This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I’d rather be Roger Ehrenberg with a thesis around data-centric companies and base my investment decisions on the skills I’ve developed in my career. To some extent Keith Rabois agreed with me about domain knowledge and argued that most of his investments are in the consumer Internet space as a result. Always have been.

Seed investments are down by any measure (funds, deals, dollars) over the past 3 years in deals < $1 million AND in deals between $1–5 million. why the hell has seed financing declined so much in the past 3 years?? Between 1999–2005 the costs went down by 90% and between 2005–2010 they went down a further 90%. What gives?

They have marked-up paper gains propped up by an over excited venture capital market that has validated their investments. Logic tells me the following: It is hard to make money angel investing. Too many angel deals just means more to watch and invest in for the ones that do succeed (if the VCs can get in at reasonable prices).

So why invest in that period of uncertainty unless it’s early-stage and thus valuation matters less. If the next 30 days stays calm then investment will pick up. So, too, investments. It will make follow-on financings much harder and people will have to consider whether or not to do inside rounds.

At the time I pointed out: “If I had realized exits almost certainly it would be because I invested in a company that failed. In 2010 somebody posed the question on Quora, “Is Mark Suster a Successful Venture Capitalist? I’ve now been involved with many other successful foll0w-on financings. ” Still.

YC''s best investing days may be behind it. YCombinator had a great run from 2007 through early 2009 investing at a time when there weren''t nearly as many seed funds and accelerators as there are now. Considering the myopia at the top, it''s not surprising that turning point may have already happened for YCombinator.

I’m obviously only naming a small fraction of their investments since I don’t feel inclined to research them all and many other great venture firms have this kind of access. It’s hard for me to imagine that angel investing outcomes judged 10 years from now will have a drastically different profile. Or the CEO?

Thomas Rush is founder of Bootstrapp and Head of Investment Platform at ConsenSys Mesh. Revenue-based investing ( RBI), also known as revenue-based financing, or revenue-share investing, 1 is a natural next step for the private equity and early-stage venture investment industry. Share on Twitter.

The VC industry has different segments in it that have different fund sizes, different investment amounts and different risk / return expectations. If you’re an angel you invest your own money and you have nobody to answer to except your spouse. If you invest it in startups you’re a VC professional money manager.

I’d rather be Roger Ehrenberg with a thesis around data-centric companies and base my investment decisions on my background. I should say that I agree that naive optimism in entrepreneurs can produce higher beta (upside or flops) and that’s good from an investment standpoint if you’re looking for big returns.

Limited Partners or LPs (the people who invest into VC funds) have taken notice as 2014 is by all accounts the busiest year for LPs since the Great Recession began. pre-money valuation you certainly would want to exercise your right to continue investing if you had prorata rights. and the bigger funds can’t get in directly.

This week we closed $250M in financing from Silver Lake , the premier technology private equity firm. Of course a nice chunk is primary capital, i.e. for the company balance sheet, to invest in growth initiatives, security and quality, and advancing our existing strategic priorities through acceleration and de-risking.

The truth is that I’ve been warning about convertible notes since 2010 it was first declared that “convertible notes have won.” Pre-money ($8m) + investment ($2m) = Post-money ($10m) and the investors now own 20% of your company $2m / $10m. So how DOES a VC think about financings at early stages?

Looking ahead at the next decade I am excited by what I believe will be viewed as one of the best and most rational investment periods for venture capital due to seven discrete factors: 1. Yes, it’s true that FOMO (fear of missing out) is driving some irrational behavior and valuations amongst uber competitive deals and well-financed VCs.

Clearly a startup should consult its lawyer before filing or not filing.But the attorneys I relied on to write this piece told me that they’ve done lots of Section 4(2) deals in the past, and would recommend it to clients who had relatively simple financing agreements (not tranched-out, not too many investors, etc.) Short answer: no.

2018 YLAI Fellow Gastón is the founder of eaInversores , an online platform based in Córdoba, Argentina, that provides low-cost investment assistance and financial literacy education. Few in Argentina are actively investing their money,” Gaston says.

Every investment so far in this YC batch (and there have been a lot) has been done on a convertible note.&#. Convertible debt is an investment that “converts&# into equity in the future usually at a discount to your next funding round price and sometimes has a “cap&# (maximum price). “Convertible notes have won.

Ugandan technology-enabled asset finance company Tugende today announced that it has closed $3.6 The investment, which, according to the company, was agreed on and structured in 2020, follows the $6.3 million raised in November 2020 and led by Toyota Tsusho investment fund Mobility 54. million in a Series A extension round.

Spark Capital is relatively new to VC (founded in 2005) yet has become one of the hottest new VCs having invested in Twitter, Tumblr, AdMeld, Boxee, KickApps and many more companies. Mo & I both have double majors with one being finance / econ. Our guest was Mo Koyfman of Spark Capital. Content, of course, is the same!].

Rustic Canyon is an LA-based, but geography-agnostic VC that is currently investing from a $200 million fund. They were originally founded inside of Times Mirror and had a huge string of major investment success before spinning out as a fully independent fund. VC Financings: 1. Read more: TechCrunch. Wildfire Interactive.

How to finance a new seed-stage startup? As of August 2010, Paul Graham famously proclaimed , “Convertible notes have won. Every investment so far in this YC batch (and there have been a lot) has been done on a convertible note.” A convertible note financing is not a loan in the conventional sense.

Does the traditional VC financing model make sense for all companies? A new wave of Revenue-Based Investors are emerging who are using creative investing structures with some of the upside of traditional VC, but some of the downside protection of debt. So what is Revenue Based Investing? Absolutely not.

Megan, also known at The Cyclist Lawyer , formed her own law practice in 2010 at age 29. In early 2018, we happened to fall into one of those phases where we had lots of new cases requiring lots of up-front investments in records, experts and filing fees. I streamlined my accounts and finances.

When I began investing a little over five years ago, it felt like the conventional wisdom was that one had to invest in the Bay Area to harvest venture-like returns. Will the next company to raise $100M in financing just poach from decent seed-stage companies and pay triple the amount to lock up talent?

It is 2010. That means that they likely raised money at a particularly high price relative to 2010 prices. They don’t have the appetite to invest more money but they want to protect all (or much of) of the investment they’ve made too date. Find out whether they plan to pass on the investment internally.

Just two years later, in 2009, we worked out a deal to create the Techstars Seattle program, with our first program running in 2010. From the beginning, we were deeply committed to Techstars’ “give first” ethos and mentorship-driven approach to startup investing. Bottom line, Techstars needed cash.

So it’s really hard to draw too many conclusions about whether the investment really makes sense because often you learn stuff in the fund raising about the future strategy of the company that might make you much more excited than somebody on the outside might be. Others I have not. 24.5mm in Series C. Online peer-to-peer lending.

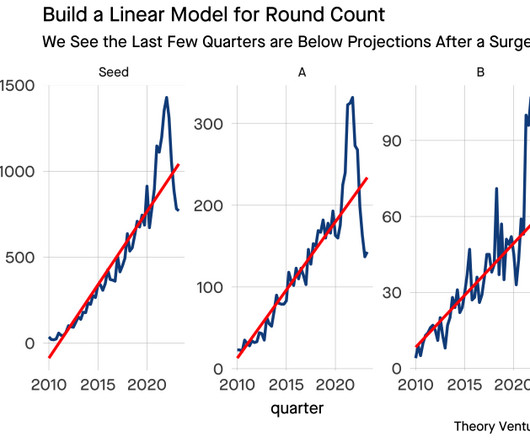

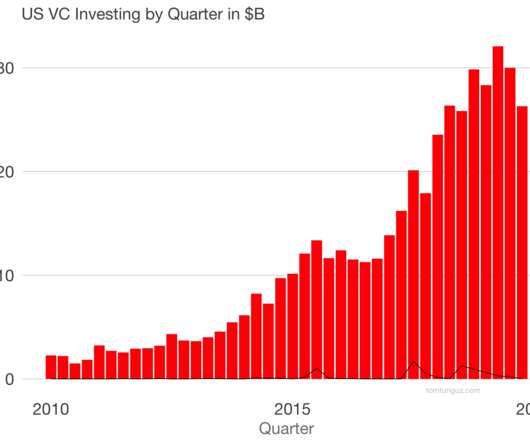

Since then, investing activity dropped precipitously. The red is a linear model based on data from 2010 to 2018 that predicts activity rates for each financing series of US & Canadian software companies. [1] When a collapse follows a surge, mean reversion suggests behavior should revert to a reasonable baseline.

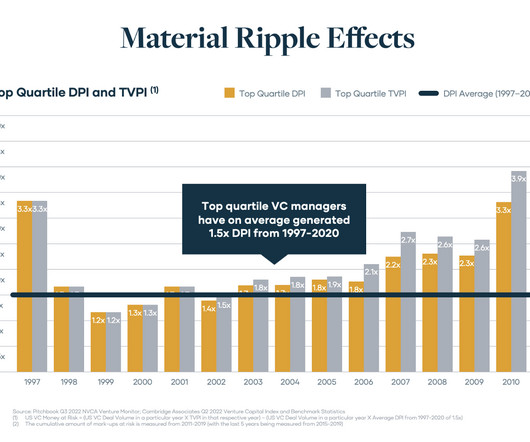

We looked at the analysis in two parts: the 1997–2010 time period and the 2011–2020 time period. 1997–2010 The chart above captured fund vintages that were fully-seasoned and had distributed most of their holdings. 2010–2020 We then looked at the top quartile fund performers for fund vintages since 2010. since 2011.

Martino founded Bullpen in 2010 with a focus on post-seed, pre-Series A startups, and he led the fund’s investments in companies like FanDuel, Namely, Ipsy, SpotHero, Classy, and Airmap. This geographic distinction is now less about actual geography and more about mentality and style of investing of these types of firms.

Investment in training, adherence to process, global knowledge sharing systems, quality control / partner reviews and campus recruitment programs that attracted the right talent. And coming to the end of 2010 I feel a sense of reminiscence of some of the trends from a decade ago. The things that always differentiated Accenture?

from 2010 to 2019. million jobs due to Google’s $1 billion investment in the continent. The continent’s investment story. The report first highlights the growth of venture capital on the continent over the past six years; within this period, investments in African startups have grown 18x. and Latin America’s 2.8%.

VVSEAI Fund V’s substantial corpus includes a dedicated co-investment envelope of $50 million, which will be utilized to invest alongside the primary fund in startups led by women founders. Their investment scope encompasses key regions such as Singapore, India, Indonesia, Thailand, Vietnam, and Malaysia.

In March 2019, SoftBank Group International made headlines when it announced the SoftBank Innovation Fund, which started out with a $2 billion commitment to invest in tech startups in Latin America. The Japanese investment conglomerate has dramatically ramped up its investing in the region, and so have a number of other global investors.

Embed that finance : Pezesha, a Kenyan-based fintech startup, is flush with $11 million in new capital as it seeks to bridge the gap between access to financial products and what is a “$330 billion financing deficit for the small enterprises that make up 90% of Africa’s businesses,” Annie reports. Christine and Haje. Startups and VC.

In the third and final article in her series on personal health and finances, Megan Hottman shares a tool that helps her stay on course for financial success. She formed her own law practice in 2010 at age 29 and joined EO in 2018. Or perhaps you financed a piece of jewelry that makes you feel confident when you wear it.

General Atlantic, SoftBank Vision Fund 2, Princeville Capital and sovereign wealth funds, ADQ (UAE) and Qatar Investment Authority co-led the round. . The new financing also makes Trendyol Turkey’s first decacorn, and among the highest-valued private tech companies in Europe. The deal marks SoftBank’s first in the country.

Let’s take a closer look at trends in government grants, angel investment and venture capital financings. According to the Center for Venture Research, The Angel Investor Market in 2010 was about $20 billion and funded about 60,000 companies, with about one-third of that capital committed to seed/startup stage companies.

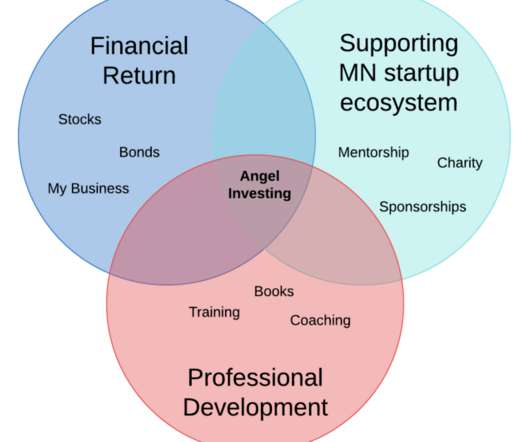

I’m sharing my thought process because perhaps it will nudge some of you to angel invest too! I consider myself a furiously curious person, and angel investing is one of the most rewarding ways I’ve experienced to satisfy this curiosity. My angel investing hobby was making me a better Founder, CEO, and business leader.

venture capital deals, a spike in mega-financings where it’s common to see not only $100M private rounds, but companies that raise two or three types of financings like this in the same calendar year! 5/ The Enduring Allure Of Platform Potential: Revenue is important.

The unprecedented explosion of investment in life sciences over the past decade has resulted in incredible new therapies for patients, strong financial returns for companies and an overall increase in translational research, which is critical to advancing the next generation of therapies. Share on Twitter.

Founded by Sheel Mohnot and Jake Gibson in November of 2019, San Francisco-based Better Tomorrow Ventures ( BTV ) has allocated $150 million to invest in startups at the pre-seed and seed stages. It has also reserved $75 million for an opportunity fund for follow-on investments. The personal finance company went public last year.

I wondered if Softbank's changes in investment strategy had much to do with it, but as the chart shows, they were not a meaningful contributor. Their investment is marked in the black line. Since 2010, the number of round by quarter has followed a periodic growth, with consistent seasonality.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content