This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In the first post in this three part series I described why I believe the VC market froze between September 2008 – April 2009. I obviously don’t have a crystal ball so the economy could fare better than my gut, but here’s why I’m cautious for some time in 2010 or early 2011: Why is the future still so unpredictable?

Greycroft is an early-stage VC. Closing a VC fund in 2009/10 is a major achievement in and of itself. In the intro section of the show we talked a lot about why VC funds are becoming smaller again and where Greycroft fits. CEO hinted to WSJ that it may go public in early 2011. Tags: Start-up Advice. File sharing?

If you want a very quick primer on all the stuff nobody ever tells you about raising venture capital check out this video where Mark Jeffrey & I break it down on This Week in VC. All of this is covered in more detail on the TWiVC video above (and much of it is covered in text on this blog on the “ Raising VC &# tab).

This is where VC comes in and why it’s needed in the industry no matter how much populist sentiment exists against the VC industry. got picked up early without raising a lot of VC. If 2011 & 2012 look like 2010 then the current crop of angel investments will look great. So where are we now? It’s hard to say.

I joined Upfront Ventures in 2007 and took over as co-Managing Partner in 2011 along with the founder, Yves Sisteron. In the end, if you’re not developing a deep bench of talented professionals who keep you on your toes, you’re bound to be disrupted. Yet I’m always thinking about it.

That’s how it felt then and a bit how it feels in May 2011. years ago you’d remember RIP Good Times from Sequoia, which still strikes me as having been prudent advice in late 2008. I hope to offer experiences from being an entrepreneur and being a VC.&#. And 18 months later, in May 2011, I have crossed 422,000 views.

Will you get the TechCrunch bump, the tier-1 VC anointment, followed by great PR firm support and then the NY Times or WSJ story that follows? So as I get around the country speaking at college campus in 2010 & 2011 I have been preaching the same theme. Not every problem has to be a huge VC-fundable business.

I myself coined the term ENIFA (everyone now is a f **g angel) in 2011 but it didn’t stick as well as the term Unicorn did. They now have a strong VC lead from Foundry Group and from experience when you get advice from Foundry it comes with authority, experience, empathy and the right amount of straight talk.

Because my role as a VC requires me to take and endless stream of meetings I long ago decided I need to learn as much as I can from the meetings I attend so I often just ask tons of questions and assimilate knowledge. When I think about what defines us as a VC I think: Operationally knowledgeable / strong startup competence.

By 2011 the market had started to change dramatically. Throughout all of these years I was a full-time VC so Launchpad really came out of evenings and weekends for me. Throughout all of these years I was a full-time VC so Launchpad really came out of evenings and weekends for me. We announced Fund I in 2011.

It’s the one bit of advice I find myself giving most frequently these days, “raise money at the top end of normal.&#. 2007, 2011) and for the hottest of companies and in bad markets for fund raising (2003, 2008) prices test the bottom end of the range. I’m a VC so I have an obvious bias. It was early 2000.

In 2008 I started VC blogging. Ironic to be self-centered while you’re trying to offer advice to others. In 2011 I started using Instagram. In 2007 I started using Twitter and most of my friends & colleagues wondered why people would care what I ate for lunch. I had blogged when I was an entrepreneur.

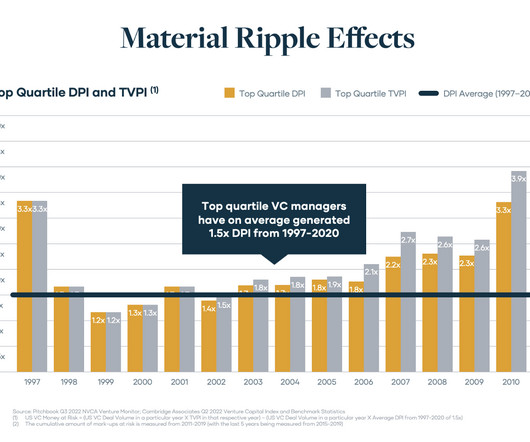

VC dollars are at risk, we conducted a historical analysis of top quartile fund managers over the past quarter century (as far back as we could access reliable Cambridge Associates data). We looked at the analysis in two parts: the 1997–2010 time period and the 2011–2020 time period. since 2011. But what could that look like?

I believe that over capitalizing companies too early often favors the VC. Talking about whether to raise more money or not, their VC allegedly said to them: “If you had more capital, could you get to the future faster? It’s the whole basis of my investment philosophy, which I call “ The Entrepreneur Thesis.&#.

This is where VC comes in and why it’s needed in the industry no matter how much populist sentiment exists agains the industry. got picked up early without raising a lot of VC. If 2011 & 2012 look like 2010 then the current crop of angel investors will look great. So where are we now? It’s hard to say.

Still, as a VC I value proprietary dealflow & long term relationships. I know it was over heated when a deal where I wrote one of the first checks on (as an angel, not VC) went out on AngelList. Mostly, I don’t believe that a VC not being on AngelList is “anti entrepreneur&# – it is not. My personal use.

While Google and Facebook will buy “acquihires” (at least as of Dec 2011), many acquirers hate the idea of buying companies that aren’t profitable. Do you imagine eventually raising VC and trying to build a faster growing company?” It allows you many more exit opportunities. ” Harsh, but reality.

I spoke about how Amazon Web Services deserves far more credit for the last 5 years of innovation than it gets credit for and how I believe they spawned the micro-VC category. I said that I felt that Micro-VCs were the most important change in our industry. It is great for entrepreneurs and great for VCs. I believe that.

Business writer Gordon Pitts pinpoints 2011 as the game-changing year for the Atlantic startup scene. In his book “Unicorn in the Woods: How East Coast Geeks and Dreamers are Changing the Game , ” Pitts recounts how in March 2011 Salesforce purchased New Brunswick-based social media monitoring company Radian6 for approximately $300 million.

James covers the genesis of Ministry of Awesome following the Christchurch earthquakes in 2011, and provides updates on Ministry of Awesome approaches to startup founder support and programming. We’ve got some really incredible people that have joined our team to provide that one-to-one mentorship and advice.

Chris Neumann: I’ve been lucky to have been a part of 5 startups going back to the late-90s, including two that were VC-backed (DataHero and Aster Data). If you could magically give one piece of advice to every founder seeking venture capital what would it be? Hunter Walk: So why venture capital, why early stage, and why Canada?

“I had one cross my desk yesterday where a brand-name VC led the seed, which they are now calling a pre-seed,” Winfield told TechCrunch. On Monday, we’ll run columns with practical advice for exploring both of those scenarios. Patricio Jutard, co-founder and general partner, Newtopia VC. Walter Thompson.

At TechCrunch Early Stage 2021 , a virtual bootcamp experience in two distinct parts, you’ll learn from leading experts across the startup spectrum — including prominent founders ready to share their personal experiences and hard-won advice to help you avoid costly missteps. Talk about awesome exposure!

A great recent example of this was a successful group of entrepreneurs who had created a company that will do $10-12 million in revenue at their system integration business (read: services business) in 2011 after having done $5 million or so in 2010 and $2-3 million in 2009. They wanted advice. That’s the right answer for VCs.

In a post that identifies embedded finance’s top providers and enablers, he offers advice for startups and established brands that are hoping to “earn and build customer loyalty while generating new revenue streams.” ” From startups to Starbucks: The embedded API opportunity.

“We did hear that and I think it’s very poor advice,” he says. There is every likelihood that Zennström’s Atomico would have joined Klarna’s cap table in 2010 if it weren’t for a single line of text published on the VC firm’s website, which read something like, “don’t contact us, we’ll contact you.”

The company started in 2011 and built what I still think is the best free learn-to-code product online. not professional software engineers) Short/Intermittent usage patterns across all users — E.g., they show up for a few weeks/months to learn something, then leave for a while, then maybe come back in a few months/years.

Again, this is highly individualized so no generic advice can be offered. It’s hard for many VCs to get excited about funding a company who is going to compete with somebody who just raised $10 million from an A-list VC (although this can go the other way, also). The market is over-valued in 2011 relative to norms.

So we’d love your thoughts on maybe just advice for companies rebuilding their partnership orgs or they’re developing their sophistication on the ELG front. Then by 2011 or 2012, some of the tech components of the Great Recession had started wearing off and the market started waking up.

I’ve been on the road much of 2012 and part of 2011. As I’ve written about before, You’d Have to be a Big Baby to Complain about Being a VC. One of the most asked questions I get about being a VC who was formerly an entrepreneur is if I ever miss being an entrepreneur? And I’m happy as a VC.

“We did hear that and I think it’s very poor advice,” he says. There is every likelihood that Zennström’s Atomico would have joined Klarna’s cap table in 2010 if it weren’t for a single line of text published on the VC firm’s website, which read something like, “don’t contact us, we’ll contact you.”

For instance, as I’ve previously written , “In 2011, only 28% of Europe’s venture-backed tech deals were seed stage… [but] in 2013 and 2014, roughly half of all European tech venture deals were seed stage.” Remember the “buy low, sell high” advice they were supposed to teach you in business school?

It’s why the first company I ever invested in as a VC – Invoca – just announced a $20 million funding by Accel Partners. The three largest webmail services had over 1 billion global users at the end of 2011. And while this data is from mid-2011 I can assure you that data is not going down. There are 2.9

My advice to entrepreneurs was and is “ when the hors d’oeuvres tray is being passed take two ” (e.g. So I agreed to offer my current thinking on the economy and what it portends for the VC industry & fund raising for entrepreneurs. raise money now to weather any storms).

But I guess you could say the same about VC. Stock market declines would bring back dog days of VC. If you want a comprehensive summary of the industry in this era it’s worth a read: VC Ice Age Part 1 – What Happens When a Market Comes to a Standstill? VC Ice Age Part 2 – Why the Market Started Moving Again?

I had been trading emails & Tweets with venture capitalist John Frankel and we were to meet in person in March 2011 at SxSW to talk about Klout and other investments he had made. Other people were convinced including Kleiner Perkins who lead their $30 million fund raising in 2012 (they had previously also invested in 2011).

SPV-driven funds like Candou face competition from traditional venture capital firms, angel investors, equity crowdfunding platforms, and micro-VC funds. Traditional VCs typically manage large capital pools and invest across a spectrum of startups. Candou stands out by offering greater flexibility compared to traditional VC structures.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content