This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Marc Andreessen kicked off another great debate on Twitter last night , one that I’ve been talking about incessantly in private circles for the past 2-3 years – what actually IS the definition of a seed vs. A-round. No VC will be so naive as not to see straight through it. .” My personal definition?

The VC market has right-sized (returned back to mid 90′s levels & less competition). But it still takes VC to scale a business (thus large capital into industry winners like Uber, Airbnb, SnapChat, etc). But it still takes VC to scale a business (thus large capital into industry winners like Uber, Airbnb, SnapChat, etc).

I usually direct people to this post --still hanging atop the search rankings for " How to be a VC analyst" years later. In VC, no one''s investment gets bought on the first day, or the second day, or the third day. Well, let me be the first to tell you. 5) It takes a long time to be successful. And most of all, I love people.

I told my friend that I felt that in 2014 too many new VCs feel the pressure to chase deals, to be a part of syndicates with other brand names and to pounce on top of every startup whose numbers are trending up quickly. I know I can’t be in every deal and I know that the easy part of being a VC is writing the first check in a deal.

Learn how to pass a VC associate screen in under 10 minutes! It means you haven’t properly framed this deal in the associate’s mind and that makes it hard for us to come to a definitive conclusion. These are easy tips if you know what to look out for. Do your research You should do your research before talking to an associate.

*. What is the role of a VC for entrepreneurs? I suppose it can be different for every founder and for different VCs but I’d like to offer you some context on what I think it is and it isn’t. They are unique to you and not to each other situation that VC has faced. ” I responded. Your decisions are unknowable.

If you want a very quick primer on all the stuff nobody ever tells you about raising venture capital check out this video where Mark Jeffrey & I break it down on This Week in VC. All of this is covered in more detail on the TWiVC video above (and much of it is covered in text on this blog on the “ Raising VC &# tab).

By definition?—?I’m I’m over-paying for every check I write into the VC ecosystem and valuations are being pushed up to absurd levels and many of these valuations and companies won’t hold in the long term. However, to be a great VC you have to hold two conflicting ideas in your head at the same time.

I spoke about this more in depth in these two posts: 4 things I look for in an investment & how to manage VC relationships. Note that “performance&# on my chart is a loose term for my definition of perceived progress that can take the form of product, customer adoption, employees, investors, press or whatever.

I became a VC 12 years ago in 2007 when the pace of deals was much slower. As I was trying to figure out the role I wanted to play in the VC world I decided I wanted to focus on businesses that were building deeply technical products to solve problems for business users. almost be definition you should be scratching your head.

I can definitely think of a few people I met with and said, "Well, that person was kind of a jerk" or they just had a bad personality--and they went on to build seemingly successful businesses. You''ve been in VC long enough to see lots of different funds, partners and deals. I think I''ve been good about that so far.

” This is a frequent theme of mine when asked to speak to audience about the VC industry. And this is fueled by the VC culture in Silicon Valley. I was recently talking to a VC about a business I was looking at and I was asking whether he found the business interesting, too. It is VC math, like it or not.

.” From the hyperbolic Jason Calacanis weighing in that “The petty VC’s did everything to deride [Naval, the co-founder of AngelList]” as though the industry was collectively s g its pants that AngelList was going to put us out of business. This is the same way VC firms, by the way. VC Industry'

Does the VC think that a designer needs to be on the team from day one if you’re going to build a better version of Instagram? Does the VC think that a machine learning engineer needs to be there to build a real version of Tony Stark’s Jarvis? Let’s first talk about the definition of a co-founder. That’s fair.

But last week I noticed a blog post by a woman, Tara Tiger Brown, that asked the question, “ Why Aren’t More Women Commenting on VC Blog Posts? She has a quote from literally every major VC from whom you’d want to hear. ” [it's short, you should read it]. Please watch this. Every single one.

and even though by definition that means the majority of our dollars are invested outside the area, that still makes us meaningfully different from the ten other Sand Hill Road funds this LP might be speaking with. We’re definitely not a “regional investor” but we do have some comparative advantage in a good portion of our deals.

I was having a conversation last night with another VC who was suggesting I monetize the pro-ratas that I don't take by creating SPVs. It's definitely not the kind of relationship I want to have as an investor. But you could charge fees or at least carry for that. You're leaving money on the table!"

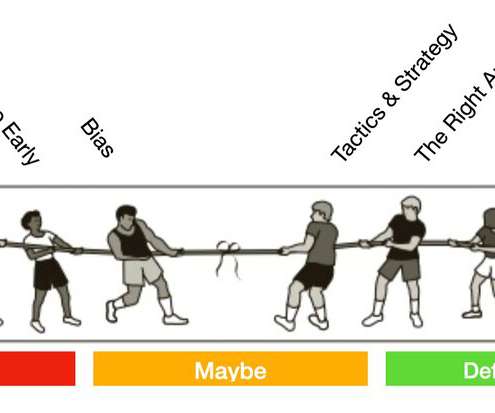

Any VC will tell you that the ones they said yes to, they mostly got there right away—and that there are very few “maybe” deals that get tipped over the fence. Here’s the way I look at the math: Let’s go over the structural bias first—the “pipeline” that happens before you ever even get near a VC. First is network bias.

Since then, I’ve founded several startups, was employee #3 at a $65m VC firm in San Francisco, and realized that there is a similar phenomenon to what Robert Kiyosaki is talking about in Rich Dad, Poor Dad currently occurring in Silicon Valley. Wealth My definition of rich is having a passive income that’s greater than your burn.

I’ve been meeting with LPs (those who invest in VC funds) over the past year and discussing trends I see in the market and where I think we need to be as a firm to be near to and meet the needs of our customers. I think NY has always – by definition – been urban. These days it’s Santa Monica and Venice.

Dan asked Fred about “generational change” at USV and in the VC industry more broadly. Greg joined a bit earlier so has had more time to start to shape our investment philosophies and the strong opinions, well-through-through positions have been a breath of fresh air and definitely started to make changes in our thinking.

Ok, back to the VC content marketing. As a result I’ve seen hundreds of VC decks, all certain they will be among the top performers. What’s my needle magnet definition? The idea that it’s nearly fruitless to blindly search for a single small object when it’s located in a vast container.

There was a time not too long ago when VC bios read "Fab investor", "Quirky investor", and "Gilt investor". VCs can provide a useful piece of advice at a key moment--or help make a key hire, but the day in and day out grind is done by the work of the founder and the team, and they deserve 99.999999% of the credit. No one is perfect.

That means you actually have a *better* shot, statistically, of getting VC investment at these firms, statistically, once you actually pitch. If you go for people with some experience and insight, you are definitively going to get more females. Once again, that''s all stats and doesn''t really explain anything.

It’s when the noise stops and you can actually get customer attention, press articles and VC meetings. Poorly implemented this category was the definition of shelfware. It’s where the truly innovative separate themselves from the pack. It’s when the game slows. It’s when you separate the wheat from the chaff.

We are often asked how companies get funded, why VCs make the decisions we make and what we’re looking for in entrepreneurs. I think this is a Seriously great example of how this process works for at least one VC – Upfront Ventures. So this was definitely an introduction I was going to take. Domain Knowledge.

You’d be surprised how many firms are “dictator VCs” – even those that don’t formally acknowledge it internally. When you’re newer in VC many partners choose to play it safe, doing smaller investments and not trying to bet on something that a “far out” risk. ” Guys?

I’m enjoying being a VC. I thought I’d talk a bit about the differences I’ve experienced between being an entrepreneur & a VC – you know, from “both sides of the table.&#. I’m sure everybody has their own definition of the attributes of an entrepreneur. VC meetings going well. 2 million in VC.

But in my experience as an entrepreneur and now spending my time amongst investors I can generalize that almost all VC investments in early stage technology & Internet investments come down to just four key factors. Everyone has their own definition of momentum (user numbers, revenue, channel partners, biz dev deals, whatever).

It’s in an area that has no hardware and no software and definitely isn’t a company you’d read about on TechCrunch. Fred Wilson said it best in his post about loss ratios in VC. I think the VC industry tends to pressure new entrants to feel like strategy consultants did. VCs don’t need to be perfect.

Just don't go picking someone who really doesn't compliment you just because it's some kind of VC rule. I've heard a lot of VCs tell founders they need co-founders--and that they wouldn't look at a business at a very early stage without a co-founder. The same holds true for VC funds.

The definition of Exit Strategy from Investopedia: “The method by which a venture capitalist or business owner intends to get out of an investment that he or she has made in the past. But it’s also not smart to go into a meeting having just achieved product-market fit and tell an investor that you plan to IPO.

I guess this is the ultimate definition of implementing a business model when you’re not clear on strategy! If it’s the former your company will definitely start to top out at some point. I sometimes see VCs debate ad finitum about a company’s strategy. My take on his argument is this: 1. Markets decide.

What this tech definitely does is that it expands the size of the creator market. As it is, I’m a paid Canva user and you definitely wouldn’t have counted me in that target demo as narrowly defined by Adobe’s core audience ten years ago. That being said, I’d hate to be a stock photography model these days.

This is the definition of “Why Buy Anything?” So understanding the stage of a VC matters. Also, you need to consider the type of investments each VC does. Finally, the same rules apply for VC firms raising money from LPs. Nothing is worse than maybe or not knowing. ” You have a problem that I can fix.

The definitive article about 33 Flatbush--the kind of commercial building you would drive by a million times without thinking twice-- was written in the NY Times a few years ago. It's the kind of place you just don't find in Manhattan, and definitely don't find in Silicon Valley. 33 Flatbush. 10 Jay Street. via Brownstoner.

Raise a big VC round – yeah! I had foregone my VC term sheets to accept an offer yet I knew it wasn’t 100% probability to close – it never is. Surreal, it definitely is. I know it’s not what it used to be, but news flash – it’s still a million dollars! Five million? Upside scenarios.

The thing we thought was happening with robotic investments is definitely happening by Brian Heater originally published on TechCrunch A proper bounce back, on the other hand, seems inevitable, but only those with high-powered crystal balls can say precisely when.

Lastly, your city needs to be livable—and that definition is changing. In 2005, it was a risky bet to join Union Square Ventures and plant my VC career here in NYC. It wasn’t until I helped Foursquare raise their seed round in 2009 that many outside VCs even took notice of NYC. They’re less impactful on a year to year basis.

Signaling risk happens when a VC chooses to not do pro rata, or follow-on investing, in an existing portfolio company. The earliest investors are rethinking signaling risk, dilution and, most surprisingly, the worth of a traditional demo day. Let’s start with a juicy topic: pro rata.

By definition you will either get a crappy SI promising you they will move mountains or a great SI that gives you their C-player team. So I’m not endorsing your building your entire company around professional services ( although I think that’s a fine strategy for many non VC-backed companies ) but rather not to avoid it.

Recently I wrote a post arguing to make the definition of a Startup more inclusive than that to which Silicon Valley, fueled by Venture Capital return profiles, would sometimes like to attach to the word. Elect 1-2 representatives and even invite a local VC to invest personally and sit on the investment committee or be an advisor.

It''s a solid exit to a company that has lots of revs, is growing, and together will form a very formidable player in the data backup space--one that can definitely be a public company in the next couple of years.

And yes, VC’s, too. Negotiate directly with your VC or acquirer with lawyers present in the room. VCs : VCs are often on your side and usually act in an ethical manner. You can sometimes leverage your VC in a “bad cop&# negotiation with a buyer. What might the VC do against your interest?

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content