LPs who invest in VC funds will also need to adjust a bit as well. These two trends had a major impact on the computing industry from 2000-2005 but the effects weren’t yet felt by the VC industry. When I built my first company starting in 1999 it cost $2.5 The Emergence of “Open Cloud&# Infrastructure.

In fact, thanks to increased scrutiny of investment funds in a post-Madoff world, this imbalance will probably get bigger and bigger. But crowdfunding investments in startups is the answer to all our worries in life, right? If venture funds could be supported by the local communities they invest in, you'd create a fantastic dynamic.

Chris then discussed his current approach to angel investing in that he tries to do everything through Founder Collective (FC), unless it is out of the purview of the firm’s investment thesis, then he’ll do it on his own. The firm focuses on early stage companies in the Northeast but occasionally invests in California startups.

I get 2000 things passing through my inbox in any given year, and I make about ten investments per year. How excited do you think I am if I’m only picking the top 10 out of 2000? That’s because of the simple math of competition. Do you think any of those handful of deals are seven out of ten?

We moved into the legal process and final due diligence in January and February of 2000. Our final closure was the first week of March 2000. If it’s a biz deal you might care about IP protection, revenue share, investment commitments to joint marketing – whatever. Our final closure was the first week of March 2000.

They have totally changed the way you run a VC firm, investing heavily in systems & events for their founders that are pushing the boundaries of the way our industry works. In the early 80’s he left academia to work on venture capital investing with Jim Simons, Renaissance Technologies. Investing Strategy. and Half.com.

Assume you have the right factors to get angel investment: experienced team, good product-market fit, growth potential, defensibility, and a reasonable shot at a successful exit. This might seem awkward on this site, suggesting that you don’t want angel investment. But angel investment isn’t for everybody.

Ad-buying opportunities within podcasts have historically been manual and limited, not unlike the process of purchasing web ads pre-2000. USV has been looking for an opportunity to invest in podcasting that fits with our thesis and we found it with Headgum and Gumball.

In fact, they will think better of you because you’re demonstrating that you’re the kind of thorough person that they wanted to invest money into in the first place. My chips were down in late 2000 / early 2001. Don’t be afraid to (politely and respectfully) ask for this. Don’t stop there. My story briefly.

In the Correlation post, they define “hit rate” as: the percent of invested dollars generating a 10X or greater return. It could be the number of investments in your portfolio that return the fund. It could be the number of seed investments you make that turn into billion-dollar valued businesses.

The framework of his book has profoundly altered how I think about the technology market and affects how I thought about building my businesses and how I think about investing in venture capital. In 1999-2000 they weren’t doing enterprise-wide installations at Merrill Lynch, Dell and Cisco. It is not a beach novel to be sure.

I don’t believe that search is the only answer in 2010 as it was in 2000. I won’t belabor this – I have an investment in this space ( ad.ly ) so I’m biased. I think this classifies as a “crack filler&# and I’m not sure I would have done the investment for that reason. Finally, I HATE the name.

I know that most people who are close to them tend to deny their existence, as we saw in the great housing bubble of 2002-2007 and the dot com bubble of 1997-2000. million pre-money valuation is now raising $1 million at a $12 million valuation the next investor has nowhere to go but up (or sit out the investment).

Originally a computational physicist who spent many long nights at a particle accelerator, since 2000 Paul inspired thousands of people to innovate, help hundreds of startups launch, overseen investments in 50+ startups and held leadership positions in the national angel investor community. Your Instructor.

I learned this lesson long ago – many investors wait until you’re staring at a cliff before committing whether to re-invest in you. We control our hours, our travel and our investment areas. Let’s say you became a partner in a VC fund in 1995 and started investing heavily in 1997-99. I had to go there? Making bank.

<Small plug> – I invested in an awesome company called … awe.sm … that is a performance tracking tool that let’s you measure efficacy of channels like this (email, facebook, twitter, linkedin, etc.) They never did any PR or marketing to get their videos to first get shown on the news during the 2000 election.

Look more modern than our previous website, which had a very 2000 feel to it. We wanted to emphasize the number of truly big wins that have been created by the partners at GRP in their 20+ years of investing. Yet we wanted to be clear that we invest heavily in digital media, mobile & software companies. That’s here.

Upfront VI is our latest core fund and is $400 million to invest in early stage entrepreneurs. LPs (the people who invest in VC firms) have clearly voted in favor of LA with the creation of 15+ new early-stage venture firms and the continued growth is size and team of the great larger firms that are well established.

Venture Capital funds: the different between “closed funds&# (which typically have a 10-year time horizon) and “evergreen funds&# which re-invest profits back into the fund. An investment doesn’t guarantee your product will suddenly be on the investor’s price sheet. DST invested $180mm last fall.

I believe the middle isn’t being “gutted” but rather is being supplemented by “opportunity funds” and “growth funds” that sit side-by-side “core funds” allowing the firms to stay small and nimble while still being able to grab prorata rights of their best early-stage investments.

Qualcomm Ventures , Qualcomm’s investment arm, today announced four new strategic investments in 5G-related startups. “Within 5G, there are three buckets of areas we look to invest in: one is in use cases, second is in network transformation, third is applying 5G technology in enterprises.”

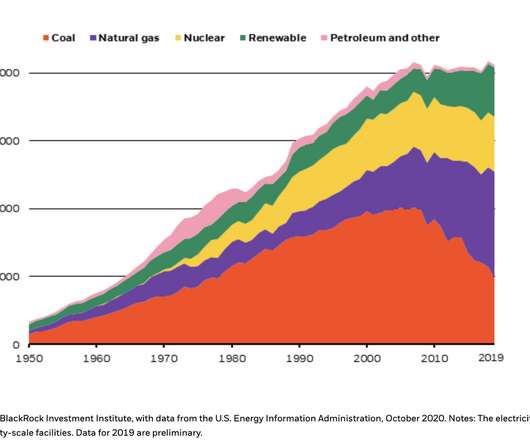

Companies in developed markets have churned out profits at a historic pace, despite massive economic dislocations like the bursting of the dot-com bubble in 2000 and the global financial crisis eight years later. We invested in online technologies and continue to do so, to improve communication and its periodicity.

How much money will they reserve from their fund for future investments in your startup? How much pull that investment professional has within his or her fund? which matters for getting future support) Where the fund is in its investment cycle (year 1 out of 10 or year 7 out of 10)? What percentage of their fund will you be?

Most top tier VCs return about 3x invested capital and outlier funds (the best of a vintage) might return 6-8x. But the larger funds usually have lower returns because they are often investing bigger dollars at later stages with less risk and therefore lower returns. In 2000 our industry had more than $100 billion in LP money.

Within a year, by late 2000 / early 2001 consulting firms were firing people en masse. Investment in training, adherence to process, global knowledge sharing systems, quality control / partner reviews and campus recruitment programs that attracted the right talent. Most of the Internet startup consulting firms went bankrupt.

If you invested in the first angel round of a startup company it is usually very hard to sell your stock – usually for many years if ever at all. The earlier you invest the higher the chances the company won’t work out and thus you pay a lower price than later-stage investors. It was early 2000. That was market.

Spark Capital is relatively new to VC (founded in 2005) yet has become one of the hottest new VCs having invested in Twitter, Tumblr, AdMeld, Boxee, KickApps and many more companies. Founded in January 2000 in Oakland by Tim Westergren; new CFO, Steve Cakebread was previously CFO of Salesforce.com. Content, of course, is the same!].

We spoke about the changes to an “accredited investor&# proposed by Chris Dodd – This would be bad for angel investing. Following Microsoft’s addressable advertising trials with NBC in June 2009, many suspect that Google’s investment may have some defensive motivations, as well. We spoke briefly about why.

tevye2009 , Q: “can you briefly explain why it’s best to get a small valuation when getting investment.&# The A round was done in February 2000 (end of the bull market) and my B round was done in April 2001 (bear market). 6: @ marklanday Q: “Do you make personal angel investments and if so what are your criteria?&#

We could do more in 2010 with more VC investment; the doubling assumes only ratable increase in marketing spend to achieve profitability. Coupled with my participating preferred from 1999 and 2000 I had more than $55 million of liquidation preferences. The net effect for [my company] for example is we are now doing reasonably well.

You shouldn't, because it's still your fault they didn't invest. Getting an investment is very difficult thing. Well, my own statistics are that about 2000 things come across my desk in a year, and I make 8-10 investments. Maybe they didn't even have the guts to say no. How difficult? That's the top 0.5%.

When venture capitalists scale back investing activities it can be very swift and leave many companies that are in the process of fund raising hung out to dry. Just ask anybody who was trying to close funding the fateful week of September 11, 2001 or even March 2000. The best MBA class I took was an investment strategy class.

I began studying angel investing returns about 10 years ago as a result of a problem I couldn’t resolve: The investing world seemed certain that angel investors were rubes. Conventional wisdom dictated that they made reckless investments in very early-stage ventures mostly doomed to fail. Only they’re not.

Alomar, who led startups through the dotcom bust of 2000 and the Great Recession of 2008, will talk about whether investors are still prioritizing growth over profits, and identify which proof points founding teams must define before their next raise. Image Credits: OsakaWayne Studios / Getty Images.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content