This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Sometime in the next few weeks, I’ll complete my next investment. Last August, I passed the point at which I had spent literally half my entire life working in this asset class, having started at the General Motors pension fund doing institutional investments in venture funds and late-stage directs back in February of 2001.

That's basically what founders have to do when they fundraise, because you'll never be more successful with an investor who thought it was their brilliant idea to invest in your company, not yours. Who invests is also important--these are people who want to make money, but also be seen investing in the "hot" companies.

When Revolution Growth first invested in Sweetgreen in 2013, the whisperings of food and wellness were present but sparse, and the bulk of lunchtime options focused more on convenience than ingredients. At the time, restaurants and food tech were on the margins of most investors’ minds and there was skepticism around VC-backed food concepts.

Seed investments are down by any measure (funds, deals, dollars) over the past 3 years in deals < $1 million AND in deals between $1–5 million. Over the past month a colleague ( Chang Xu ) and I sifted through data on the venture capital industry (as we do every year) and made a bunch of calls to VCs and LPs to confirm our hypotheses.

What Alan recognized was that most IRL forums and networking events are absolutely awful places to pitch and here’s why: 1) When a VC shows up in person, they’re looking to replicate the kind of top of the funnel they would get in an hour or two’s worth of e-mail, and that’s not going to happen if you corral them into a corner for 30 minutes.

This week I wrote about obsessive and competitive founders and how this forms the basis of what I look for when I invest. I had been thinking a lot about this recently because I’m often asked the question of “what I look for in an entrepreneur when I want to invest?” I had invested in myself for years.

A very common practice in the investment world is syndication. Syndication allows multiple investors -- whether they be individuals, angel groups, VC funds, etc. -- to join together and provide the funding resources needed by one company. Syndication has been a common practice amongst VC firms for decades.

The last thing you want as either a founder or even a VC is to have an investor get stuck with you when you're not on the same page about expectations. So here's all the reasons I told him he shouldn't be in: 1) Fund investing is boring. More updates, more casual events, more exposure to portfolio companies, co-investing, etc.,

This page shows the highlights of this sale, including a video, a link to the investment deck, and a link to the offering circular. I paid $330 for ten shares (out of a total of 1000 shares) implying a value of $33,000 for the five pairs, or roughly $6600 each.

When I look at all of the opportunities we are currently considering plus all of the investments we have made this year to date, what stands out most to me is the location of the founders and teams. And very little of it is in western Europe where most of our non-US investing has been for the last decade.

While most of the money that goes into VC funds comes from institutions that are highly experienced in the asset class, some family offices and high net worth individuals also invest in VC. They’re trying to get exposure and diversification at the same time, while potentially seeing co-investment deal flow.

Since the beginning of modern venture capital investing — a relatively nascent asset class — the industry has been biased toward funding what it knows best: founders with familiar demographics (white, male) in familiar geographies (Silicon Valley).

Berman comes from a real estate background, and he co-founded Camber Creek after realizing an opportunity to “create a double alpha situation,” both investing in high-growth startups and using those startups to improve the operations of his own real estate portfolio. Mitchell Schear was President of Vornado/Charles E.

When you get an investment from Brooklyn Bridge Ventures—you get me. My investment thesis is shaped by the sum of my personal experience and so are my values. My goal is to make Brooklyn Bridge Ventures the most accessible VC firm not just because I think it’s good business, but because I think it’s a based on good values.

Recently, Lightspeeds Mercedes Bent offered founders some reasons why a VC might ghost a founder. It was a perfectly reasonable explanation that basically boiled down to VCs are busy and theres no upside to hurting your feelings or getting into a debate. Never end a VC call without an immediate next step.

Even then private market investors can paper over valuation changes by investing at the same price but with more structure so it’s hard to understand the “headline valuation.” No blog post about how Tiger is crushing everybody because it’s deploying all its capital in 1-year while “suckers” are investing over 3-years can change this reality.

I woke up to a dream this morning where I was playing a game that was very similar to Turntable.fm , a failed effort to create a social music experience that had a moment back in 2011 and that I had invested in via USV. Investments that don’t work haunt me. It comes with the territory in VC. Then I woke up.

With our 2020 Robotics + AI sessions event on the horizon in early March, we’re diving back into the sector to learn about the attributes of construction attracting robotics VCs the most and which types of startups VCs are actually writing checks for in 2020. How much time are you spending on construction robotics right now?

During Q&A, both sides start engaging in a sort of conversational dance - with one side leading (VC/customer) and the other side following (founder). Most of that time goes to the meat of the conversion: the question-and-answer portion. It’s similar with investors.

Time and time again i hear about founders that have bigger egos then anything else rejecting offers from top tier VC's (like YC ) and eventually leading thier companies to fail. If you do get and offer from top US VC's take them, dont be greedy and stay humble. Dont have a big ego.

It may be silly and crazy, but it has also been a good investment for my friend and anyone who bought it in the early years. The combination of memes and investing is a powerful cocktail that I have been ignoring for a long time, probably incorrectly. It is easy to dismiss meme investing.

I realized a long time ago that the VC’s customer is the founder/CEO/portfolio company and that our investors (called LPs in VC speak) are our “shareholders” That was a very defining moment for me and has clarified what matters the most in a VC firm. That is very rare but has happened. That can work too.

VC firms see thousands of deals and have a refined sense of how the market is valuing deals because they get price signals across all of these deals. It’s not uncommon for a VC to ask you how much capital you’ve raised and what the post-money valuation was on your last round. So why does a VC ask you?

Staying on top of the early stage investing world requires a lot of reading. One of the biggest trends we witnessed over the past few years is the rapid pace of new early stage venture fund formation combined with significant growth in the amount of capital invested.

This will be the post where I dangerously attempt to walk the minefield of a white male VC opining on the topic. 4) The diverse background of the founder is not the main reason why most diverse founders get turned down for investment. That pitch has never excited any VC in the history of VC funding. Ducks head.]

I’m over-paying for every check I write into the VC ecosystem and valuations are being pushed up to absurd levels and many of these valuations and companies won’t hold in the long term. However, to be a great VC you have to hold two conflicting ideas in your head at the same time. That used to be called A-round investing.

Learn how to pass a VC associate screen in under 10 minutes! Alana suggests that before speaking to an associate, you gain a basic understanding of the fund’s focus and stages they invest in. These are easy tips if you know what to look out for. Do your research You should do your research before talking to an associate.

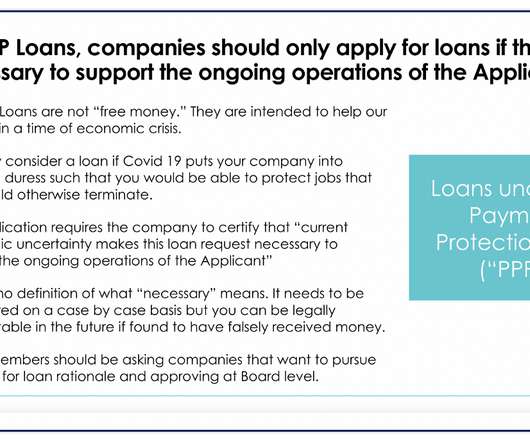

But I have been in close contact with the NVCA, many of the major law firms and many of the major VC firms. Am I ineligible since I’m VC-backed? There is nothing in the rules that state that VC-backed businesses are ineligible. I am not claiming to be the world expert on this. shouldn’t I? The short answer is “no.”

Why do VC's get such a bad rap? That's literally your baby--and 98% of the time, a VC will tell you that your baby is ugly. We're "kingmakers" whose investment has the "Midas Touch." That's probably why the vast majority of applications for VC positions tend to be from males. So what gives? 3) Access to money.

As a single GP (a firm with one investment decision making professional), I get asked a lot of questions about how I manage my time considering the number of investments I make. I think that's probably less than most early stage VCs take, but I think I've gotten pretty good at being decisive about what I'm *not* likely to invest in.

Fund investing, like adulting, is boring. That’s the first thing anyone trying to raise a fund needs to understand, as well as anyone thinking about investing in one. The partner at the fund, the VC, gets to do the fun part—the meeting with founders, vetting deals, negotiating, helping, etc. So what’s the point?

In order to understand how to “get to yes” with a VC you first need to understand how VC partnerships make decisions and then you can understand how to increase your odds of closing a deal. VC Partnerships Start by understanding how many partners are at the firm you are approaching. It’s super easy to suss all this out.

View this post on Instagram A post shared by Charlie O'Donnell - VC (@ceonyc) She’s the best. I’d like to invest in enterprise companies that make the experience of working better for all—from benefits and professional development to company culture. These are solutions I want to invest in. This is my daughter, Mirren.

If you truly believe that you, your company and your products are exceptional and your company will be valuable then you’re actually doing them a FAVOR by helping them invest in your startup. If you don’t believe in your bones that you’re amazing then it’s no wonder you don’t want to sell them on making the investment.” Same with VC.

Join Seraf for an engaging and informative webinar on VCinvesting in BRICS countries, with an emphasis on the exciting opportunities in Brazil. This event is tailored for venture capitalists, startup founders, and investors eager to delve into the high-growth potential within Brazil's dynamic market.

I wrote yesterday , about the quarterly numbers for VCinvesting activity: If this was a student coming home with a report card, it would be straight As. Firms invested a total of $434 million in Q3—the lowest figure since the second quarter of 2017, according to PitchBook data. It feels like positive change is happening.

might be, “finding great companies, investing in them and waiting for big financial returns.” Putting in place a well-thought-out investment strategy is a crucial component when building a high- performing portfolio of early stage companies, especially if that portfolio is going to generate acceptable returns.

In Part I of this article we discussed several key concepts of fund investment strategy and how funds are categorized, whether it be by industry, geography, stage, specialty (e.g. social impact, corporate, etc.) or some other criteria. Now let's take a closer look at capital allocation strategy and the life cycle of a venture fund.

. “ Different & Excellent ” equates to something that doesn’t exactly look like other VCs. Could be pinning their thesis on a category of technology or type of founder that isn’t yet understood by the investment community. I could even ask you directly which one of these you think you are and why.

To a VC, $50,000 a pre-sale isn’t really that much. VCs are less interested that you sold 10 customers, 20, or 100—they want to understand how many you’re selling per week and whether or not that kind of pace would be profitable for your sales & marketing efforts. That’s why we invest in a portfolio.

— @jasonlk How the Long Game Has Benefitted Upfront I was thinking about it this morning in particular and thinking about my own personal investment history. sold to Disney for $670 million and since our first investment was at < $10 million valuation we did quite well. Maker Studios?—?sold

In the most recent Pitchbook 2021 predictions , they project that Silicon Valley will make up less than 20% of all VC deals in 2021. In the first decade of USV, the 2000s, we mostly invested in NYC and Silicon Valley. In the second decade of USV, the 2010s, we invested throughout North America and Western Europe.

These investments have a high failure rate. In my experience, roughly half of seed stage investments fail completely, wiping out everyone’s investment, including the founding team’s. The exit values in VC have increased significantly over the last decade leading to escalating entry values. That makes sense.

Alicia Castillo Holley is an active angel investor in Silicon Valley and the Founder and CEO of The Wealthing VC Club, a boutique investment group of accredited investors that fills rounds led by VCs. This profile is the eighth in a series of interviews highlighting the work of interesting female investors.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content