This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Scott pointed to B-round SaaS valuations in excess of $100 million in $15m+ financing rounds with companies with very limited proof of customer traction or revenue. At some point the music will stop and we’ll find out which strategies were prudent. This can’t all be driven by increased company performance).

I asked some of the participating VCs, and they told me their attorneys had figured out a way to keep their stealth-mode companies stealthy.Yes, this strategy is not for every company. Often times when companies raise “bridge” financing (this is money from internal investors. Invidi is based in New York and founded in 2000.

I know that most people who are close to them tend to deny their existence, as we saw in the great housing bubble of 2002-2007 and the dot com bubble of 1997-2000. Or worse yet they may never get financed. Raise at “ the top end of normal &# but not so high that future financings in a corrected market become impossible.

One investor played chicken with me by threatening not to approve my next-round financing unless I gave him more equity. I remember this attitude really well from working in consulting where people took too much credit for “creating new strategies&# and deny any responsibilities for failed initiatives. So here’s the deal.

Just ask anybody who was trying to close funding the fateful week of September 11, 2001 or even March 2000. The best MBA class I took was an investment strategy class. When venture capitalists scale back investing activities it can be very swift and leave many companies that are in the process of fund raising hung out to dry.

The A round was done in February 2000 (end of the bull market) and my B round was done in April 2001 (bear market). Most importantly we talked about my good friends at Okta who were financed by Andreesen Horowitz. I explain in the video what happened in my first company (e.g. I eventually needed more money. Check ‘em out!

What would happen if companies offered flexibility to their employees, backed by data and scalable strategies? Sparked by a pair of scissors, some pantyhose and a party where founder, Sara Blakely , wanted to look her best, Spanx officially began production in 2000 and changed women’s fashion and fit forever. Sara Blakely / Spanx.

billion in an all-stock deal that was a reflection of its continued push into consumer finance. At the height of the dot.com boom in the first quarter of 2000, the bank had invested in a record 53 startups. In Q2 of 2000, that number dipped slightly to 46. We are trying to create a Strategic Finance category.

What can today’s founders learn from the 2000 dotcom bubble burst? By 2000, many of these high-fliers had left smoking craters behind. TechCrunch roundup: Dotcom crash history lessons, post-M&A strategies, climate tech heats up by Walter Thompson originally published on TechCrunch. “That person was me.”

2018 and 2019 exceeded the heady days of 2000 in terms of dollars deployed. Some firms run multiple strategies: different industries, geographies, and stages, akin to PE specialization and diversification. Also, more venture firms and startups are choosing debt as a non-dilutive financing alternative.

I have experienced two major financial disruptions in my career: the bubble burst in 2000 and the financial crisis of 2008. This ultimately leads to more frugal post-funding strategies. The comparable valuations from last year cannot be supported today, and expectations should be managed.

Existing backers Jungle Ventures and Xplorer Capital led the financing, which also included participation from JLL Spark, the strategic investment arm of commercial real estate brokerage JLL. . Its platform, the company says, houses all workplace data — including strategy, design, pricing and portfolio analytics — in one place.

THE ORIGIN I was the Founder & CEO of InboxDollars from 2000 to 2019. Ultimately, we chose not to pursue this model as part of our corporate strategy. About Daren Cotter : I founded InboxDollars from a dorm room (literally) as a college freshman in 2000. Side note: I rarely play the “What If?” A lot of new things.

2008 and 2000), not only have we seen outstanding companies being formed, we’ve also witnessed great venture firm performance during these windows,” he said. Private market valuations, at any point in time, are not only a reflection of a team’s hard work and progress, but are also impacted by the financing environment.

One investor played chicken with me by threatening not to approve my next-round financing unless I gave him more equity. I remember this attitude really well from working in consulting where people took too much credit for “creating new strategies&# and deny any responsibilities for failed initiatives. So here’s the deal.

The fresh capital will accelerate Tanaku’s mission to make home ownership accessible and radically transform the home buying experience, with the current focus on building the product, expanding the team, acquiring homes, and executing the go-to -market strategy. The problem stems from how the home needs to be purchased.

in Electrical Engineering from Stanford University in 2000 for her breakthrough work in circuit design automation. Prior to Prelude Ventures, Victoria worked on climate change strategy at BCG and started an agriculture supply chain company. Earlier, she led Finance at a major solar manufacturer. Mar received her Ph.D.

“Shopware, a company 100% bootstrapped prior to this investment, is ideally suited to CETP’s strategy of partnering with ambitious, founder-led technology companies. The money is notable not just for its nine-figure size, but also because of its context.

There are complex reasons for this, but at a high level, the success of nuclear power is much more about project management, financing, and policy than it is cutting-edge engineering or safety. Today, our nuclear fleet is among the oldest in the world, with an average reactor age of approximately 40 years.

Independent sponsors (groups seeking to acquire a company which do not have the equity financing needed in advance) earn nothing upfront, but earn 20% of the deals they facilitate. Similarly, certain Revenue-Based Finance investors (e.g., We are people-first, values-driven, multi-strategy, always-accessible. Blue Collective.

Alomar, who led startups through the dotcom bust of 2000 and the Great Recession of 2008, will talk about whether investors are still prioritizing growth over profits, and identify which proof points founding teams must define before their next raise. You can even break down that data more granularly by layering shopper data,” writes Price.

But there are also problems / risks: - the funding environment might change dramatically – there may never be a next round (see: March 2000, September 11, 2001 and September 2008). - I say define a strategy, test it up front and pivot if you’re not getting the traction you had expected. Who started this meme?

Instead, venture capital growth funds are financing these companies at these stages. Perhaps these investors are encouraging companies to continue to finance growth with negative profits, a trend that continues through the public offering but ultimately, isn’t the best decision for shareholders. Small IPOs. . Large IPOs. .

Founded by Russell Teubner in 2000, HostBridge Technology occupies a historic building along E. Teubner attributes the OCAST Technology Business Finance Program managed by Oklahoma Innovation Model partner i2E, Inc., There isn’t one. 7th Street, just off Main Street. I think the Oklahoma Innovation Model is both simple and brilliant.”.

The first is Momentum Investing , “a strategy to capitalize on the continuance of an existing market trend”, which usually meaning that the price has been rising in the recent past. In 2000, LPs invested $104b into 638 funds, but by 2003, LPs’ commitment rate had dropped to just $11b into 161 funds. Why, yes, they are.

I freely admit this (along with nearly everything between 1999-2000) was a mistake. You also understand that there are future financing rounds and in tough times this can change the value equation of stocks. I think either strategy is OK. But I thought I should do a quick post on the topic. I prefer not to.

I raised money as an entrepreneur, like you, in 1999, 2000, 2001, 2003 and 2005 for two different companies. These include building products, recruiting, managing your finances, marketing, selling, getting feedback from customers and … fund raising. Our 2000 fund is the single best fund of its vintage.

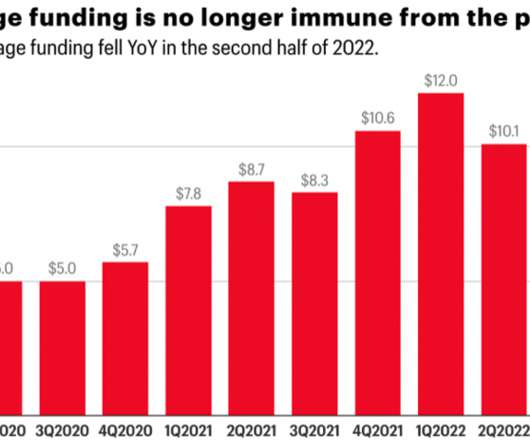

FIGURE 17: NUMBER OF COMPANIES ANNOUNCING NEW FINANCING ROUNDS Source: Crunchbase In 2022 the demand for capital outstripped the supply and this gap worsened as the year progressed. The recovery following the Internet bubble collapse of 2000 similarly took three years. By Q4, for every dollar of available capital there were 1.4x

Founded in 2000 by Vikas Jain, Rahul Sharma, Sumit Kumar Arora and Rajesh Agarwal, Micromax first started life as a small IT firm, making its first move into phones only in 2008. But the deal never closed reportedly due to disagreements between Micromax and Alibaba over future strategy for the business. billion from Alibaba.

I had previously raised VC in 1999, 2000, 2001 and 2005. They picked apart holes in our strategy and they were right. We will hopefully close on a $2-3 million financing round at some point in January and I can get back to the full time work of running my business. I look forward to the next phase of our business.

Terrorism at scale can only occur when these organizations can move money around to finance people who make bombs, buy guns, train recruits and so forth. Trust Between 1998–2000 the world became enamored with the “new economy” and Internet companies that were going public on NASDAQ in the United States. Regulation will come.

To the untrained eye, these zombies might have appeared to be alive and well– but they got deaded a long time ago by unsustainable business models and trading strategies. They procured additional financing at a 66% discount to their previous round … ouchie … but at least they did not have to halt withdrawals.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content