This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Many observers of the venturecapital industry have questioned whether its best days are behind it. Looking ahead at the next decade I am excited by what I believe will be viewed as one of the best and most rational investment periods for venturecapital due to seven discrete factors: 1. The Funding Problem.

In this three-part series I will explore the ways that the VentureCapital industry has changed over the past 5 years that I would argue are a direct result of changes in the software industry, not the other way around. I will argue that LPs who invest in VC funds will also need to adjust a bit as well.

I was on This Week in VentureCapital (TWiVC) again this week with Jason Calacanis. I don’t believe that search is the only answer in 2010 as it was in 2000. I won’t belabor this – I have an investment in this space ( ad.ly ) so I’m biased. There is also another inherent weakness.

We received so much positive feedback from our This Week in VentureCapital show walking through valuation calculations & term sheets that we decided to do a Q&A show this week to address topics that entrepreneurs want to learn about. In fact, far better if you haven’t raised venturecapital.

And so it happened that between 2000-2008 I was the biggest buzz kill at dinner parties. They have marked-up paper gains propped up by an over excited venturecapital market that has validated their investments. Logic tells me the following: It is hard to make money angel investing. There are too many deals.

Those companies would have not only returned any fund that invested in them, but would likely return an entire career''s worth of investing over the course of several funds. Why invest at top dollar in the last round, when you can offer liquidity to early investors at a huge discount to the last round? But at what valuation?

Back in 2009, I wrote a post called The VentureCapital Math Problem. This 2009 piece from @fredwilson (literally the best in the biz) predicted significant venture industry contraction when in fact the last 10yrs have seen massive expansion. So what did I get wrong in my attempt to solve the venturecapital math problem?

We have previously raised funds in 1996 ($200 million), 2000 ($400 million) and 2008/9 ($200 million). Perhaps the biggest piece of new news is that after 17 years of operations we’ve changed our name from GRP Partners to Upfront Ventures. Well, the venturecapital industry has changed a lot in the past 20 years … and we have too.

This is a story of one of the risks of venturecapital. But some companies have entrepreneurs that seem talented on paper, are in a space that seems interesting to investors and are able to raise venturecapital early in the company’s existence. True story.) 2 weeks later and we may never have raised any more VC.

The VC industry grew dramatically as a result of the Internet bubble - Before the Internet bubble the people who invested in VC funds (called LPs or Limited Partners) put about $50 billion into the industry and by 2001 this had grown precipitously to around $250 billion. So the people who invest in VC funds have two problems.

We moved into the legal process and final due diligence in January and February of 2000. Our final closure was the first week of March 2000. It quickly became impossible to raise venturecapital. It isn’t even a story about raising venturecapital or M&A. They accepted my argument. Any deal.

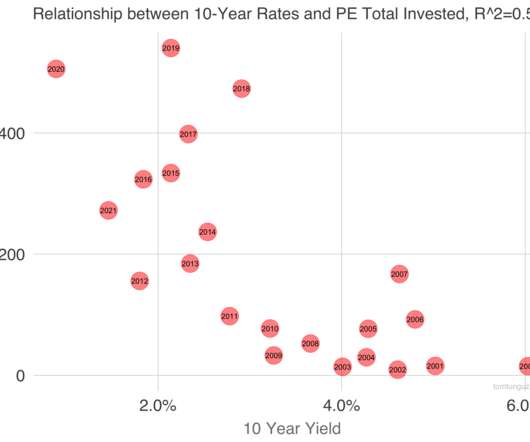

What does it mean for venturecapital and Startupland? Let’s examine the relationship between total venturecapitalinvestment and the 10 year Treasury in some detail. The y-axis tracks enture capitalinvestment by year and the year of the data point resides in the reddish circle.

Amy Cortese published “VentureCapital, Withering & Dying” in the New York Times on Oct 21, 2001. So far this year, 29 venture-backed companies have tried initial offerings, compared with 252 in 2000. Venturecapital funds lost 18.2 In Venturecapitalinvestment pace has slowed.

Andy Areitio is a partner at the early-stage fund TheVentureCity , a new venture and acceleration model that helps diverse founders achieve global impact. When you’re running your own venture — especially if it’s your first — it’s unlikely you will find the time to deep dive into how venturecapital firms work.

This week I sat down with Chris Dixon, co-founder / CEO of Hunch and Partner at Founder Collective in the most recent installment of This Week in VentureCapital. The firm focuses on early stage companies in the Northeast but occasionally invests in California startups.

In fact, thanks to increased scrutiny of investment funds in a post-Madoff world, this imbalance will probably get bigger and bigger. But crowdfunding investments in startups is the answer to all our worries in life, right? Who wouldn't want in on the next Union Square Ventures or First Round Capital funds?

This is part of my series on Understanding VentureCapital. billion under management.&# I don’t really understand why VCs do this since it’s mostly a meaningless number. It’s also meaningless if they had four $200 million funds and the last one they closed was in 2000. What is a VC fund?

What a pleasure that I got to spend an hour talking with both Om Malik (whom I’ve always respected his views) and Paul Jozefak , a venturecapital partner at Neuhaus Partners in Germany (and formerly the head of Europe for SAP Ventures). Paul discussed his perspective having been at SAP Ventures. 406 Ventures.

If you read this blog often you'll know that I'm a huge fan of First Round Capital. They have totally changed the way you run a VC firm, investing heavily in systems & events for their founders that are pushing the boundaries of the way our industry works. Infonautics went public in 1996 and Half.com was sold to eBay in 2000.

I am so proud and humbled to be able to formally announce that Upfront Ventures has raised its 6th venturecapital fund in the past 21 years. Upfront VI is our latest core fund and is $400 million to invest in early stage entrepreneurs. We’ll invest in about 15 new companies every year or just over 2 per partner.

This is part of my ongoing series on Raising VentureCapital. Not so in venturecapital. In fact, they will think better of you because you’re demonstrating that you’re the kind of thorough person that they wanted to invest money into in the first place. My chips were down in late 2000 / early 2001.

This simple and short blog post by the folks at Correlation Ventures contains the key to venturecapital returns – the hit rate. In the Correlation post, they define “hit rate” as: the percent of invested dollars generating a 10X or greater return. More capital means more businesses get funded.

We had a special edition of This Week in VentureCapital this week shooting out of the Next New Networks offices in New York. Our guest was Mo Koyfman of Spark Capital. And what we think about Sequoia’s website , First Round Capital’s and True Ventures (we both like to copy stuff from True). Read more: MediaWeek.

The framework of his book has profoundly altered how I think about the technology market and affects how I thought about building my businesses and how I think about investing in venturecapital. In 1999-2000 they weren’t doing enterprise-wide installations at Merrill Lynch, Dell and Cisco. Enter Salesforce.com.

I know that most people who are close to them tend to deny their existence, as we saw in the great housing bubble of 2002-2007 and the dot com bubble of 1997-2000. million pre-money valuation is now raising $1 million at a $12 million valuation the next investor has nowhere to go but up (or sit out the investment).

I began studying angel investing returns about 10 years ago as a result of a problem I couldn’t resolve: The investing world seemed certain that angel investors were rubes. Conventional wisdom dictated that they made reckless investments in very early-stage ventures mostly doomed to fail. So which is it? Only they’re not.

We could do more in 2010 with more VC investment; the doubling assumes only ratable increase in marketing spend to achieve profitability. Coupled with my participating preferred from 1999 and 2000 I had more than $55 million of liquidation preferences. The net effect for [my company] for example is we are now doing reasonably well.

Assume you have the right factors to get angel investment: experienced team, good product-market fit, growth potential, defensibility, and a reasonable shot at a successful exit. This might seem awkward on this site, suggesting that you don’t want angel investment. But angel investment isn’t for everybody.

<Small plug> – I invested in an awesome company called … awe.sm … that is a performance tracking tool that let’s you measure efficacy of channels like this (email, facebook, twitter, linkedin, etc.) They never did any PR or marketing to get their videos to first get shown on the news during the 2000 election.

How much money will they reserve from their fund for future investments in your startup? How much pull that investment professional has within his or her fund? which matters for getting future support) Where the fund is in its investment cycle (year 1 out of 10 or year 7 out of 10)? What percentage of their fund will you be?

Next Wednesday we’ll have Dana Settle of Greycroft Partners, a New York / LA early-stage venturecapital fund. We spoke about the changes to an “accredited investor&# proposed by Chris Dodd – This would be bad for angel investing. Invidi is based in New York and founded in 2000. Short answer: no.

Is there a bubble going on in seed investing? Retail investors were burned in IPOs in 2000, Consumers getting burned by services disappearing) Minutes 31-35. Tags: This Week in VentureCapital. Not as many entrepreneurs are aspiring to do it any more. Minutes 23 – 26. Dan: Maybe in the future, but not now.

“I don’t know the exact math, but I hear it again and again: the top 2% of firms generate 98% of the returns in venturecapital.” Most top tier VCs return about 3x investedcapital and outlier funds (the best of a vintage) might return 6-8x. In 2000 our industry had more than $100 billion in LP money.

The easiest way to work with and for VC funds is to become a part-time scout, getting paid for sourcing investments. How to win consulting, board, operating, and investment roles with private equity and venturecapital funds (video). How to get a job in venturecapital. But how do you do that? .

If you invested in the first angel round of a startup company it is usually very hard to sell your stock – usually for many years if ever at all. The earlier you invest the higher the chances the company won’t work out and thus you pay a lower price than later-stage investors. It was early 2000. That was market.

Historically, ventureinvesting right after major market downturns – such as after the Internet bubble burst in 2000-2002, and after the financial crisis of 2007-2009 — has proved lucrative because you’re buying at a discount. That’s a very good entry point for new venture investors. Watch the latest from OurCrowd.

Andrew Chan is a senior associate at Builders VC , investing in early-stage companies that are transforming pen and paper industries. In the last couple of years, a large group of “Gen Z VCs” have come to the forefront of what one might consider “hip” venturecapitalinvesting. Andrew Chan.

Most venture capitalists who have been in this business for a long time foresaw this correction and have been talking about it privately for the better part of the last year or two. We write about $40 million of first-checks into new deals / year and about $40 million of follow-on investments. What is the True Sentiment of VCs?

Nathan Heller published an article called Is VentureCapital Worth the Risk? It’s a well-researched critique of the venture industry. If you have ideas for how to improve venturecapital for founders, please tweet me or send me an email with the link above. In the 2000s, a wave of PE funds went public.

In addition, we saw Voyager Ventures launch its first fund , which will pump $100 million into climate technology startups in North America and Europe. We asked Beezer Clarkson, partner at Sapphire Ventures, and Josh Lerner, the Jacob H. Overlooked Ventures co-founders Janine Sickmeyer and Brandon Brooks. That’s new.”.

Navin Chaddha is managing partner at Mayfield , an inception and early-stage investor with more than 50 years of a people-first investing philosophy. What is happening to risk-taking in venturecapital? More posts by this contributor. Biology as technology will reinvent trillion-dollar industries.

But, still, every startup, especially those seeking angel and venturecapital funding, are conditioned to project this growth curve – because investors love it. Blade Years: The blade years lasted for at least 3 years from 1997 to 2000, where its revenue was around 1.5 Today, disruption is rather slow-paced.

As the recipients of less than 1% of venturecapital raise, institutionalized systems are visibly at play. When you think about the intersection of venturecapital and technology, and specifically how it works — it is being led from an engineering perspective. I was in college from 2000 to 2004.

Alomar, who led startups through the dotcom bust of 2000 and the Great Recession of 2008, will talk about whether investors are still prioritizing growth over profits, and identify which proof points founding teams must define before their next raise. 3 tips for biotech startups seeking non-dilutive capital to weather the downturn.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content