This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Lots of discussion these days about the changes in the VC industry. The VC industry grew dramatically as a result of the Internet bubble - Before the Internet bubble the people who invested in VC funds (called LPs or Limited Partners) put about $50 billion into the industry and by 2001 this had grown precipitously to around $250 billion.

I can’t help feel a bit of rear-view mirror analysis in all of “VC model is broken” bears in our industry. What the explosion in startups really means for our industry is a much bigger pipeline of potential deals if we VC’s can be patient. In 1998 there were around 850 VC funds and by 2000 there were 2,300.

You’re tied at the hip to your VC. Get to know VCs over a long period of time so that when you’re ready to get engaged you feel you know their character. How do you then reference check your VC to be sure that you’ve chosen a good firm and partner? Ask the CEO’s about the VC when the chips were down.

It’s always fun chatting with Jason because he’s knowledgeable about the market, quick on topics and pushes me to talk more about VC / entrepreneur issues. The following was available: “I kept hearing about startups that raised VC funding, but which hadn’t filed Form Ds (nor issued a press release). Short answer: no.

Spark Capital is relatively new to VC (founded in 2005) yet has become one of the hottest new VCs having invested in Twitter, Tumblr, AdMeld, Boxee, KickApps and many more companies. Topics we discussed in the first 45 minutes of the video include: What is VC like in NY? Our guest was Mo Koyfman of Spark Capital.

My partner Albert told me that when you factor in the financing costs of this swap, the average home in the Northeast United States could save $1000 to $2000 a year by doing this swap. It has gotten less expensive to do this swap out as solar and heat pump costs have come down.

Scott and I agree on nearly everything: The VC structure is changing and there appears to be a bifurcation into small & large VCs with an impact on “traditionally sized” VCs. The only point we didn’t seem totally aligned on was what we happening to the “middle of the VC market.”

Just ask anybody who was trying to close funding the fateful week of September 11, 2001 or even March 2000. I would argue that the shut-down of September 2009 was equally severe yet there are signs that this “VC Ice Age” has begun to thaw. Why did the VC markets freeze so quickly? Short answer – yes.

I’m enjoying being a VC. I thought I’d talk a bit about the differences I’ve experienced between being an entrepreneur & a VC – you know, from “both sides of the table.&#. VC meetings going well. 2 million in VC. And I had all the VCs play head games with me. I swore never to do that as a VC.

And so it happened that between 2000-2008 I was the biggest buzz kill at dinner parties. That would mean that the increased number of new business startups will lead to a “funding gap&# of deals that can’t get financed. Great businesses take 7-10 years to build. I avoided much of this. Why should you care?

I spoke about how Amazon Web Services deserves far more credit for the last 5 years of innovation than it gets credit for and how I believe they spawned the micro-VC category. I said that I felt that Micro-VCs were the most important change in our industry. It is great for entrepreneurs and great for VCs. I believe that.

The easiest way to work with and for VC funds is to become a part-time scout, getting paid for sourcing investments. How to find a job as a VC scout. VC recruiters list and compensation data. How to negotiate a partner role at a VC or private equity firm. Syllabus for how to launch, manage, and invest a VC fund.

In the technology world there are a few websites that most startups track to keep up with the latest financings, acquisitions, product announcements and gossip: BusinessInsider, TechCrunch, Mashable, GigaOm, etc. In the VC & Private Equity world there’s a small number, too, with one of the most respected being PEHub.

People assume that I’m biased because I’m a VC and think you should always get the highest valuation possible. The A round was done in February 2000 (end of the bull market) and my B round was done in April 2001 (bear market). But if you do this early (pre VC) then the price points are pretty low. This is wrong.

Andrew Chan is a senior associate at Builders VC , investing in early-stage companies that are transforming pen and paper industries. Gen Z VCs have raised funds, garnered social media followings and profited from the Gen Z mentality. Andrew Chan. Contributor. Share on Twitter. Objectively speaking, and much to my chagrin, I’m a Gen Z.

2018 and 2019 exceeded the heady days of 2000 in terms of dollars deployed. Second, as competition has intensified, VC funds have invested in platforms (we call it founder experience at Redpoint). Also, more venture firms and startups are choosing debt as a non-dilutive financing alternative.

I’d like to explain as best I can my opinion on what is going on because most of what I hear from entrepreneurs is not only wrong but is reminiscent of what I heard in 1997-2000. What is the True Sentiment of VCs? Brad was openly writing about this and it felt like he was giving the VC playbook away for free!

Within a year, by late 2000 / early 2001 consulting firms were firing people en masse. I was reminded of all this this when I read a blog post by one of my favorite thinkers on the VC market, Bryce Roberts, who talked about “ unfundable companies.&#. Most of the Internet startup consulting firms went bankrupt.

That’s the deal you get when you’re raising in a good market for startup financing. I’m a VC so I have an obvious bias. It was early 2000. I saw this kind of pricing when I first entered the VC market in 2007. That’s fine. But that’s not where this is coming from. That was market.

More financings occur outside San Francisco, but Bay Area companies now raise 2000 to 2500 rounds per year, up from 404. It’s not that VC dollars have left San Francisco to fuel other geographies. It’s not that VC dollars have left San Francisco to fuel other geographies. per year to $30b-$36b per year.

Founders who manage to raise more VC funds end up having a greater value stake in their company when the time comes to IPO, according to statistical research. The learning curve is steep; you’re not just studying VC as an industry, but the individual investors themselves. But the opposite is also true.

I’m enjoying being a VC. I thought I’d talk a bit about the differences I’ve experienced between being an entrepreneur & a VC – you know, from “both sides of the table.&#. VC meetings going well. 2 million in VC. And I had all the VCs play head games with me. I swore never to do that as a VC.

Lerner said this point in time feels like the period between March and December 2000, “when public technology stock prices dropped dramatically and there was little apparent impact on venture capital fundraising. The biggest VC firms are managing a lot more moolah than you thought. That’s new.”. India-based 100X.VC

However, it appears that even though VCs are proceeding more cautiously than before and taking their time with due diligence, they are still investing. CB Insights recently found that two of the largest global VC firms, Sequoia Capital and Andreessen Horowitz, actually backed more fintech companies in 2022 than any other category.

If it sounds odd that a Series B would be so much smaller than the Series A, that’s in part because that previous round was a mix of debt and equity: the company had raised very little since being founded in 2000 and was profitable. That is driving a market for more software automation, to take out some of the busy work.

The judges for this pitch-off will be Yoon Choi (Muirwoods Ventures), Mar Hershenson (Pear VC) and Gabriel Scheer (Elemental Excelerator) on day one; and Sven Strohband (Khosla Ventures), Victoria Beasley (Prelude Ventures) and John Du (GM Ventures) on day two. ” Mar Hershenson — Pear VC. Mar received her Ph.D.

Nicholas leverages his extensive experience in entrepreneurialism, traditional and decentralized finance, and early-growth startups to provide operational guidance, optimize developer velocity, and help new sales teams reach operational maturity — quickly. As Chief Technology Officer at Armor Scientific, he successfully raised $2.5

THE ORIGIN I was the Founder & CEO of InboxDollars from 2000 to 2019. Our Leadership Team started noticing something interesting around 2010: many of our customers were VC-backed startups. About Daren Cotter : I founded InboxDollars from a dorm room (literally) as a college freshman in 2000. A lot of new things.

A multibillion dollar acquisition , IPO projections and some good ol’ VC and billionaire drama? That conversation hasn’t disappeared, but it has certainly gotten quieter, with many investors now telling me that there’s a super surge of financing on the way. billion in financing for startups that use its own platform.

He pointed to data from Pitchbook showing an uptick in down rounds in Q3 this year, with almost 19% of all European VC funding now fitting this criteria. The alternative after 6 months could mean “a rescue financing littered with aggressive liquidation preferences and exit clauses. Don’t let that be you,” he said.

But my VC didn’t seem to be in such a rush. They say, “I haven’t been able to reach my client (the VC) yet.” I call the VC to discuss. I talk to the VC. My VC wasn’t that keen either. And it obviously doesn’t just apply to a VCfinancing. Nor did their lawyer.

This trend opposes the broader VC market’s investment patterns. Startups pursuing consumer finance have popped recently, not driven by Bitcoin, but by a wave of founders bringing more sophisticated financial tools to the masses. Financial management tools like expense management or receivables financing are growing steadily.

Startups and VC. million in a new financing round as it looks to expand to the U.S. Before Karl Alomar became managing partner of VC firm M13, he led one company through the dotcom bust of 2000 and helped another survive the Great Recession of 2008. And came to the same conclusion. sorrynotsorry.

As in other countries in “COVID 2020”, VC tended to focus on existing portfolio companies. Jerusalem’s economy and therefore startup scene suffered after the second Intifada (the Palestinian uprising that began in late September 2000 and ended around 2005). billion (£7 billion), came from Jerusalem.

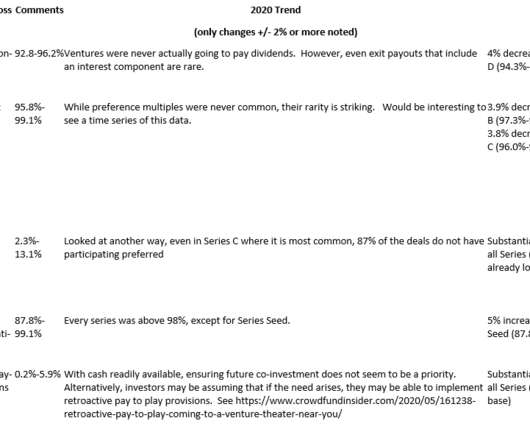

Roughly 40% of the data fields included in the Aumni survey relate to the frequency with which certain deal terms are found in financing transactions. Most deal terms are present in 80-90%+ of financings. Minimal Variation by Round – The lack of variability by financing round is striking. Covid, What Covid?

It also takes options off the table if you eventually find out that this isn’t a VC backable business. I’ve spoken about this in a post entitled, “ Do you even need VC ?&# Let’s assume that the $2 million buys 25% of your company, which is the norm in an equity financing. Should you take it?

Last, the capital to finance immense growth is readily available. 2014 will likely be the third largest year for VC fund raising since 2000, meaning investors have more capital to invest than in quite a while. More importantly, open source is a powerful distribution mechanism. The median IPO in the late 90s was about $25-30M.

2014 will be the third largest year in VC fundraising since 2000. The financing markets are a train and the IPO market and M&A markets are the locomotive, setting pricing multiples and valuations. VCs, flush with cash, are financing startups at the fastest pace in 14 years.

From an investor’s perspective, 2022 witnessed a sudden market reversal from an extreme equity seller’s market to an equity buyer’s market, causing dislocations throughout angel, VC, and startup ecosystems. It is unclear if VCs will agree to these terms, but LPs believe they now have more leverage. Smaller VC fundraises?

Private market rounds were 14x as common as IPOs in 2014, compared to the 2004-2007 era, when IPOs were about as equally common as large private financings. As Bill Gurley wrote, “These large, high-priced private financings are the defining characteristic of this particular technology cycle.”

In VC, this means you source companies by talking with other VCs and tracking the investment patterns and new Linkedin connections of other VCs. You could argue that when they were [raising] oversubscribed [VC rounds], Facebook, Google, Amazon, etc., But VC is historically and consistently cyclical.

I freely admit this (along with nearly everything between 1999-2000) was a mistake. I wouldn’t be a VC for very long if I did. You also understand that there are future financing rounds and in tough times this can change the value equation of stocks. But I thought I should do a quick post on the topic. I prefer not to.

Below is a marketing email sent around by one of the participating investment banks after the recent nCino IPO (which was underpriced in record-setting fashion, 195% first day “pop” – “the biggest first-day surge since the 2000 tech bubble”). You will see highlighted in red the two key objectives that guarantee underpricing.

She wants to figure out how to finance the billions of dollars in much-needed NYCHA repairs. But, fine, I’m sure he would have been an ok administrator—that is, until he brazenly flaunted the election finance laws through his father’s $1 million donation to his campaign. She wants to field complaints about flooded streets. Bike lanes.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content