This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Sometime in the next few weeks, I’ll complete my next investment. Last August, I passed the point at which I had spent literally half my entire life working in this asset class, having started at the General Motors pension fund doing institutional investments in venture funds and late-stage directs back in February of 2001.

I believe the rise in angel investing is here to stay and the professionalization of this class (aka “super angels&# or “micro VC&# ) is a good thing for the VC industry and for entrepreneurs. But I fear that for most angel investors who invest over the long haul angel investing will not be a profitable endeavor.

On the one hand, you’re over paying for every investment and valuations aren’t rational. In 2001 companies IPO’d very quickly if they were working, by 2011 IPOs had slowed down to the point that in 2013 Aileen Lee of Cowboy Ventures astutely called billion-dollar outcomes “unicorns.” That used to be called A-round investing.

a nonprofit dedicated to fostering the growth of startups and entrepreneurs in Oklahoma, is proud to announce surpassing the $100 million mark in total investments. These investments, collectively over $100 million, have provided vital early capital to help startups throughout the state to thrive. million in 2001. i2E, Inc.,

This lasted from about 2001-2004. Since then Mike his built his career by investing in early-stage companies (seed or series A), which is remarkable given that Polaris Ventures is a $1 billion fund. Simple: according to Mike Polaris has followed on nearly every seed investment that they’ve done. Total raised: $30mm.

Due to competitive markets we ended up with a pretty good term sheet until we needed to raise money in April 2001 and then we got completely screwed. In an early round of investment where there is not an extremely high price relative to normal valuations this is anything but benign. Those were the dog days of entrepreneurship.

At an accelerator … Me: Raising convertible notes as a seed round is one of the biggest disservices our industry has done to entrepreneurs since 2001-2003 when there were “full ratchets” and “multiple liquidation preferences” – the most hostile terms anybody found in term sheets 10 years ago. And so forth.

When I first started in venture capital, back in 2001, I used to fund funds. I worked for an institutional investor that invested in both venture capital funds and later stage growth deals. They raise larger and larger funds, for example, after building up a track record of successful angel investments.

My godfather got me IBM stock right after that, so that''s how I knew that a stock market and investing existed. I got my first job in venture--at GM--in February 2001. My dad brought home an IBM PS/2 in 1987. I got an internship on the buy side at the GM pension fund in high school--in 1997.

Like the downturns in 2008 and 2001, this has been a very trying time for entrepreneurs running startups. At the same time, many investors are being more cautious with making new investments, preferring to focus on their existing portfolio before investing in new companies. A startup is not a lone adventure.

Within a year, by late 2000 / early 2001 consulting firms were firing people en masse. On July 27th, 2001 Accenture IPO’s and many of the partners grew fabulously wealthy. Andersen had lost its long-time CEO, George Shaheen, was hemorrhaging staff and wasn’t exactly known as being an Internet pioneer.

I've been in venture capital (with the exception of a year in product management and two years as an entrepreneur) since 2001, when I started doing late stage venture and fund investing at a big financial institution.

It is a little known part of my career, but for a brief period from 1997 to 2001, I was part of a small group of investors who helped to create a startup ecosystem in Latin America. In that Chase Capital Partners meeting was a woman named Susan Segal who ran Chase’s Latin American private equity investing.

The VC industry grew dramatically as a result of the Internet bubble - Before the Internet bubble the people who invested in VC funds (called LPs or Limited Partners) put about $50 billion into the industry and by 2001 this had grown precipitously to around $250 billion. So the people who invest in VC funds have two problems.

The VC industry has different segments in it that have different fund sizes, different investment amounts and different risk / return expectations. If you’re an angel you invest your own money and you have nobody to answer to except your spouse. If you invest it in startups you’re a VC professional money manager.

million pre-money valuation is now raising $1 million at a $12 million valuation the next investor has nowhere to go but up (or sit out the investment). Just because the valuation in absolute terms isn’t a big difference does not mean that people aren’t paying higher than intrinsic value for these investments.

We went “nuclear&# and slimmed down to 33 people (yes, I know, still large by today’s standards but this was 2001), raised $10 million and we built a real company. I learned everything I know about startups in these lean years: 2001-2004.

For those of us who’ve invested in early stage companies, especially technology startups, we have confronted a universal problem. There are many ways to project the value of a company for purposes of pricing an investment, but all rely upon the revenue and profit projections of the entrepreneur as a starting point.

One of the first things I did when I joined the venture asset class as a lowly institutional LP analyst in 2001 was to build the VC fund cashflow model. Just about every analyst who looks at fund investing has built one. They're only investing in the ones that make it past seed, so isn't that a better bet? It's not perfect.

I’ve seen friends (and family members) lose much of their savings that way over the years because “Black Swans” happen and in 1987, 2001, 2003 & 2008 (just to name a few from my memory) huge market gyrations caused much financial distress to people seeking short-term gains. So, too, investments.

Martino founded Bullpen in 2010 with a focus on post-seed, pre-Series A startups, and he led the fund’s investments in companies like FanDuel, Namely, Ipsy, SpotHero, Classy, and Airmap. This geographic distinction is now less about actual geography and more about mentality and style of investing of these types of firms.

In fact, they will think better of you because you’re demonstrating that you’re the kind of thorough person that they wanted to invest money into in the first place. My chips were down in late 2000 / early 2001. Don’t be afraid to (politely and respectfully) ask for this. Don’t stop there. My story briefly.

I lived through this again September 2001. If it’s a biz deal you might care about IP protection, revenue share, investment commitments to joint marketing – whatever. I lived through this again September 2001. Many companies that were in the process of raising money did not. Anybody who didn’t close was dead.

We could do more in 2010 with more VC investment; the doubling assumes only ratable increase in marketing spend to achieve profitability. In my first company I had to raise money in April 2001 or die. The net effect for [my company] for example is we are now doing reasonably well. >50% of our revenue in now viral.

tevye2009 , Q: “can you briefly explain why it’s best to get a small valuation when getting investment.&# The A round was done in February 2000 (end of the bull market) and my B round was done in April 2001 (bear market). 6: @ marklanday Q: “Do you make personal angel investments and if so what are your criteria?&#

That next round of investment is proving difficult. This was soon after the bursting of the dot com bubble – in early 2001. I jumped on a plane and immediately flew to New York for just 1 day to meet with the Chief Investment Officer of ETF. It’s a gritty existence. Customers are harder to sign than you want.

When venture capitalists scale back investing activities it can be very swift and leave many companies that are in the process of fund raising hung out to dry. Just ask anybody who was trying to close funding the fateful week of September 11, 2001 or even March 2000. The best MBA class I took was an investment strategy class.

Please don’t also confuse this with whether a VC should invest in a CEO who’s done it before – that’s a given. This was a reasonable achievement when you consider that it was 2001-02, one of the worst years to be selling enterprise software and we were selling it SaaS style, which was still evangelical back then.

Founded by Tanya Van Court, who lost over $1 million in the 2001 bubble burst, the platform teaches financial literacy to children of all ages, helping them learn economic concepts, lingo and the principles of financial health. Brown, Ryan Bathe, CC Sabathia and Amber Sabathia. That teaches them how to spend money.

The additional days off translates into a roughly 80,000-Euros investment per year. The positive impact more than justifies the financial investment. After having worked in London, Frankfurt and San Francisco, he returned to Hamburg in 2001, where he lives with his wife and his seven-year-old twins. But it’s worth it.

Investing is similar. The below analysis outlines an approach to quantify the attractiveness of investing in commercial real estate at a given point. Such hard data can increase investment conviction when either is tempting. This is a positive signal for investing. The highest score ever was 97.6

Investing is similar. The below analysis outlines an approach to quantify the attractiveness of investing in commercial real estate at a given point. Such hard data can increase investment conviction when either is tempting. This is a positive signal for investing. The highest score ever was 97.6

Amy Cortese published “Venture Capital, Withering & Dying” in the New York Times on Oct 21, 2001. Most vulnerable are funds that were raised and invested at the height of the bubble, in 1999 and 2000, when 70 percent of all high-technology venture capital for the last two decades was invested.

Me: Raising convertible notes as a seed round is one of the biggest disservices our industry has done to entrepreneurs since 2001-2003 when there were “full ratchets” and “multiple liquidation preferences” – the most hostile terms anybody found in term sheets 10 years ago. Me: So, who was willing to invest in that? At an accelerator ….

OutSystems was founded in 2001, making it older than most companies that we cover on TechCrunch, and yet it remains privately held. TechCrunch had asked the company to break down its stated plan to invest its new capital in both go-to-market (GTM) capabilities and product (R&D) work. based software company has raised.

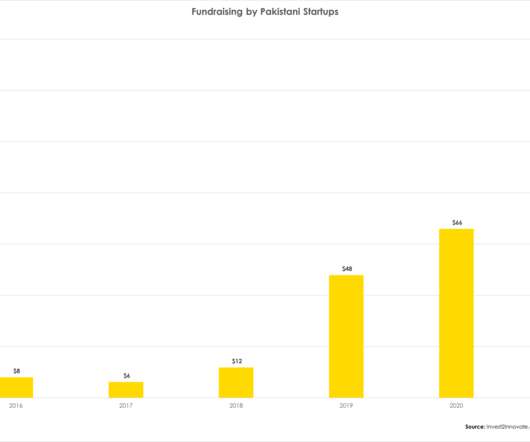

Mikal is an early-stage investor at Wavemaker Partners investing in startups across North America, MENA and Asia and author of the newsletter Emergent , analyzing one fast-growing startup in an emerging market every week. Mikal Khoso. Contributor. Share on Twitter. Unlocking Pakistan’s potential.

These angel investors generally invest $25,000 to $100,000 in a round totaling $250,000 to $1,000,000. For this round of investment, the angels collectively purchase 20-40% of the equity of the company and are seeking a return on investment of 20-30X in a period of five to eight years.

When we look at investing in companies we often look at their communities and the social engagement as an indicator of whether there is organic demand for the product (vs. companies that have to spend too heavily on customer acquisition).

The startup was founded by Tanya Van Court who had her own struggles with financial literacy after losing more than $1 million in stock during the bubble burst of 2001. The platform even recently introduced a feature called Goalsetter Invest, which allows users to buy and sell stocks. Goalsetter raises $3.9

“We’ve seen that all before … what’s new-ish (at least since 2001) is the massive overhang of growth investments that will take startups years to grow into,” he wrote. ” The ‘unicorn glut’ theory of startup misery. ” Armed with experience, insurtech MGAs are paving the way for insurtech 2.0.

As the entrepreneurs are hardly making any money to pay their personal bills, they devote a great deal of time and energy in making elaborate pitches for raising investment capital. Surging Growth: This period started in 2001. Some of the common mistakes made at this stage are –. Go On, Tell Us What You Think! Did we miss something?

Schiff Professor of Investment Banking at Harvard Business School, to weigh in on what we are seeing, and while they’re trying to make sense of things, too, they noted a couple of things that could impact the velocity of deal-making that we’ve been seeing. We asked Beezer Clarkson, partner at Sapphire Ventures, and Josh Lerner, the Jacob H.

There’s also been tremendous growth when it comes to dollars invested in female-founded companies. One 2018 study found that, during investment pitches, female entrepreneurs are more likely to be asked “prevention” questions, or those related to safety and potential risks and losses.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content