This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Jeff Berman is General Partner at Camber Creek , one of the first venture funds dedicated to real estate technology and the built world. Key Questions To Answer When Pitching Real Estate Tech VCs Is there demand for the product? Founders speak to this network as part of the diligence process and get feedback.

The funny thing about stats is that you can basically come up with a stat to justify any argument or position--and the whole female founders in tech conversation has a ton of numbers that people put out there as various types of proof and justification, or blame. First time founder friendly. Venture Capital & Technology'

There''s been some writing about how VCs and founders interact with each other and it inspired me to take a step back and reflect on what my role is supposed to be with regards to the investments I make and the founders I deal with. Venture Capital & Technology' Here''s what I came up with.

Pitchbook estimates that there is about $290 billion of VC “overhang” (money waiting to be deployed into tech startups) in the US alone and that’s up more than 4x in just the past decade. But it will be patiently deployed, waiting for a cohort of founders who aren’t artificially clinging to 2021 valuation metrics. What is a VC To Do?

How long does it take from first meeting a VC to getting cash in the bank? It''s also not the best way to create a helpful syndicate of investors that share the founder''s vision for the company. If all my deals came as intros from trusted connections that I know for years versus at founder pitch events that''s interesting data.

There’s a quick litmus-test conversation any early-stage VC will have with the founder and it’s one that you should be as prepared for as your elevator pitch. It goes something like this … VC: “How much money are you raising?” Founder: “$8–10 million” VC: “What’s your current burn rate?” Founder: “$250k / month.”

I realized a long time ago that the VC’s customer is the founder/CEO/portfolio company and that our investors (called LPs in VC speak) are our “shareholders” That was a very defining moment for me and has clarified what matters the most in a VC firm. That can work too.

The world around us is being disrupted by the acceleration of technology into more industries and more consumer applications. Technology solutions are now used by authoritarians to monitor and control populations, to stymie an individual company’s economic prospects or to foment chaos through demagoguery. Are we in a bubble?”

One is “tentpole company,” or a category-defining startup that helps put their hometown on the map, both for investors and future generations of founders. Internally, we’ve begun using the term “founder-market-geography fit” to describe this idea. What is Founder-Market-Geography Fit? Let’s get into it.

Plus, when I look at my risks--is the risk that a legal term will shoot me in the foot or that these two founders and a prototype run this business into the ground. Venture Capital & Technology' When a bigger fund is in a round with me, they''re going to look at the legals, too--so I''m generally fine with whatever they go for.

I became a VC 12 years ago in 2007 when the pace of deals was much slower. As I was trying to figure out the role I wanted to play in the VC world I decided I wanted to focus on businesses that were building deeply technical products to solve problems for business users.

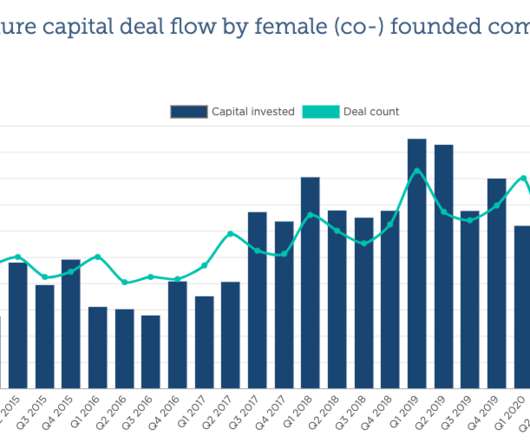

I wrote yesterday , about the quarterly numbers for VC investing activity: If this was a student coming home with a report card, it would be straight As. The third quarter total also amounts to a 48% drop in funding from Q2, when female founders received $841 million across 132 deals. It feels like positive change is happening.

In order to understand how to “get to yes” with a VC you first need to understand how VC partnerships make decisions and then you can understand how to increase your odds of closing a deal. VC Partnerships Start by understanding how many partners are at the firm you are approaching. Reciprocity is equally destructive.

Not every potentially good VC previously worked for Fred Wilson and Josh Kopelman. Not every VC used to get pitched by VC funds for a living and has seen hundreds and hundreds of VC pitch decks. So what about a Techstars-like program for new VCs? How can we leverage them to help create the next generation of VCs?

There are studies that suggest that there are lots of perfectly fantastic female owned business that are undercapitalized because the founders aren''t seeking it--perhaps they believe the system won''t support it, perhaps it relates to perceptions of risk. Venture Capital & Technology' It doesn''t prove squat.

Much has been written about when it is time to hire a “professional CEO” to run a startup company and of course that has long been a norm in Silicon Valley when founders find that their inexperience may be a limiting factor in company growth ( know as the Peter Principle ). I like technical founders so this wasn’t an issue.

Every time he opens his mouth about founder diversity, he seems completely out of his league to address the topic. The biggest question I think VC''s face right now is whether or not, in the future, the best founders will look and act like the best founders of the past. Venture Capital & Technology'

“Why do founders want to take the VCs’ money? ” This is a frequent theme of mine when asked to speak to audience about the VC industry. Founders will continue to take the “growth at all options” path that leads to privacy & trust creep at places like Quora. Growth, again. Grow or die.

The culture is driven by the 20-something irreverent founder with huge technical chops who in a “David vs. Goliath” mythology take on the titans of industry and wins. But markets have changed and I think investors, founders and experienced executives who want to join later-stage startups can all benefit from playing the long game.

Add on the fact that some people theorize that the need for venture capital dollars will peak, or potentially already has, and then decline because of the ever-decreasing cost of technology infrastructure as well as the increasing capability of AI to replace expensive humans. This is something I talk about a lot with my VC coaching clients.

I only say that because after years as a VC I can always tell when my peer group invested in something because “it seemed like it would make money” versus when they invested out of passion. On reflection of the role that I want to play as a VC it is clearly in the camp of passion. I’m a VC.

This is a theme I have come back to many times over the last decade but in the wake of all of the headlines about high profile founders, VCs, and companies leaving the bay area, I thought I would return to it. I am not saying that founders will stop traveling to raise money, although I think that may stick post-pandemic.

Besides, there were a limited number of places where I could do my job in venture capital anyway—and while I might be a go to for a pitch from super early stage pre-seed and seed founders looking for quick answers and decisive term sheets in New York City, the reality is that I would be pretty far down the list in the Valley. Plenty of bros.

Over the past month a colleague ( Chang Xu ) and I sifted through data on the venture capital industry (as we do every year) and made a bunch of calls to VCs and LPs to confirm our hypotheses. The reality is that as a result of two major trends the costs of starting a technology startup went down massively.

He talked about how for centuries education had “no technological core” (meaning it was bound by physical locations) and thus disruption was very difficult. Internationalization of Technology. We spoke about what succeeds early in technology market evolutions. If you have some time I highly recommend watching it.

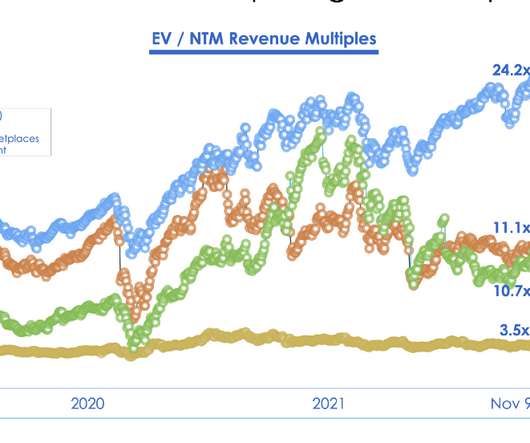

To shed additional light on this issue and its ultimate impact on startups, I partnered with the Center for Real Estate Technology & Innovation to ask proptech founders about their capital and strategic partners. VC firms are not blameless — over 1.8K VC investors wrote checks into proptech deals over the last five years.

Sesie Bonsi is the founder and CEO of Bleu , a financial technology platform focused on enabling touchless payment experiences. But most venture-backed startups are “still overwhelmingly white, male, Ivy-League-educated and based in Silicon Valley,” according to a study conducted by RateMyInvestor and Diversity VC. Sesie Bonsi.

Between 2006–2008 I sold both companies that I had started and became a VC. SEEING THINGS FROM THE VC SIDE OF THE TABLE While I was a VC in 2007 & 2008 those were dead years because the market again evaporated due the the Global Financial Crisis (GFC). THE VC VALUATION GOD Valuation obsession wasn’t restricted to startups.

The frantic pace of technology cycles, the amount of tech news, the blogs, the conferences, the demo days, the announcements, the fundings, the IPOs. It got me thinking about the advice that I often give to new VCs. But in today’s fast-paced world my observation is that as VCs we don’t control the ball as much as we should.

Creating awareness for your brand and products is one of the lifebloods of technology startups yet in a world where so many companies are being created it becomes difficult to rise above the noise. I am a VC. They are an investment bank that targets the technology & media sectors. I hand out money. Think about Luma Partners.

So today, I will write about 2020 in the context of tech/startups/VC/crypto. And technology based products and services are benefitting from these losses. 3/ Technology based commerce solutions gain when less people venture into stores to buy groceries, clothes, and other consumer products. And that is a good thing for society.

We particularly have developed many Fundraising hacks for VC and private equity funds , including our master databases of LPs interested in emerging VC managers. Investors are using some of the technology companies we have invested in and/or have assessed. Contact us if you have ideas on how we can work together.

Register The Philippine venture capital firm Kaya Founders has successfully raised $12 million in funding for two new funds. With this funding, Kaya Founders now manages a total committed capital of $16.5 With this funding, Kaya Founders now manages a total committed capital of $16.5

But VC is like congress. As you can see from the chart their data suggests there are about $25 billion of VC distributions per year in the US. According to FLAG Capital there are 100 active VCs (as defined by making at least $1 million in VC per quarter for 4 consecutive quarters). Their data looks at tech VCs.

For most of my career as a VC, the IPO has been the holy grail. I don’t take as much offense to this situation as others in the VC business have. I have viewed it as a mutually beneficial relationship between the top banks, VC firms, and the founders and CEOs who lead our portfolio companies. We will see.

I’m often asked about the differences between being at a VC and being an entrepreneur and whether I prefer one or the other. Funds like First Round Capital, True Ventures, Foundry Group, HomeBrew, USV and many others are still run by the founders and are still on the mission they started.

This goes for founders, employees and investors alike. That VC speaking on the panel, are the deals you know about really doing that well? There are a lot of founders with questionable records, too. Venture Capital & Technology' The NYC startup community maintains a positive, supportive atmosphere. How long ago?

Today I’m handing her the largest A-round check I’ve ever written as a VC as we lead her $10 million A-Round at uBeam. I said simply, “That’s the most ambitious project I’ve seen since I became a VC.” The practical uses for uBeam technology is limitless. That was three months ago this week.

I have one failed attempt at a startup under my belt as a founder and I don't have any particularly usable skills that anyone would pay for like selling, designing, building, etc. Try and figure out exactly what a startup had to show at the moment a VC chose to invest in them. Why should that stop me, though? So why bother showing up?

Of course Screendoor has an eye towards new VCs with identities, backgrounds and networks which are ADDITIVE to the venture ecosystem to better serve founders, so while the structure of the playbook is duplicative, the people running the playbook aren’t – and that’s the key.

With one company, a founder and his super inspirational, creative, and established buddy hatch a plan to build a very strong content brand that serves as a platform for a lot of diverse revenue streams--events, ecommerce, advertising. The second startup came to me from a founder of a company that I only found out later wasn''t fulltime.

Most founders barely have anything that looks like anything at this point, and most of them haven''t done this before. The founders I backed aren''t VCs (well, except Dave ) so I don''t know if that is such a great signal. The founders I backed aren''t VCs (well, except Dave ) so I don''t know if that is such a great signal.

Many questioned whether it could survive under the fail whale, inevitable competition from Facebook, founder fighting, fights with 3rd-party developers let alone become a revolutionary business that could make money. Apeel Technologies. Far from it. Lots of it.

Prorata rights are one of the most important rights of a private market technology investors and yet are seldom fully understood. These tensions seep out in some angels or seed funds publicly or semi-privately deriding later-stage VCs for their “bad” behavior. I believe I was one of the first to point this out publicly.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content