This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I started in 2007 with a thesis that my primary investment decision would be about the team (70%) and only afterward about the market opportunity (30%). But they are also a tax on your time with portfolio companies, looking for new investments, running your shop and honestly they are a tax on your family life. Co-founder discontent.

That's basically what founders have to do when they fundraise, because you'll never be more successful with an investor who thought it was their brilliant idea to invest in your company, not yours. Who invests is also important--these are people who want to make money, but also be seen investing in the "hot" companies.

Sometime in the next few weeks, I’ll complete my next investment. Last August, I passed the point at which I had spent literally half my entire life working in this asset class, having started at the General Motors pension fund doing institutional investments in venture funds and late-stage directs back in February of 2001.

In this Dreamit Dose, associates Alana Hill and I, Elliot Levy , offer five things we wish founders knew after screening over 1,000 startups in the last year. Learn how to pass a VC associate screen in under 10 minutes! That’s something I didn’t realize when I was a founder sitting on the other side of the table.

This week I wrote about obsessive and competitive founders and how this forms the basis of what I look for when I invest. I had been thinking a lot about this recently because I’m often asked the question of “what I look for in an entrepreneur when I want to invest?” I had invested in myself for years.

Recently, Lightspeeds Mercedes Bent offered founders some reasons why a VC might ghost a founder. It was a perfectly reasonable explanation that basically boiled down to VCs are busy and theres no upside to hurting your feelings or getting into a debate. Never end a VC call without an immediate next step.

Berman comes from a real estate background, and he co-founded Camber Creek after realizing an opportunity to “create a double alpha situation,” both investing in high-growth startups and using those startups to improve the operations of his own real estate portfolio. Does the founder know how to sell into real estate?

founders, marketers, investors?—?and Trust, which today has announced a $9 million financing (Upfront is an investor), is a platform designed to help make the most of marketing investment by providing both analytics and a community of likeminded executives to share what’s working, and what’s not, across platforms.

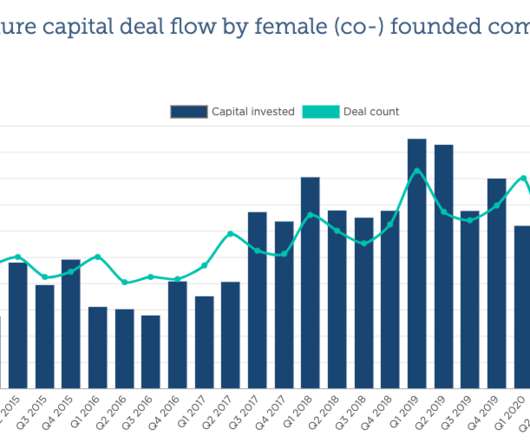

Last week, there was a Business Insider article measuring the percent of female founded companies that NYC seed funds invest in. That means you actually have a *better* shot, statistically, of getting VCinvestment at these firms, statistically, once you actually pitch. Lerer Ventures was second, with just under 20%.

During Q&A, both sides start engaging in a sort of conversational dance - with one side leading (VC/customer) and the other side following (founder). But often, we’ll hear founders misstep and repeat easy mistakes that throw off Q&A flow and cause startups to lose points. It’s similar with investors.

Even then private market investors can paper over valuation changes by investing at the same price but with more structure so it’s hard to understand the “headline valuation.” No blog post about how Tiger is crushing everybody because it’s deploying all its capital in 1-year while “suckers” are investing over 3-years can change this reality.

There''s been some writing about how VCs and founders interact with each other and it inspired me to take a step back and reflect on what my role is supposed to be with regards to the investments I make and the founders I deal with. Here''s what I came up with. I am not an expert. Venture Capital & Technology'

Time and time again i hear about founders that have bigger egos then anything else rejecting offers from top tier VC's (like YC ) and eventually leading thier companies to fail. If you do get and offer from top US VC's take them, dont be greedy and stay humble. Dont have a big ego.

When Revolution Growth first invested in Sweetgreen in 2013, the whisperings of food and wellness were present but sparse, and the bulk of lunchtime options focused more on convenience than ingredients. At the time, restaurants and food tech were on the margins of most investors’ minds and there was skepticism around VC-backed food concepts.

” Today I want to talk about how a VC thinks about equity pricing on your round and particularly if you’re coming off of a convertible note. Pre-money ($8m) + investment ($2m) = Post-money ($10m) and the investors now own 20% of your company $2m / $10m. So how DOES a VC think about financings at early stages?

Seed investments are down by any measure (funds, deals, dollars) over the past 3 years in deals < $1 million AND in deals between $1–5 million. Over the past month a colleague ( Chang Xu ) and I sifted through data on the venture capital industry (as we do every year) and made a bunch of calls to VCs and LPs to confirm our hypotheses.

Yesterday, I met with a founder with an interesting model who was raising $400k to bring the finishing touches to her product to make it customer-ready. In fact, the only founder I've ever seen completely run the table for a multi-million dollar seed round based off of a Powerpoint is Chantel Waterbury of chloe + isabel.

Founders seem to get that. Don’t get me wrong—I don’t mean trust in the sense that VCs think founders are just going to get a fake passport and move to Fiji, or that investors are secretly plotting to take over the company. VCs aren’t experts at every aspect of a startup at the same level across the board.

While most of the money that goes into VC funds comes from institutions that are highly experienced in the asset class, some family offices and high net worth individuals also invest in VC. They’re trying to get exposure and diversification at the same time, while potentially seeing co-investment deal flow.

How long does it take from first meeting a VC to getting cash in the bank? It''s also not the best way to create a helpful syndicate of investors that share the founder''s vision for the company. If all my deals came as intros from trusted connections that I know for years versus at founder pitch events that''s interesting data.

A recurring theme in a lot of my BSList posts is that, if an investor thinks they can make a boatload of money with you, they’ll go to all sorts of lengths to invest. That includes investing way earlier than they would normally, investing outside of scope, investing with their personal capital outside of the fund, etc.

This is what I know it feels like for a lot of founders and investors alikefloating in the rarified air of extremely successful people defined by their outcomes. I cant tell you how many times I got announced as a successful VC when I was introduced on a panel or sat across the room from a potential limited partner telling them I was.

VC firms see thousands of deals and have a refined sense of how the market is valuing deals because they get price signals across all of these deals. It’s not uncommon for a VC to ask you how much capital you’ve raised and what the post-money valuation was on your last round. So why does a VC ask you?

I realized a long time ago that the VC’s customer is the founder/CEO/portfolio company and that our investors (called LPs in VC speak) are our “shareholders” That was a very defining moment for me and has clarified what matters the most in a VC firm. That is very rare but has happened. That can work too.

The responses I got came at a time when I've been having a lot of conversations with female founders as well about their fundraising experiences. At this moment, I'm in the process of backing three companies that have at least one female founder and I just finished a round for a black female founder in December. Ducks head.]

Investing in founder-led businesses is comforting to me. Coinbase has reacted by making huge new bets on Coinbase Wallet and Coinbase NFT and is committed to winning in those markets like it did in the investment era of web3. Investing in founder-led businesses is comforting to me.

Firms like Baseline, Felicis, ff Ventures, Founder Collective, Freestyle, HomeBrew, IA Ventures, K9, Lowercase, NextView, Resolute, Rincon, Crosscut and the countless other great firms we all now know didn’t exist. Some quick highlights include: The Role of a Seed Stage VC. Each VC raises money – say $90 million.

But I have been in close contact with the NVCA, many of the major law firms and many of the major VC firms. Am I ineligible since I’m VC-backed? There is nothing in the rules that state that VC-backed businesses are ineligible. I am not claiming to be the world expert on this. shouldn’t I? The short answer is “no.”

The Dreamit team has said it before, raising money from a VC is a lot like sales. co-founder). If they hesitate, respond with, “Okay, can you tell me the 2 or 3 things you would need to see in order to invest?” It set you miles apart from other founders and quickly demonstrate your sales skills. It takes a lot of stamina.

The last thing you want as either a founder or even a VC is to have an investor get stuck with you when you're not on the same page about expectations. So here's all the reasons I told him he shouldn't be in: 1) Fund investing is boring. You trust me with your money and I get to do the fun part--working with founders.

If I was optimizing for cash, I would have been an investment banker a long time ago. Plus, when I look at my risks--is the risk that a legal term will shoot me in the foot or that these two founders and a prototype run this business into the ground. A fund that returns three dollars for every dollar of capital invested would be a $2.4

Alicia Castillo Holley is an active angel investor in Silicon Valley and the Founder and CEO of The Wealthing VC Club, a boutique investment group of accredited investors that fills rounds led by VCs. This profile is the eighth in a series of interviews highlighting the work of interesting female investors.

I’m over-paying for every check I write into the VC ecosystem and valuations are being pushed up to absurd levels and many of these valuations and companies won’t hold in the long term. However, to be a great VC you have to hold two conflicting ideas in your head at the same time. two founders in a garage?—?(HP

In 2017, we partnered with iconic leaders in American business to turn the thesis we developed on the road — that great companies can start and scale anywhere when given a chance — into an investment vehicle. In the last decade, we’ve socialized several Rise of the Rest-isms to describe investments that check those boxes.

Since the beginning of modern venture capital investing — a relatively nascent asset class — the industry has been biased toward funding what it knows best: founders with familiar demographics (white, male) in familiar geographies (Silicon Valley). One event held by a few investors focused on Black founders is clearly not enough.

Why do VC's get such a bad rap? That's literally your baby--and 98% of the time, a VC will tell you that your baby is ugly. We're "kingmakers" whose investment has the "Midas Touch." That's probably why the vast majority of applications for VC positions tend to be from males. So what gives? 3) Access to money.

When I look at all of the opportunities we are currently considering plus all of the investments we have made this year to date, what stands out most to me is the location of the founders and teams. And very little of it is in western Europe where most of our non-US investing has been for the last decade.

Fund investing, like adulting, is boring. That’s the first thing anyone trying to raise a fund needs to understand, as well as anyone thinking about investing in one. The partner at the fund, the VC, gets to do the fun part—the meeting with founders, vetting deals, negotiating, helping, etc. So what’s the point?

I wrote yesterday , about the quarterly numbers for VCinvesting activity: If this was a student coming home with a report card, it would be straight As. Firms invested a total of $434 million in Q3—the lowest figure since the second quarter of 2017, according to PitchBook data. It feels like positive change is happening.

This is part of a series of advice for founders who need to raise money from venture capitalists. Somehow many first-time founders equate “sales” with something that is beneath them. I always tell founders … “An investors job is to deploy capital and make a return. an investment in your company.

Supply chains have been disrupted, businesses have had to close or operate at limited capacity for months, and even founders have had to expand their fundraising timeframes as we saw in our 2020 Female Founders Data Report. As a VC firm, we’ve had to adapt many aspects of our business as well.

In order to understand how to “get to yes” with a VC you first need to understand how VC partnerships make decisions and then you can understand how to increase your odds of closing a deal. VC Partnerships Start by understanding how many partners are at the firm you are approaching. It’s super easy to suss all this out.

I woke up to a dream this morning where I was playing a game that was very similar to Turntable.fm , a failed effort to create a social music experience that had a moment back in 2011 and that I had invested in via USV. I met the founders and was happy for them. Investments that don’t work haunt me. Then I woke up.

So Why Did We Invest? As a VC (especially based in LA), I see hundreds of video apps. I first met the Ferris founders ( Paul Boukadakis & Chris Shaheen ) more than a year ago. The post Why We Invested in @FerrisApp – A New Kind of Video Sharing App appeared first on Bothsides of the Table. Building for Android.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content