This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

One of the biggest trends we witnessed over the past few years is the rapid pace of new early stage venture fund formation combined with significant growth in the amount of capital invested. A decade or two ago, most of the new funds were traditional VC funds located in technology hubs in the US and a few other countries around the globe.

Of the first four investments I made as a VC in 2009, two have exited and two (Invoca & GumGum) still are independent and likely to produce $billion++ outcomes . The abundance of late-stage capital is good for us all. My first ever investment as a VC was Invoca. The abundance of late-stage capital is good for us all.

Gregg Johnson, CEO of Invoca For the first 5 years or so after I became a VC I didn’t talk much about what I thought a VC should be excellent at since frankly I wasn’t sure. It’s easy to think the role of a VC is to have strong opinions about markets, trends, tech dynamics and so forth. The role of VC is sparring partner.

Dreamit Urbantech Managing Director Andrew Ackerman recently sat down with Jeff for a wide-ranging conversation on real estate tech, and a large part of that conversation focused on what founders can do to successfully raise venture capital from real estate tech investors. Has the founder done his homework before his pitch?

At our mid-year offsite our partnership at Upfront Ventures was discussing what the future of venture capital and the startup ecosystem looked like. No blog post about how Tiger is crushing everybody because it’s deploying all its capital in 1-year while “suckers” are investing over 3-years can change this reality. What is a VC To Do?

They count on me to be a good steward of their capital, and to take reasonable and appropriate risk with the expectation of a certain level of returns. That also means that I need to act in a way that ensures my ability to get future opportunities to invest their capital in attractive deals. Venture Capital & Technology'

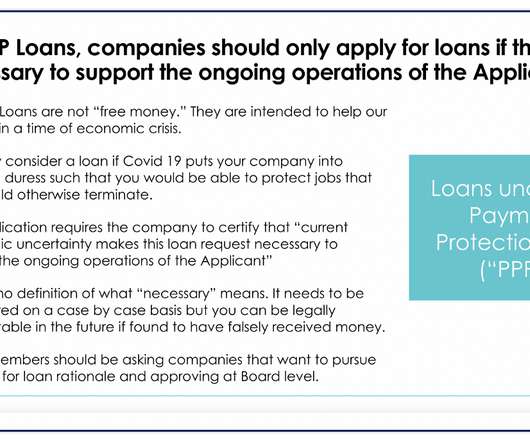

But I have been in close contact with the NVCA, many of the major law firms and many of the major VC firms. If your US-based business is adversely affected by Covid-19 such that you would need to lay off employees imminently and having access to capital would enable you to keep more employees on the payroll then you might be eligible.

The venture capital screening call is an important step to get right in due diligence. Learn how to pass a VC associate screen in under 10 minutes! To get to partners, often you’ll have to go through the associate first. These are easy tips if you know what to look out for. These are easy tips if you know what to look out for.

Brooklyn Bridge Ventures , the pre-seed and seed stage VC fund I run in NYC, has invested in 64 companies in the last six and a half years. The diversity is the direct result of our mission—to build the most accessible venture capital fund in NY. Twenty-five of them have at least one female co-founder. Fifteen had co-founders over 40.

” Today I want to talk about how a VC thinks about equity pricing on your round and particularly if you’re coming off of a convertible note. So how DOES a VC think about financings at early stages? ” That is a problem for the founder and the VC. And the VC isn’t happy because he or she owns 17.4%

VC firms see thousands of deals and have a refined sense of how the market is valuing deals because they get price signals across all of these deals. What was the post money on your last round (and how much capital have you raised)? So why does a VC ask you? In the first place they’re looking for “fit” with their firm.

Time and time again i hear about founders that have bigger egos then anything else rejecting offers from top tier VC's (like YC ) and eventually leading thier companies to fail. If you do get and offer from top US VC's take them, dont be greedy and stay humble. Dont have a big ego.

How long does it take from first meeting a VC to getting cash in the bank? Here were the results: I would guess that getting a third of my deals from events is probably disproportionately high compared to other seed investors on the east coast--and that my VC intro percentage is probably somewhat low. Venture Capital & Technology'

million of initial capital with all its fees and stuff, and you''ve got about $6 million of gains. A fund that returns three dollars for every dollar of capital invested would be a $2.4 Venture Capital & Technology' Subtract the $8.3 That''s a little over a million dollar gain for me personally. million return for me.

But until very recently, raising capital for your startup was significantly easier if it was located in the major startup hubs, most notably Silicon Valley. It takes a long time, at least five years and more likely a decade, to know how changes in the startup economy and venture capital will play out. And we are doing exactly that.

After checking out The Information's "open dataset" on diversity in venture capital , I felt pretty disappointed. Most people need a little bit of capital to bring a product to market--or they're an engineer. VCs have an inflated sense of the value of their own time.

I’ve heard a lot of people question whether there is too much money in venture capital chasing too few great deals. Others believe that new business models are emerging that could replace venture capital all together. We’re in a new tech bubble!” some have pronounced. Valuations are out of control” is the mantra of others.

And here we are, with a 24×7 global marketplace for crypto assets that has a market capitalization of over half a trillion and daily volumes in the hundreds of billions. This pales in comparison to the legacy capital markets, but that is always the case with a new entrant on the scene. And many/most do that. USV TEAM POSTS:

So I asked a few founders that I've worked with and they mentioned a word that struck me--because I've never heard any of the hordes of people in my inbox asking for internships, VC job recommendations and advice, etc. I think of venture capital as a service business. mention about themselves. Generosity.

As policy makers around the world seek to mitigate the economic shock from this pandemic, one less obvious but powerful place to look are working capital flows. We also need our capital markets to work so actions like the Fed is taking are necessary and important.

I always tell founders … “An investors job is to deploy capital and make a return. The typical VC process is as follows: They say there are three rules in property: Location, location, location. Same with VC. Somehow many first-time founders equate “sales” with something that is beneath them. these are simply guidelines.

The last thing you want as either a founder or even a VC is to have an investor get stuck with you when you're not on the same page about expectations. I recently met up with an investor who I'm not totally sure is a fit for my second fund , so it was important to me that I was upfront about all the reasons why he shouldn't come in.

The partner at the fund, the VC, gets to do the fun part—the meeting with founders, vetting deals, negotiating, helping, etc. Having a better overall portfolio of venture capital by adding funds into the mix. In fact, that number is probably even more than the average VC fund has the bandwidth to make. So what’s the point?

I became a VC 12 years ago in 2007 when the pace of deals was much slower. As I was trying to figure out the role I wanted to play in the VC world I decided I wanted to focus on businesses that were building deeply technical products to solve problems for business users. VCs have different views and strategies on this.

Now let's take a closer look at capital allocation strategy and the life cycle of a venture fund. In Part I of this article we discussed several key concepts of fund investment strategy and how funds are categorized, whether it be by industry, geography, stage, specialty (e.g. social impact, corporate, etc.) or some other criteria.

Those values, on a schedule of investments we publish to our investors every quarter, flow through to our financial statements and capital accounts and establish how much an interest in our partnerships are worth at that time. Every quarter our firm goes through a process to value our entire portfolio.

That story actually begins about eleven or twelve years ago, with a little bit of VC mentoring. I was working for the GM pension fund, an institutional LP, as an analyst, doing a research project on consumer private equity and venture capital investing.

That was a question posed to me by a new analyst at a venture capital fund. While there are lots and lots of really kind, generous people working in venture capital--the recently retired Howard Morgan, Hunter Walk, Brad Feld, and Karin Klein for example--it's really tough to argue that there isn't widespread jerkery. So what gives?

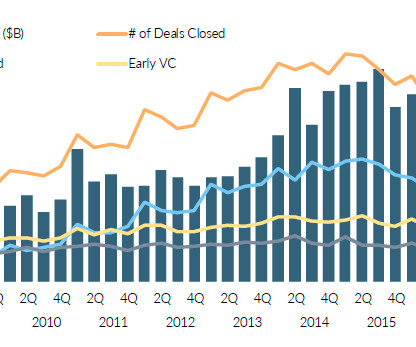

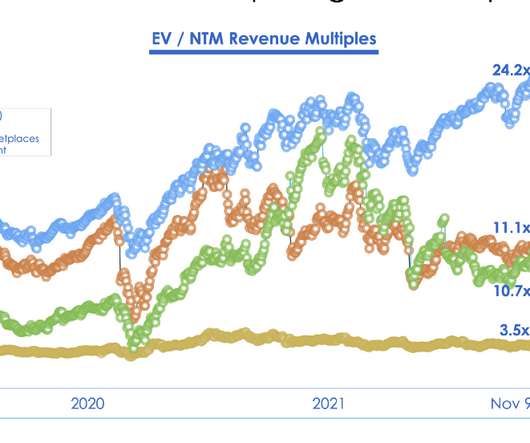

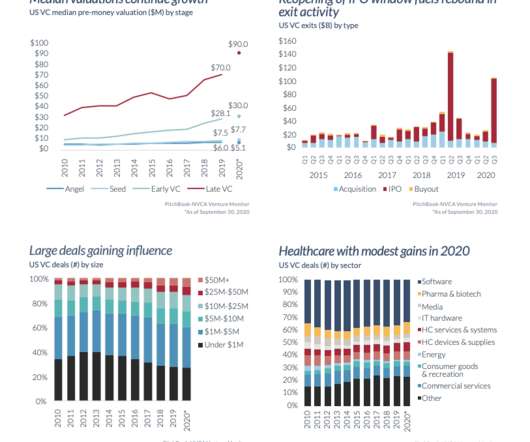

The NVCA and Pitch Book are out with their Q3 report on the VC industry and what they report is that the VC industry continues to be very active throughout the pandemic. The massive expansion of later-stage private capital continues unabated. The massive expansion of later-stage private capital continues unabated.

To a VC, $50,000 a pre-sale isn’t really that much. VCs are less interested that you sold 10 customers, 20, or 100—they want to understand how many you’re selling per week and whether or not that kind of pace would be profitable for your sales & marketing efforts. That’s why we invest in a portfolio.

Over the past month a colleague ( Chang Xu ) and I sifted through data on the venture capital industry (as we do every year) and made a bunch of calls to VCs and LPs to confirm our hypotheses. As a result of the IPO window shifting we saw a massive inflow of public-market capital into the latest stages of venture.

I believe that the next generation of top companies are far more likely to be founded by people not on VC radars today. Last week, we ran Fall Fundraising Days , which featured 11 NYC events on raising capital that 800+ individuals attended across the week.

There have been a lot of calls for VC firms to make more hires from the Black and Brown community, as well as to hire more women. There are lots of problems with access to venture connections that account for some of this, but how you invest and pay your own team is the one indisputable thing that is in a VC firm’s control.

There is a lot of criticism of venture capital in web3. Bitcoin did not have or need venture capital. Ethereum did not have or need venture capital. So why would any web3 project need venture capital? That’s why you might want to take venture capital for your web3 project. It is a good question.

There are more active VCs alive today than have ever existed in the history of modern human existence—and that dates back 300,000 years! This is something I talk about a lot with my VC coaching clients. That means a lot of competition for the best deals and more difficulty in standing out. The question is what to focus on.

Investment experience (5 years a VC at Battery Ventures). As I like to say (and as Kara humbly hates when I do so in front of others) … she has a much better resume to a venture capital partner than I do. Upfront Ventures VC Industry' M&A experience (Morgan Stanley and later co-headed M&A for Barry Diller at IAC).

No VC will be so naive as not to see straight through it. When I first became a VC, seed rounds were typically $500k – $1.5 There weren’t a lot of seed funds in 2007 so this was often done by angels, funding consortia or sometimes early-stage funds that existed then (First Round Capital, True Ventures, SoftTech VC, etc.).

I spoke at Michael Kim’s excellent annual Cendana VC/LP conference today. One of the points I tried to make is that as venture capital investors as an industry we seem to have a healthy disdain for public market investors. What is your revenue growth rate and what does this imply about your number of months of capital remaining?

Part of the antidote for startups: employing a more prudent approach to raising capital and curating a diverse investor base. To shed additional light on this issue and its ultimate impact on startups, I partnered with the Center for Real Estate Technology & Innovation to ask proptech founders about their capital and strategic partners.

Any VC will tell you that the ones they said yes to, they mostly got there right away—and that there are very few “maybe” deals that get tipped over the fence. Or that venture capital is a meritocracy? We know what the racial and gender wealth disparity looks like: This is a lesson taught to be by Jewel from Collab Capital.

I was a huge Fab.com buyer in the early days when we backed it at First Round Capital. But Fab fell into the trap that many companies who go down the VC route fall into--too much money, too soon, and growing too fast. Venture Capital & Technology' How I got to this investment was another long term story.

SPACs are publicly traded “shell companies” that raise capital in an IPO process and then use that capital to merge with a privately held business. For most of my career as a VC, the IPO has been the holy grail. I don’t take as much offense to this situation as others in the VC business have.

There has been this narrative about investing in VC funds that you have to get into the top quartile (25%) or possibly the top decile (10%) in order to generate good returns. I have heard that for as long as I have been in VC and probably have written it here a few times. As you can see, investing in VC funds can be very profitable.

Unlike venture capital funds, they don't make money directly off the multiples of their return. What's worse is that this end of the market is even affecting early stage VC mindset. If you're a VC and you think for a second that whether or not Square pricing at $2.9

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content