This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Lots of discussion these days about the changes in the VC industry. The VC industry grew dramatically as a result of the Internet bubble - Before the Internet bubble the people who invested in VC funds (called LPs or Limited Partners) put about $50 billion into the industry and by 2001 this had grown precipitously to around $250 billion.

how on Earth could the venture capital market stand still? One of the most common questions I’m asked by people intrigued by but also scared by venture capital and technology markets is some variant of, “Aren’t technology markets way overvalued? With the enormous changes to our economies and financial markets?—?how Of course we can’t.

It will also be my last venture capital deal. Venture capital is a pretty opaque industry and if I can shed some light on what it’s like to do this, or to decide to stop doing it, I’m happy to help. I’ve decided that this is long enough for me—especially given the fact that when you’re in venture capital, you don’t just stop.

One of things I’ve loved the most about doing now 11 weeks of This Week in VC is a chance to have an hour-long recorded conversation with investors. And in my interviews with many VCs I feel that people can watch these and get to know the VC’s as human beings a bit better. So how did Mike get into VC?

One of the first things I did when I joined the venture asset class as a lowly institutional LP analyst in 2001 was to build the VC fund cashflow model. You incorporate expected company returns, mortality rates, and fee structures to try to predict how a venture capital fund works from a cash in, cash out, and NAV standpoint.

This is part of my ongoing series on Raising Venture Capital. Not so in venture capital. You’re tied at the hip to your VC. You’re tied at the hip to your VC. Get to know VCs over a long period of time so that when you’re ready to get engaged you feel you know their character.

When Chantel at chloe+isabel was getting offers from VCs, one of the things I said to her was to try and get as experienced a VC as possible--because she already had the younger product focused/community networked guy on her board. Of course, you don't always need that experience from a VC.

We received so much positive feedback from our This Week in Venture Capital show walking through valuation calculations & term sheets that we decided to do a Q&A show this week to address topics that entrepreneurs want to learn about. In fact, far better if you haven’t raised venture capital. A: It’s not best.

Back in 1999 when I first raised venture capital I had zero knowledge of what a fair term sheet looked like or how to value my company. Due to competitive markets we ended up with a pretty good term sheet until we needed to raise money in April 2001 and then we got completely screwed. The VC assumes you’ll have an option pool.

I spoke at Michael Kim’s excellent annual Cendana VC/LP conference today. One of the points I tried to make is that as venture capital investors as an industry we seem to have a healthy disdain for public market investors. What is your revenue growth rate and what does this imply about your number of months of capital remaining?

Just ask anybody who was trying to close funding the fateful week of September 11, 2001 or even March 2000. I would argue that the shut-down of September 2009 was equally severe yet there are signs that this “VC Ice Age” has begun to thaw. Why did the VC markets freeze so quickly? Short answer – yes.

This is part of my ongoing series “ Start Up Advice &# but I’d really like to call this post, “VC Advice.&#. We exchanged ideas when I was an entrepreneur along side him in NorCal in 05-07 and my point-of-view on founder / VC relationships hasn’t shifted even 1% since I went to the dark side. You lose the dream.

Something happened in the past 7 years in the startup and venture capital world that I hadn’t experienced since the late 90’s — we all began praying to the God of Valuation. How might our next phase of the journey seem brighter, even with more uncertain days for startups and capital markets? What happened? Until we weren’t.

And that was evident on today’s Angel vs. VC panel. There are real changes in the venture capital industry and it would have been fun to talk about them. The VC industry is segmenting – I have spoken about this many times before. So in the past we needed VC to really get a startup going. Answer: Not much.

It quickly became impossible to raise venture capital. I lived through this again September 2001. Many deals – VC or otherwise – didn’t close. It isn’t even a story about raising venture capital or M&A. VC, sales, biz dev, M&A or otherwise. Especially in VC. Anybody who didn’t close was dead.

Me: So, you raised venture capital? Me: Raising convertible notes as a seed round is one of the biggest disservices our industry has done to entrepreneurs since 2001-2003 when there were “full ratchets” and “multiple liquidation preferences” – the most hostile terms anybody found in term sheets 10 years ago. On the phone ….

Henry told me that I should start a fund--me, a 27 year old former VC analyst turned product manager with no MBA at a startup that wasn''t really headed in any particular direction. I got my first job in venture--at GM--in February 2001. Venture Capital & Technology' After my two year stint was up, I bought a domain name.

It is a little known part of my career, but for a brief period from 1997 to 2001, I was part of a small group of investors who helped to create a startup ecosystem in Latin America. In that Chase Capital Partners meeting was a woman named Susan Segal who ran Chase’s Latin American private equity investing.

When I first started in venture capital, back in 2001, I used to fund funds. I worked for an institutional investor that invested in both venture capital funds and later stage growth deals. My job was to figure out why certain firms were winning and why they might continue to win.

I spoke about how Amazon Web Services deserves far more credit for the last 5 years of innovation than it gets credit for and how I believe they spawned the micro-VC category. I said that I felt that Micro-VCs were the most important change in our industry. It is great for entrepreneurs and great for VCs. source: Capital IQ.

What happened in 2022 is the bottom fell out of the capital markets and the startup and tech sector more broadly. As the capital markets, including crypto/web3, came undone, companies reacted by adjusting their burn rates to reflect that the growth at any cost phase was over and it was time to get on a path to breakeven.

Within a year, by late 2000 / early 2001 consulting firms were firing people en masse. On July 27th, 2001 Accenture IPO’s and many of the partners grew fabulously wealthy. Andersen had lost its long-time CEO, George Shaheen, was hemorrhaging staff and wasn’t exactly known as being an Internet pioneer.

Paul Martino, General Partner at Bullpen Capital. During our recent Dreamit Kickoff week, Bullpen Capital Founder and General Partner Paul Martino ( @ahpah ) spoke with our Spring 2020 cohort about the state of the VC ecosystem in the current economic crisis. Will a financial crisis affect how venture funds deploy capital?

Our first big institutional round of VC was $16.5 We went “nuclear&# and slimmed down to 33 people (yes, I know, still large by today’s standards but this was 2001), raised $10 million and we built a real company. I learned everything I know about startups in these lean years: 2001-2004.

I’ve seen friends (and family members) lose much of their savings that way over the years because “Black Swans” happen and in 1987, 2001, 2003 & 2008 (just to name a few from my memory) huge market gyrations caused much financial distress to people seeking short-term gains. At least later stage investors.

You’ve got to be able to come out of unsuccessful VC meetings, pull your socks up, and go into the next pitch. As a VC if I can tell that you’ve survived tough times and you don’t appear beaten down that’s a huge plus. This was soon after the bursting of the dot com bubble – in early 2001.

We raised a seed round of capital in 1999 and our first venture capital round was the first week of March 2000 (e.g. We were now set to close at $46 million in new capital. We found a way to get a round of venture capital closed after all of this. We were based in London. It became a social activity.

For example, Leading Edge Capital closed on nearly $2 billion for its sixth fund, Base10 Partners brought in $460 million for its third fund, Founders Fund secured $5 billion for two funds, Freestyle raised $130 million for its sixth fund and the list goes on and on. That’s new.”. Image Credits: Overlooked Ventures.

Andre Maciel is the founder of Volpe Capital. Jennifer Queen is the founder of Pina , a PR firm focused on startups and venture capital firms. Latin American venture capital and growth investments through 2018 had averaged less than $2 billion per year. Image Credits: Volpe Capital. Share on Twitter. Jennifer Queen.

Individual accredited investors in typical angel deals put personal capital at risk for an equity share of growth-oriented, start-up companies. We also have data points for VC investments in seed/startup companies (but not necessarily pre-revenue companies). – Need venture capital. million to a high of $3.4

The judges for this pitch-off will be Yoon Choi (Muirwoods Ventures), Mar Hershenson (Pear VC) and Gabriel Scheer (Elemental Excelerator) on day one; and Sven Strohband (Khosla Ventures), Victoria Beasley (Prelude Ventures) and John Du (GM Ventures) on day two. ” Mar Hershenson — Pear VC. John received his Ph.D.

If this pace of fund raising continues, 2014 would mark the biggest year for VCs since 2001, when the industry raised about $38B. The second quarter of 2014 is the sixteenth largest by capital deployed sinced 1995, making it a top quartile quarter, but to break into the top five, that figure would need to triple.

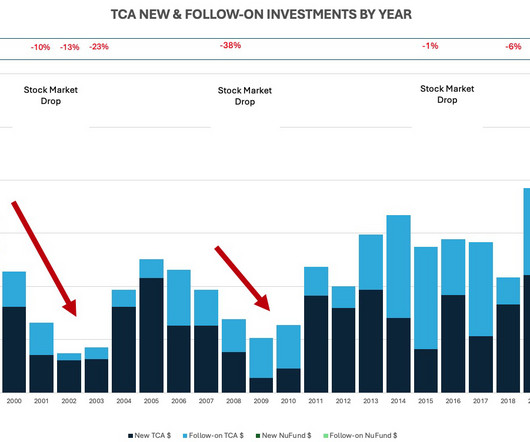

The recent data from ACA for all Angel Groups shows a similar recent pattern, with only 7% in the $1-3 million range and 12% in the 3-6 million range: Source: TCA Venture Group, Angel Capital Association Angel Funders Report There are of course higher valuations (as expected) in Series A compared to Seed/Pre-Seed, and dispersion in each stage.

As for the capital-raising event, I think it’s hard for the bankers to know where it will land with the broader market, so I’m not as negative as maybe some others. While several marketplace unicorns prepare IPOs, a VC digs into the data (EC). I do think this could be a $500 billion-plus company. There’s so much to be excited about.

This is part of my ongoing series on Raising Venture Capital. Recently I’ve been debating with a number of young startup companies that are raising money in the next few months, “what is the right about of capital to raise at a startup?&#. I’ve spoken about this in a post entitled, “ Do you even need VC ?&#

Most of what I learned about operating startups I learned from the really tough years at my first company from 2001-2003. My company had raised venture capital in April 2001 but we were told that there may never be any more coming. Hell – we fought against the VC’s together!

I’m not going to cover in this post the obvious post-show marketing tasks such as following up on all those business cards you grabbed, communicating with all those people who registered at your site and leveraging your new found fame to score venture capital. 2001-2004 were very humbling but we built a real company.

And as DeCambre points out, so far through 2014, the ten largest startup financings have yielded about twice as much capital as the ten largest IPOs. To paraphrase Mark’s question, can startups raise just as much capital in the private markets as in the public market, without the hassle of public market regulation?

For many businesses you should keep your costs low & your capital raises low until you discover whether you are really on to a big idea where there is market demand. When you see evidence that there is this so called “product / market fit&# then you may be ready for larger amounts of capital. How long is the window open?

I had previously raised VC in 1999, 2000, 2001 and 2005. In case VC’s haven’t figured this out yet, shit rolls downhill. My blog linked to Brad Feld’s blog because I was so grateful for his series on term sheets and he was one of the biggest reasons that as a VC I felt compelled to blog. Tempus Fugit.

There is all sorts of advice on the Internet about how to raise capital. I’ve raised money as a “hot company” and I’ve raised capital when no one would return my phone calls. I raised money as an entrepreneur, like you, in 1999, 2000, 2001, 2003 and 2005 for two different companies. Executive Summary.

With venture capital out of the equation, and only two business banks in his town, he couldn’t afford to lose one of them. “I A VC treating an entrepreneur that way today wouldn’t stay in business for long… 7. I recall one day, sitting in Wallace’s office. Both he and White were working me over pretty good.

John Danner , managing partner, Dunce Capital (an edtech and future of work fund with portfolio companies Lambda School and Outschool). Benoit Wirz , partner, Brighteye Ventures (an active edtech-focused venture capital fund in Europe that backs YouSchool, Lightneer and Aula). Full Extra Crunch articles are only available to members.

Bain Capital Ventures has named Christina Melas-Kyriazi, a former Affirm executive and angel investor, as its newest partner. Matt Harris, partner at Bain Capital Ventures, agrees. Since BCV’s first fund in 2001, the firm has invested over $4.5 The move to VC felt like a natural transition,” Melas-Kyriazi said.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content