This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

But until very recently, raising capital for your startup was significantly easier if it was located in the major startup hubs, most notably Silicon Valley. And very little of it is in western Europe where most of our non-US investing has been for the last decade. What makes it easier for USV is our thesis-driven model of investing.

And the loosening of federal monetary policies, particularly in the US, has pushed more dollars into the venture ecosystems at every stage of financing. how on Earth could the venturecapital market stand still? On the one hand, you’re over paying for every investment and valuations aren’t rational. Of course we can’t.

— @jasonlk How the Long Game Has Benefitted Upfront I was thinking about it this morning in particular and thinking about my own personal investment history. sold to Disney for $670 million and since our first investment was at < $10 million valuation we did quite well. Entrada Ventures? —?that

Sometime in the next few weeks, I’ll complete my next investment. It will be the 105th deal out of Brooklyn Bridge Ventures, the firm I started back in September 2012, and it will be the last deal I’ll be making out of my third fund. It will also be my last venturecapital deal.

Why do some embedded analytics projects succeed while others fail? We surveyed 500+ application teams embedding analytics to find out which analytics features actually move the needle. Read the 6th annual State of Embedded Analytics Report to discover new best practices. Brought to you by Logi Analytics.

So here's all the reasons I told him he shouldn't be in: 1) Fund investing is boring. More updates, more casual events, more exposure to portfolio companies, co-investing, etc., Being in a fund is not the same thing as angel investing. Of course, angel investing for most people isn't very fun past the first year.

Most VCs did well academically and had enough career success that a venture firm was willing to give them an investment role or they were able to raise their own fund. Fundamentally venturecapital is about human capital. In the end I know the only true differentiator in venturecapital is the company you keep.

Brooklyn Bridge Ventures , the pre-seed and seed stage VC fund I run in NYC, has invested in 64 companies in the last six and a half years. The diversity is the direct result of our mission—to build the most accessible venturecapital fund in NY. Twenty-five of them have at least one female co-founder.

One of the first things I did when I joined the venture asset class as a lowly institutional LP analyst in 2001 was to build the VC fund cashflow model. Just about every analyst who looks at fund investing has built one. And no, the numbers don't exactly add up--but they're more than close enough for venturecapital.

I’ve made over 100 investments in my career and nearly half of those went into diverse teams. A founder who has a handful of venture-backed friends—successful ones who have raised multiple rounds of capital and who have grown their companies through different stages—has a huge advantage over one that doesn’t.

It's a story that just hit a milestone--a $4mm round of venture funding that I'm ecstatic to say Brooklyn Bridge Ventures just led. But just because you could see them everywhere doesn't make them an obvious venture bet--nor does it tell the story of how the round even came to be. Still, I followed the space closely.

After checking out The Information's "open dataset" on diversity in venturecapital , I felt pretty disappointed. I went back and calculated the number of companies in the first Brooklyn Bridge Ventures portfolio who have at least one founder who is female, from an underrepresented minority group, or LGBT.

Staying on top of the early stage investing world requires a lot of reading. One of the biggest trends we witnessed over the past few years is the rapid pace of new early stage venture fund formation combined with significant growth in the amount of capitalinvested.

However, women – and especially minority women – often face institutional and systemic challenges including obtaining funding for their ventures, which can make the climb to the top slower and more difficult. Despite the growth in women-owned businesses, venturecapital is still funneled to mostly male-owned businesses.

We love capital efficiency until we love land grabs until we abhor over funding until we get huge payouts and ring the bell for more funding until we attract every non-VC on the planet to invest in startups until it crashes and we start the cycle all over again none the wiser. What do I know about venture? VC funding.

Those values, on a schedule of investments we publish to our investors every quarter, flow through to our financial statements and capital accounts and establish how much an interest in our partnerships are worth at that time. If you might lose money on an investment, it is always best to signal that ahead of time.

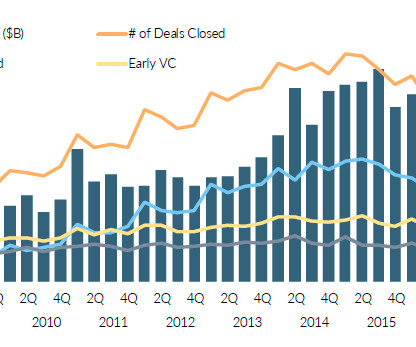

Seed investments are down by any measure (funds, deals, dollars) over the past 3 years in deals < $1 million AND in deals between $1–5 million. Over the past month a colleague ( Chang Xu ) and I sifted through data on the venturecapital industry (as we do every year) and made a bunch of calls to VCs and LPs to confirm our hypotheses.

I’ve heard a lot of people question whether there is too much money in venturecapital chasing too few great deals. Others believe that new business models are emerging that could replace venturecapital all together. We’re in a new tech bubble!” some have pronounced. More on that later. Follow the money.

Today's top founders will undoubtedly start something new in the future, but they won't make up the majority of innovators going forward--just as prior generations of venture backed founders don't make up a majority of those who are succeeding today. I didn’t say ventureinvesting was easy—but at least we got a look.)

There is a lot of criticism of venturecapital in web3. Bitcoin did not have or need venturecapital. Ethereum did not have or need venturecapital. So why would any web3 project need venturecapital? But venture capitalists do, particularly good, experienced, and confident venture capitalists.

Photo by Scott Clark for Upfront Ventures (no, Evan is not standing on a box) Last year marked the 25th anniversary for Upfront Ventures and what a year it was. We are excited to share the news that we have raised $650 million across three vehicles to allow us to continue making investments for many years ahead.

Today we’re announcing that my partner Kara Nortman is becoming Co-Managing Partner at Upfront Ventures and I can’t tell you how thrilled I am to welcome her to her new role. She worked for 5 years as a VC at Battery Ventures and co-headed M&A at IAC working with Barry Diller. She had all of the skills and traits we sought?

In venture, it’s all about getting an opportunity to make partner and being included in the carry—the economic upside of a fund. It would be a directive to literally invest in the talent base—to create a path for influence and economic mobility within a firm. Not all hires, however, are made equally.

Companies in every sector are investing in the latest technologies with an eye toward winning in their markets with AI, said Misha Herscu, CEO and co-founder of Cake. The post Googles early-stage AI Fund Gradient Invests in Cakes Open-Source AI Platform for All Businesses appeared first on American Entrepreneurship Today.

Learn what investors want to hear that triggers their investment decisions. Marc Andreessen, co-founder of Andreessen Horowitz, a leading venturecapital firm, says, “The thing that gets me most excited is the founder whos obsessed with solving a problem that matters, and is determined to keep going no matter what.”

Since the beginning of modern venturecapitalinvesting — a relatively nascent asset class — the industry has been biased toward funding what it knows best: founders with familiar demographics (white, male) in familiar geographies (Silicon Valley).

Those same dynamics apply to fund investing. However, if you start an investment fund and collect and lose other people’s money, that’s a very different story. If you lose your money betting on a startup, you have no one to blame but yourself.

Paul Martino, General Partner at Bullpen Capital. During our recent Dreamit Kickoff week, Bullpen Capital Founder and General Partner Paul Martino ( @ahpah ) spoke with our Spring 2020 cohort about the state of the VC ecosystem in the current economic crisis. Will a financial crisis affect how venture funds deploy capital?

At this years Bark Tank Pitch Competition , eight teams took the stage to pitch their ventures to a panel of expert judges, competing for a record $150,000 in prizes. Chef, entrepreneur, humanitarian, and my friend Jos Andres put it well: investing in young entrepreneurs is investing in solutions. startup ecosystem.

Via TechCrunch by Arman Tabatabai: Venturecapital has been flooding the various subverticals under the robotics umbrella in recent years, and the construction space is one of the largest beneficiaries. One of the most common areas of attention respondents highlighted were startups focused on construction and manufacturing.

The venture asset class seems to have already decided that AI is the next great investment opportunity, but I’m not so sure it’s going to disrupt business and create the across-the-board wealth that has been predicted. I got to see all of the top VCs pitching their funds.

Long before diversity and inclusion became buzzwords, we decided to make venturecapital inclusive from day one at 500 Startups. The post Why Investing in Female Founders Matters Now More Than Ever appeared first on 500 Startups. Since 2010, we have expressed our commitment to those values in multiple ways.

One of the biggest challenges faced by early stage investors is to assemble a portfolio of investments that in aggregate return more than 2 times the original amount invested in the total portfolio. In other words, for every dollar you invest in your portfolio, you want to get two dollars back over time.

Here are some common red flags for venture investors: Red Flag #1 : Ask isn’t tied to specific fundable milestones. On the other hand, if your ask offers investors too little equity, the investors won’t have enough skin-in-the-game to achieve meaningful or target returns on their investment. Apply to our upcoming program.

a nonprofit dedicated to fostering the growth of startups and entrepreneurs in Oklahoma, is proud to announce surpassing the $100 million mark in total investments. These investments, collectively over $100 million, have provided vital early capital to help startups throughout the state to thrive. i2E, Inc., About i2E, Inc.

Practice Your Pitch and Save Your Social Capital Entrepreneurs benefit tremendously from practicing their pitch and Q&A. For instance, when I fed it the executive summary of my last venture, I expected generic questions like: “Who is your competition?” and “What are your management team’s qualifications?”

That was a question posed to me by a new analyst at a venturecapital fund. While there are lots and lots of really kind, generous people working in venturecapital--the recently retired Howard Morgan, Hunter Walk, Brad Feld, and Karin Klein for example--it's really tough to argue that there isn't widespread jerkery.

Private equity firm Rotunda Capital Partners focuses on transforming family-founder-owned companies into data-driven platforms that lead to accelerated growth. The firm’s latest investment into family-owned Mama Lycha, the leading provider of branded Latin American foods, was announced this week.

The Fantasy Cash Flow Model When I was an analyst at the General Motors pension fund, investing in VC funds, I had to build a model of how I thought they would perform. It started out with initial investment size, pricing, and outcome behavior for each deal and then it made a prediction around the distribution of outcomes.

Revolution VenturesInvests in Kashable, the Fintech Leading the Socially Responsible, Employer-Sponsored Credit Movement The $25.6M Revolution Ventures is thrilled to partner with Kashable and help the team accelerate its vision to help all working Americans forge a path to financial security.

Sam Altman of YC recently pointed out that pulling back during the downturn in 2008 would result in several big misses: In October of 2008, Sequoia Capital—arguably the best-ever in the business—gave the famous “RIP Good Times” presentation (I was there). These sound fundamentals drive the venturecapital market over the long term.

Seed funding came from venture firms committed to deep tech. The $8 million seed round brings the startup’s total investment in the company to $10 million. The investment was co-led by Harpoon Ventures and Refactor Capital, with participation from Pathbreaker, BoxGroup, Seraphim, Plug and Play, Impact First, and Climate Capital.

Matt Johnson is the founder and Managing Partner of Johnson Venture Partners, a micro venturecapital fund investing in seed and early-stage startups. Matt has invested in over 40 venture-backed companies throughout 15 years of early-stage investing experience.

Jeff Berman is General Partner at Camber Creek , one of the first venture funds dedicated to real estate technology and the built world. The team owns, operates and manages over 150 million square feet of real estate, making Camber Creek one of the biggest value-add venture partners for real estate tech startups.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content