This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

2 Incumbent banks miss the mark in two crucial areas: The banking experience has not evolved to match modern consumer. Scaling a consumer-focused financial platform—that is also now the primary bank account for millions of UK consumers—in the midst of a once in a century pandemic is close to impossible. This did not happen by magic.

It was very fulfilling to see how digitalization has helped our rural bank partners to thrive during the pandemic recovery period and enabled our loyal users to access attractive deposit and loan products digitally. Bookmark ( 0 ) Please login to bookmark Username or Email Address Password Remember Me No account yet?

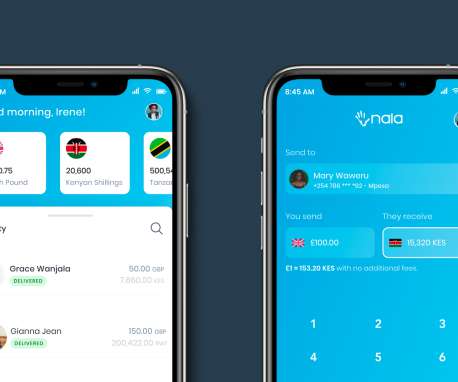

Their collective bet is that their market will grow over time and eat into traditional incumbents’ share. NALA , a Tanzanian cross-border payments company that recently pivoted from local to international money transfers, said Thursday it has raised $10 million in a new fundraising round. Whether that’ll happen remains to be seen.

We see an emphasis on young founders (“40 Under 40”), innovative ideas and disruptive challenges to legacy brands, incumbent companies and “old” ways of thinking. There is a massive opportunity to provide products and services that will make life better for today’s seniors and future generations of older adults to come.

High-growth early SaaS companies can achieve growth rates similar to those of their AI peers In the public markets, typically, the slower the growth of the company, the less they have been investing in AI. Forward ARR Multiple As of Type 25th 50th 75th percentile 2025-01-31 Software 3.1 2025-01-31 AI 8.3 There’s $1.5t of IT spend.

Internet usage continues to skyrocket, with 29.3 billion networked devices projected to be in use by 2023 and the growth rate currently at around 10%. This Series C is being led by D2 Investments, a new investment fund with LPs from the U.S. This Series C is being led by D2 Investments, a new investment fund with LPs from the U.S.

If you’ve ever taken out a mortgage, you know how painful and tedious the process can be. In an effort to make it simpler, faster and cheaper, a pair of former Blend employees have teamed up to build mortgage loan origination software that will connect banks, credit unions, mortgage bankers and brokers. trillion in loan originations in 2022.

In the long run, software platforms have the potential to be much larger than traditional incumbents. There are nearly six million small and medium businesses (SMBs) in the country, employing 43 million people. As a result, SMBs have been forced to cobble together off-the-shelf products, spreadsheets, and manual work to run their operations.

2 Incumbent banks miss the mark in two crucial areas: The banking experience has not evolved to match modern consumer expectations. Scaling a consumer-focused financial platform—that is also now the primary bank account for millions of UK consumers—in the midst of a once in a century pandemic is close to impossible.

Both approaches complement each other, especially for innovative tech companies which typically disrupt an existing market by undercutting the incumbents on the one hand ( and hence shrinking the market), while creating a new use case attracting a larger number of new users on the other hand. What’s yours? ”?—?below Four things: 1.

Displacement technologies compete with incumbents on the same buying parameters. SaaS products initially were viewed as a cheaper, often inferior product to their client/server peers. On the other hand, workflow applications enable workers to do work. Disruptive companies change the way a buyer thinks about solving their need.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content