This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

What Alan recognized was that most IRL forums and networking events are absolutely awful places to pitch and here’s why: 1) When a VC shows up in person, they’re looking to replicate the kind of top of the funnel they would get in an hour or two’s worth of e-mail, and that’s not going to happen if you corral them into a corner for 30 minutes.

Lots of discussion these days about the changes in the VC industry. The VC industry grew dramatically as a result of the Internet bubble - Before the Internet bubble the people who invested in VC funds (called LPs or Limited Partners) put about $50 billion into the industry and by 2001 this had grown precipitously to around $250 billion.

I’m writing this series because if you better understand how VC firms work you can better target which firms make sense for you to speak with. It in not uncommon to see a VC talk about “total assets under management&# as in “We have $1.5 What is a VC fund? VC’s don’t invest 100% of their own money.

I can’t help feel a bit of rear-view mirror analysis in all of “VC model is broken” bears in our industry. Looking ahead at the next decade I am excited by what I believe will be viewed as one of the best and most rational investment periods for venture capital due to seven discrete factors: 1. The Funding Problem. The Exit Problem.

You’re tied at the hip to your VC. Get to know VCs over a long period of time so that when you’re ready to get engaged you feel you know their character. How do you then reference check your VC to be sure that you’ve chosen a good firm and partner? Ask the CEO’s about the VC when the chips were down.

And so it happened that between 2000-2008 I was the biggest buzz kill at dinner parties. They have marked-up paper gains propped up by an over excited venture capital market that has validated their investments. Logic tells me the following: It is hard to make money angel investing. It was an investment management class.

To see the video of This Week in VC click on this link. We spent the first 45 minutes or so talking about industry trends (in this order): The history and background of True Ventures, one of my favorite early-stage VC’s (and the one with whom Om is a venture partner). DST invested $180mm last fall.

It’s always fun chatting with Jason because he’s knowledgeable about the market, quick on topics and pushes me to talk more about VC / entrepreneur issues. The following was available: “I kept hearing about startups that raised VC funding, but which hadn’t filed Form Ds (nor issued a press release). Short answer: no.

When venture capitalists scale back investing activities it can be very swift and leave many companies that are in the process of fund raising hung out to dry. Just ask anybody who was trying to close funding the fateful week of September 11, 2001 or even March 2000. Why did the VC markets freeze so quickly? Short answer – yes.

Spark Capital is relatively new to VC (founded in 2005) yet has become one of the hottest new VCs having invested in Twitter, Tumblr, AdMeld, Boxee, KickApps and many more companies. Topics we discussed in the first 45 minutes of the video include: What is VC like in NY? Our guest was Mo Koyfman of Spark Capital.

I will argue that LPs who invest in VC funds will also need to adjust a bit as well. These two trends had a major impact on the computing industry from 2000-2005 but the effects weren’t yet felt by the VC industry. I have called the creation of Micro VC as the most important change in our industry and I believe it.

Scott and I agree on nearly everything: The VC structure is changing and there appears to be a bifurcation into small & large VCs with an impact on “traditionally sized” VCs. The only point we didn’t seem totally aligned on was what we happening to the “middle of the VC market.”

My partner Albert told me that when you factor in the financing costs of this swap, the average home in the Northeast United States could save $1000 to $2000 a year by doing this swap. It has gotten less expensive to do this swap out as solar and heat pump costs have come down.

million which closed the first week of March 2000 – a week before the market crashed. 2 weeks later and we may never have raised any more VC. Quick aside: how can VC’s invest in online businesses, digital media, social networks or mobile applications if they don’t actually use the products actively themselves?

We have previously raised funds in 1996 ($200 million), 2000 ($400 million) and 2008/9 ($200 million). If you’ve been following the press about VC funds you’ll know this is no small feat. Like many modern VCs, we’re committed to investing in the community and in our portfolio companies.

This is part of my ongoing series “ Start Up Advice &# but I’d really like to call this post, “VC Advice.&#. We exchanged ideas when I was an entrepreneur along side him in NorCal in 05-07 and my point-of-view on founder / VC relationships hasn’t shifted even 1% since I went to the dark side.

He and I once took different sides of an debate about whether “VC signaling&# in early-stage deals is a serious problem or not. So it was fun to turn the cameras on him for 45 minutes for a special “NY edition of This Week in VC&# and hearing his views. I’ve also found him to not be dogmatic either.

But VC is like congress. As you can see from the chart their data suggests there are about $25 billion of VC distributions per year in the US. According to FLAG Capital there are 100 active VCs (as defined by making at least $1 million in VC per quarter for 4 consecutive quarters). Their data looks at tech VCs.

I don’t believe that search is the only answer in 2010 as it was in 2000. I won’t belabor this – I have an investment in this space ( ad.ly ) so I’m biased. I think this classifies as a “crack filler&# and I’m not sure I would have done the investment for that reason. Finally, I HATE the name.

I’m enjoying being a VC. I thought I’d talk a bit about the differences I’ve experienced between being an entrepreneur & a VC – you know, from “both sides of the table.&#. VC meetings going well. 2 million in VC. I swore never to do that as a VC. What do VC’s Experience?

In fact, thanks to increased scrutiny of investment funds in a post-Madoff world, this imbalance will probably get bigger and bigger. But crowdfunding investments in startups is the answer to all our worries in life, right? If venture funds could be supported by the local communities they invest in, you'd create a fantastic dynamic.

We moved into the legal process and final due diligence in January and February of 2000. Our final closure was the first week of March 2000. Many deals – VC or otherwise – didn’t close. VC, sales, biz dev, M&A or otherwise. Especially in VC. Let’s take the deal on the table and go build a huge business.”

Ask any VC how excited on a scale of one to ten they are about their latest deal, and they’ll tell you eleven out of ten. Veterans will probably be a little more cautious and tell you they’re at a ten out of ten—but despite knowing all the risks, a VC simply isn’t going to get over the line unless they’re pretty blown away by an idea.

They have totally changed the way you run a VC firm, investing heavily in systems & events for their founders that are pushing the boundaries of the way our industry works. It is clear that he is simply passionate about being a VC and participating in this industry. Investing Strategy. and Half.com.

As many of you know I run a weekly webcast called This Week in VC that’s getting between 25-35,000 weekly views across ThisWeekIn.com, YouTube & mostly iTunes. They never did any PR or marketing to get their videos to first get shown on the news during the 2000 election. Gregg is an ex Investment Banker and Wharton MBA.

The easiest way to work with and for VC funds is to become a part-time scout, getting paid for sourcing investments. How to win consulting, board, operating, and investment roles with private equity and venture capital funds (video). How to find a job as a VC scout. VC recruiters list and compensation data.

In the Correlation post, they define “hit rate” as: the percent of invested dollars generating a 10X or greater return. It could be the number of investments in your portfolio that return the fund. It could be the number of seed investments you make that turn into billion-dollar valued businesses.

I recently read a blog post by Beezer Clarkson, Managing Director of Sapphire Ventures about why entrepreneurs should care about from whom their VC funds raise their capital. There are a lot of things I think entrepreneurs should care about when raising from a VC: How big or small their fund is? I could go on for a long time.

I spoke about how Amazon Web Services deserves far more credit for the last 5 years of innovation than it gets credit for and how I believe they spawned the micro-VC category. I said that I felt that Micro-VCs were the most important change in our industry. It is great for entrepreneurs and great for VCs. I believe that.

@tevye2009 , Q: “can you briefly explain why it’s best to get a small valuation when getting investment.&# People assume that I’m biased because I’m a VC and think you should always get the highest valuation possible. But if you do this early (pre VC) then the price points are pretty low. This is wrong.

I’d like to explain as best I can my opinion on what is going on because most of what I hear from entrepreneurs is not only wrong but is reminiscent of what I heard in 1997-2000. What is the True Sentiment of VCs? Brad was openly writing about this and it felt like he was giving the VC playbook away for free!

Andrew Chan is a senior associate at Builders VC , investing in early-stage companies that are transforming pen and paper industries. In the last couple of years, a large group of “Gen Z VCs” have come to the forefront of what one might consider “hip” venture capital investing. Andrew Chan.

Not an investment philosophy “ I understand the sentiment of this post and it’s how I view AngelList (like email), but I feel like it loses a nuance about AngelList. Still, as a VC I value proprietary dealflow & long term relationships. That’s less interesting for me as a VC. I worry about that.&#.

Upfront VI is our latest core fund and is $400 million to invest in early stage entrepreneurs. link] There’s no doubt in my mind that “LA is having a moment” and both VCs and LPs realize it. 88% of the deals we do are Seed or A-Round investments and our median check size is $2.8 Boston, Finland and Paris).

Ad-buying opportunities within podcasts have historically been manual and limited, not unlike the process of purchasing web ads pre-2000. USV has been looking for an opportunity to invest in podcasting that fits with our thesis and we found it with Headgum and Gumball.

In the VC & Private Equity world there’s a small number, too, with one of the most respected being PEHub. I always wanted to have Dan on This Week in VC with Dan Primack ( to see video click link ) because he’s blunt, honest, opinionated and well informed. Question: Some people are saying traditional VC is dead.

In that post, I argued that the venture capital business could not sustain more than $20bn a year of new capital coming into it and continue to produce good returns to the investors in VC funds. Yes, it is true that some venture investments turn into businesses like Apple, Google, Microsoft that are worth $100bn and more.

Then these firms raised larger funds to invest in LBOs, but they diversified, too. In the 2000s, a wave of PE funds went public. The competitive dynamics in the market where access to invest is more valuable than capital. 2018 and 2019 exceeded the heady days of 2000 in terms of dollars deployed.

If you invested in the first angel round of a startup company it is usually very hard to sell your stock – usually for many years if ever at all. The earlier you invest the higher the chances the company won’t work out and thus you pay a lower price than later-stage investors. I’m a VC so I have an obvious bias.

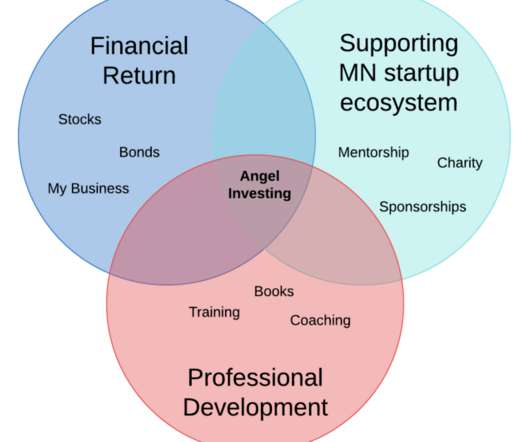

I began studying angel investing returns about 10 years ago as a result of a problem I couldn’t resolve: The investing world seemed certain that angel investors were rubes. Conventional wisdom dictated that they made reckless investments in very early-stage ventures mostly doomed to fail. Only they’re not.

Within a year, by late 2000 / early 2001 consulting firms were firing people en masse. Investment in training, adherence to process, global knowledge sharing systems, quality control / partner reviews and campus recruitment programs that attracted the right talent. Most of the Internet startup consulting firms went bankrupt.

I’m sharing my thought process because perhaps it will nudge some of you to angel invest too! I consider myself a furiously curious person, and angel investing is one of the most rewarding ways I’ve experienced to satisfy this curiosity. THE ORIGIN I was the Founder & CEO of InboxDollars from 2000 to 2019.

I was living in Europe in 2000 when the first WAP phones (Wireless Access Protocol) were introduced. I’m now a VC. I hope to soon announce an investment that relies on the mobile application infrastructure in the short-to-mid term. Absolute Power Corrupts, Absolutely. These phones were so over hyped.

million Series A round, passed the due diligence process, and the investment committee had approved the deal. In a Point Nine Capital survey, founders said that the two most stressful elements of raising venture capital are not knowing where in the fundraising process they are and not understanding why VCs have rejected their proposal.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content