This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

And that was evident on today’s Angel vs. VC panel. The VC industry is segmenting – I have spoken about this many times before. The VC industry has different segments in it that have different fund sizes, different investment amounts and different risk / return expectations. It’s just not a VC investment.

I can’t help feel a bit of rear-view mirror analysis in all of “VC model is broken” bears in our industry. To really assess what opportunities the VC industry has over the next decade, one needs to first look at some of the root causes of poor returns in the past decade. THAT is disruption. The Funding Problem. The Exit Problem.

And so it happened that between 2000-2008 I was the biggest buzz kill at dinner parties. Remember it was only 2008 where Microsoft and even Google were laying off employees. I saw VCs doing crazy things in 2007-08 when I first entered the VC market – crazy prices, limited due diligence, large funding rounds.

I spoke about how Amazon Web Services deserves far more credit for the last 5 years of innovation than it gets credit for and how I believe they spawned the micro-VC category. I said that I felt that Micro-VCs were the most important change in our industry. It is great for entrepreneurs and great for VCs. I believe that.

And we will see legacy applications embrace AI to make their products better and to remain competitive with the AI-first disrupters. I think both will grow but not nearly as fast as the sectors that surround VC. AI developed for over forty years before its coming out party. I think it will take web3 less than half that time.

Recently the firms two founding partners (and also Managing Partners) — Fred Wilson and Brad Burnham — decided to transition management of the firm to Andy Weissman (who joined in 2012) and Albert Wenger (joined in 2008 and writes one of the most thoughtful blogs in our industry ). Maybe that’s USV, too.

I was saying that I was happy it was all out in the open because I felt at least everybody could now understand the issues & opportunities from the perspectives of angels, entrepreneurs and VCs. Let’s be clear: AngelList doesn’t scare a single VC I know. But it’s not cutting VCs out. It is additive.

A little startup by the name of Dropbox competed in the Battlefield at TC50 (the precursor to Disrupt) way back in 2008. TechCrunch is on the hunt for innovative, game-changing startups to take the Startup Battlefield challenge and wrangle with the best-of-the-best at TC Disrupt 2021 in September. Are you game?

In fact, among the earliest use cases for the company was helping startups track engagement with their pitch decks at VC firms. million, according to Crunchbase, but Heddleston says that he wanted to build a company that was self-sufficient and raising more VC dollars was never a priority or necessity.

At the Upfront Summit in early February, we had a chance to have many off-the-record conversations with Limited Partners (LPs) who fund Venture Capital (VC) funds about their views of the market. A normal VC fund raises a new fund every three years if they are strong performers. That’s money that fuels our startup ecosystems.

For example, activist hedge funds, and most private equity and VC funds. A private equity/VC investor can proactively recruit new team members, win clients, or if necessary change management. . This negative externality is unique to financial services and was particularly obvious in the 2008 Global Financial Crisis.

Finishing is the ripest for disruption. From 2007 to 2011, during which the Great Recession of 2008-09 took place, the construction industry lost approximately 2 million workers. Zach Aarons, MetaProp VC Which trends are you most excited about in construction robotics from an investing perspective?

The battle to win Startup Battlefield began long before TechCrunch Disrupt kicked off Tuesday. Without further ado, here are the five judges who will pick the 2021 Startup Battlefield winner: Kirsten Green is the founder and managing partner of Forerunner Ventures, a San Francisco-based VC firm she formed in 2010.

7 investors explain why they’re all in Pitch Deck Teardown: Uber’s $200K pre-seed deck from 2008 Image Credits: Uber (opens in a new window) The word “disruptive” gets thrown around so much, it’s lost much of its impact. While it isn’t a trivial decision, it’s also not as hard as you might think.

4/ 2008 Feels Like 3 Decades Ago – This isn’t fair to AppNexus at all, because a $1.6B+ exit is huge stuff, but it is a long time ago, and the way news cycles move today, feels eons ago; additionally, in the wake of $7.5B at the right time across both broadband and mobile networks.

If you had adopted that, this was a logical next step that you could apply, which again, was like a playbook that you could run over top of a new technological disruption that had happened. In 2008, I started a business called RJMetrics, which was basically the first SaaS analytics platform. And this is my third SaaS company.

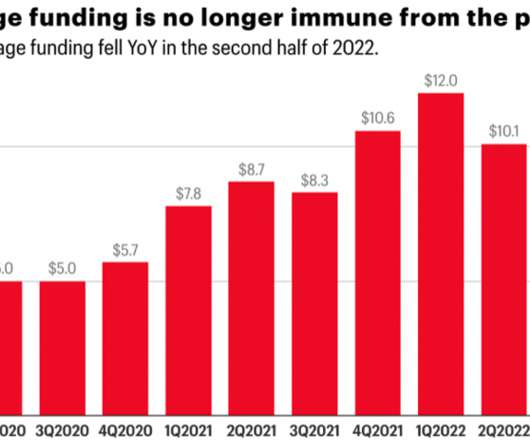

From an investor’s perspective, 2022 witnessed a sudden market reversal from an extreme equity seller’s market to an equity buyer’s market, causing dislocations throughout angel, VC, and startup ecosystems. It is unclear if VCs will agree to these terms, but LPs believe they now have more leverage. Smaller VC fundraises?

Startups and VC While most VCs will tell you they had no problem raising their newest fund, Volition co-founder Larry Cheng — an alum of Bessemer Venture Partners, Battery Partners and Fidelity Ventures — says that wasn’t his experience when trying to raise the firm’s latest vehicle. You can sign up here.

Sure, when s**t really hits the fan, like in 2008, and the whole market goes haywire, everyone's going to feel it, but in any kind of normal environment, hedge fund returns should be largely uncorrelated to anything else. I experienced that myself with my startup in 2008 and 2009. Those companies didn't execute as well as they should.

And on the distant horizon, TechCrunch Disrupt will return to San Francisco on October 18. Startups and VC. In other news, TechCrunch’s Summer Party yesterday was a major success — thanks to all who turned up! I can’t wait to see your smiling faces there. Need reading or listening material in the meantime?

By 2008 I had gotten more serious about championing companies through our investment process. I started showing my partners more deals that I found interesting and doing loads of analysis on the future of markets I thought were ripe for disruption. I have always believed that TV was ripe for disruption. It was September 2008.

Prior to the 2008 Global Financial Crisis, Goldman Sachs, Morgan Stanley, Merrill Lynch, Bear Stearns, and Lehman Brothers were true investment banks. Thank you VC money, keep pumping the market full of that fee-adjusted beta! Focus your attention on the 2008 time period. Those who do not study history are doomed to repeat it.

Today, Daye is announcing a £10 million (~$11.5M) Series A round — which includes investment from London-based Hambro Perks, global VC firm MassMutual Ventures and Canadian VC Cross Border Impact Ventures — and brings its total raised to £19M (or just under $22M) to date.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content