This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Many people bandy about the definitions of “disruptive technology&# or “the innovator’s dilemma&# without ever having read the book and almost universally misunderstand the concepts. It should affect how you think if you are an incumbent but also if you’re a startup. It is often LESS performant.

Many entrepreneurs in Silicon Valley believe that the financial services industry in the United States is “ripe for disruption. ” First, they believe that the current offerings from the financial incumbents are lacking. Once you have the assets, all the disruptive things that Silicon Valley types want to do will be easy.

I’ve been involved with several startups where a giant incumbent attacks you and tries to sue you out of existence. And the giant gets disrupted precisely because its cost structure to serve its customers and its cash cow, high-priced offering makes it nearly impossible for it to try compete. And what prompted this lawsuit?

If you read Reid Hoffman’s important book, “ Blitzscaling ” you’ll realize that in some markets that are large, global and being disruptive sometimes being first to global scale can be more important than short-term unit economics. Last year I pointed out that software would help build competitive moats and we’re already seeing that.

We look at huge markets where there are large incumbents that might not be incented to innovate or react to what they perceive as an insurgent. That’s why Revolution was so supportive of Revolution Money, which sought to break up the troika that controls consumer finance. I run Revolution’s VC investments.

Recently, there’s been rapid digitization of this market , with several startups upending incumbents such as classifieds and hoping to define the new era of used-car-sale platforms. According to the founders, Sylndr also plans on providing seven-day money back guarantee, warranty and availing flexible financing options to users.

Monzo’s culture of customer obsession allowed it to use the crisis to thoughtfully build a beloved consumer and SMB product that has changed personal finance in the UK. 2 Incumbent banks miss the mark in two crucial areas: The banking experience has not evolved to match modern consumer. This did not happen by magic. expectations.

The key purpose of being end-to-end is to deliver an even better value proposition to consumers relative to incumbent alternatives. The end-to-end approach makes the most sense when disrupting very large markets. At their core, these companies are facilitators, matching consumer demand with existing supply of a product or service.

This works for some, but too often founders find themselves diluting their equity to unrecoverable portions rather than considering other financing options that allow them to hold on to their company — options like debt capital. People tend to think that category creation is less risky than incumbentdisruption.

At TechCrunch Disrupt, Houseparty founder Ben Rubin emphasized decentralization as Web3’s central feature. In conversation with reporter Taylor Hatmaker, Rubin said NFTs show that individuals can benefit from Web3 adoption, while decentralized finance and cryptocurrency trading are more commercialized forms. In today’s Web 2.0,

“Challenger” startups in banking and insurance have upended their industries, and picked up significant business, by building more customer-friendly tools and services — more personalized, easier to access and usually competitively priced — than those typically provided by their bigger, incumbent rivals.

“Investors are putting a premium on growth in the context of profitability, and we’re growing exceptionally fast because we’re able to profitably serve customers who aren’t being well served by incumbents,” said Sean Harper, CEO of Kin. To learn more, visit www.kin.com.

A recent ZDNet piece reaffirms that the AI edge chip market is booming, fueled by “staggering” venture capital financing in the hundreds of millions of dollars. He has a deep history of investing in deep tech startups that have gone on to disrupt industries across AI, data, semiconductors, among others.”

Just over five months after raising a $9 million seed funding round , Latin American fintech Pomelo announced today that it is raising $35 million in Series A financing led by Tiger Global Management. The startup was founded earlier this year to build a fintech-as-a-service platform for Latin America.

” Going up against incumbents. Third-party providers, mostly fintechs, have tried to capture some market share from these incumbents. Wave, however , wants to disrupt it. Whereas the incumbents mostly focus on USSD (although there are provisions to use applications), Wave is solely app-based.

It will be interesting to see how newer entrants in the SaaS banking-platform space disrupt what are, effectively, becoming incumbents in their own right: Mambu is now approaching 10 years old (it was founded in 2011). That could lead to consolidation, too.

The financing marks the company’s first ever institutional funding. In a nutshell, Geopagos feels it is in the ideal position of being able to serve as the software enabler that can retrofit incumbents like large banks and launch the enablers like fintechs. Endeavor Catalyst also participated in the financing.

It also plans to soon offer embedded finance products. Additionally, Melonn works with a range of transportation providers, including incumbents such as FedEx or DHL and last-mile startups, to reduce shipping times and costs. . And in January, fulfillment is up 20% compared to November of 2021. So, just how does it work?

Larger banks and other financial service providers are getting a lot more serious when it comes to competing with upstarts that are disrupting their businesses with fresher approaches and newer technologies. We want to be closer to companies’ larger digital transformation programs.”

Embedded finance — where financial services companies and others bring in different kinds of fintech technology by way of APIs to enhance their own offerings with more data and functionality — remains a growing opportunity, both to help fuel new business and to help incumbents get up to speed with their disruptors.

General Atlantic doubled down on Klar , leading its latest financing in addition to its $70 million Series B last July. One advantage for Klar, according to Möller , is that its “cost to serve a user” is about 1/20 of what the incumbents pay. I tie it back to complacency from the incumbents. he told TechCrunch.

Entrepreneurs saw this as an opportunity to disruptincumbents, and soon there were lofty claims that everything about the industry was about to change. Many like to refute the underlying disruption by pointing to public valuations of insurtech firms, some of which are down as much as 85%-90%.

With a large population, Pakistan is geographically smaller, well-connected with fewer provinces, has lower regulatory barriers and doesn’t have strong incumbents,” Khurshid, who is originally from Pakistan, said via email. Catherine Shu reported on C2 Ventures ’ second $20 million fund targeting startups disrupting legacy industries.

When Daniel Simon sold Bread , a consumer purchase finance and payments startup he’d co-founded, to Alliance Data Systems for over $500 million late last year, he quickly set his sights on building another startup.

A number of fintechs have popped up as of late aiming to disrupt the traditional model of evaluating an individual’s creditworthiness. It’s raising a $30 million Series B, led by TransUnion — one of the largest incumbents in an industry that Spring Labs is looking to shake up. Spring Labs is one of them.

million seed round to further its insurance payments platform that combines financing, collections and payables. Ascend is offering point-of-sale financing to enable insurance brokers to break up those commercial payments into monthly installments. Ascend on Wednesday announced a $5.5 Ascend app.

At Qumra, we get excited about companies that disrupt traditional industries while doing good and improving quality of life. Our portfolio includes some great examples such as Fiverr that has disrupted the labor market by unlocking the global talent pool, or Talkspace, which is providing access to therapy to all. are at risk.

faster than those incumbents, and continue to expand it to more services in its home market, as well as take them abroad. The growth of e-commerce and other services on digital platforms has further spurred that trend. ClearBank describes itself as the first clearing bank to have launched in the U.K.

The company is not disclosing valuation but CEO Todd Clyde confirmed it was up compared to its previous financing. Some will still need financing and credit alternatives. I mentioned credit to Clyde: not every consumer wants to or can pay for goods in cash today, so why would they be able to do so in A2A?

Brazil’s banking system is a massive market, and one ill-served by incumbents. McCarthy, who spent significant time in Brazil growing up and is trilingual in English, Spanish and Portuguese, has been covering the LatAm and Miami ecosystems for TechCrunch with an eye to the disruption underway in these interconnected regions.

Monzo’s culture of customer obsession allowed it to use the crisis to thoughtfully build a beloved consumer and SMB product that has changed personal finance in the UK. 2 Incumbent banks miss the mark in two crucial areas: The banking experience has not evolved to match modern consumer expectations. This did not happen by magic.

has a legacy, centralized financial infrastructure that needs to be disrupted and re-imagined by fintechs with blockchain technology. ” Also in the report: “Exits have also stalled as IPO activity grinds to a halt, and analysts expect fintech startups will attract the attention of incumbents looking for M&A opportunities.”

This is a huge business, typified by incumbent behemoths like Lloyd’s of London, who in theory mitigate the risk insurance companies face when they get the formula wrong. “As a homeowner, if my home burns down I’ll get its value back. That can be a truly life changing thing.”

What kinds of moves are the incumbents making and how they change the market? How might a startup disrupt this market? Financing plan : What are the major buckets of expenditures? Market Size Validation : The first thing is to verify market size and whether it foots with the data the company presented.

This is particularly interesting because many of the existing corporate card players often point to Concur as an incumbent that they are trying to replace. FIS has launched Worldpay for Platforms, an embedded finance solution aimed at SMBs. These companies, of course, join a plethora of others in the U.S. See you next week!

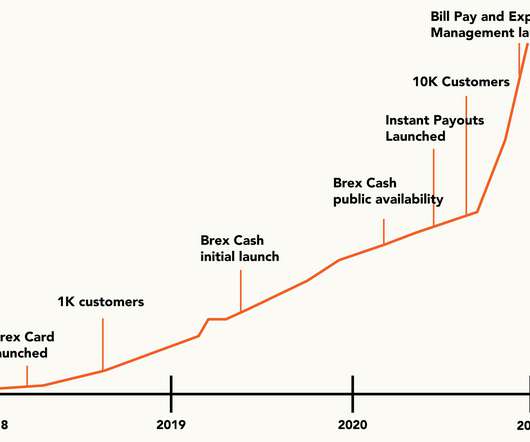

Even with $125K from YC and $1–2M in venture funding, a startup’s credit limit is still likely to tap out at $20K from an incumbent creditor—which is not nearly enough to cover software, marketing, and other expenses. incumbent offerings which only offered end-of-month reconciliation). As Brex has scaled, so have their customers.

Most immediately, Verdon says it allowed several million card holders to continue to operate their cards, “and customers could remain in business with minimal disruption” Railsbank is buying Wirecard Card Solutions, the UK arm of the disgraced fintech. and Europe and helps protect the reputation of the fintech industry.

It’s been on the lips of a growing number of investors on the hunt for disruptive opportunities blockchain-based technologies can offer. Blockchain is at its most powerfully disruptive when it supplies the missing link. can repair the attention-driven digital economy. What’s your web3 strategy?

The company is disrupting the mobile money industry dominated by banks and telcos with its app-based solution, cheaper fees and QR-based tech. And despite its continuous squabble with these incumbents due to eating into their market share, Wave claims to serve over 10 million users monthly across its operating markets.

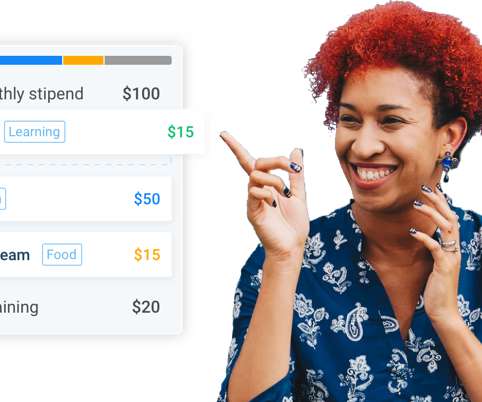

But Amy Spurling, the CEO of Compt, makes the case that incumbent solutions are overly reliant on vendor marketplaces or benefits cards, which limit the ways in which employees can use their perks. Spurling was previously the COO and CFO at Jana, a mobile advertising company, where she managed HR and finance teams.

Freemium businesses disruptincumbents by dramatically reducing the costs of customer acquisition. The paid product features satisfy the needs of accountants and company finance teams, not end users. Both of these challenges arise when the pricing model is applied to end users, instead of the right target, the manager.

Since the pandemic disrupted the social rhythms of work and school, many of us have compensated by changing our relationship to digital media. Rapid shifts in the way we buy goods and services disrupted old-school marketplaces like local newspapers and the Yellow Pages. End-to-end operators are the next generation of consumer business.

COVID-19 disrupted virtually every sector of the transportation industry. COVID-19 disrupted virtually every sector of the transportation industry. We’d love to see better debt financing for electric vehicle companies. If the debt markets line up to finance these at scale, it could be a nice win-win.

Experts say Africa is poised to be disrupted by web3 in a similar fashion that has seen Southeast Asia become one of the best markets for web3. Many web2 incumbents or even web3 are having a $100-200 user acquisition costs so we can lower that by order of magnitude by directly incentivizing the end-user.”. million in seed funding.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content