This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Many observers of the venture capital industry have questioned whether its best days are behind it. Looking ahead at the next decade I am excited by what I believe will be viewed as one of the best and most rational investment periods for venture capital due to seven discrete factors: 1. This article originally ran on PEHub.

I’d rather be Roger Ehrenberg with a thesis around data-centric companies and base my investment decisions on the skills I’ve developed in my career. To some extent Keith Rabois agreed with me about domain knowledge and argued that most of his investments are in the consumer Internet space as a result. Always have been.

And so it happened that between 2000-2008 I was the biggest buzz kill at dinner parties. They have marked-up paper gains propped up by an over excited venture capital market that has validated their investments. Logic tells me the following: It is hard to make money angel investing. It was an investment management class.

If you read this blog often you'll know that I'm a huge fan of First Round Capital. They have totally changed the way you run a VC firm, investing heavily in systems & events for their founders that are pushing the boundaries of the way our industry works. In 2008 they raised a much larger fund $132.5 Investing Strategy.

Rustic Canyon is an LA-based, but geography-agnostic VC that is currently investing from a $200 million fund. They were originally founded inside of Times Mirror and had a huge string of major investment success before spinning out as a fully independent fund. The investment will be used for product development initiatives.

I am excited to share the news of First Round Capital 's recent investment in cloud-to-cloud backup service Backupify. Josh Kopelman will be working closely on this investment as well. Joining our investment in the $900k round were General Catalyst, Betaworks, Jason Calacanis, and Chris Sacca. I freaked out.

But as sweet as that success has been (we invested pre-revenue in a small team) today my even more important news was the further expansion of our partner ranks. He first came to see me in 2008 when we was raising money for his 1st startup – NextMedium. I’ve known Hamet for 5 years. The idea immediately resonated.

Sam Altman of YC recently pointed out that pulling back during the downturn in 2008 would result in several big misses: In October of 2008, Sequoia Capital—arguably the best-ever in the business—gave the famous “RIP Good Times” presentation (I was there). A few months later, we funded Airbnb.

We had a special edition of This Week in Venture Capital this week shooting out of the Next New Networks offices in New York. Our guest was Mo Koyfman of Spark Capital. The Spark Capital website (it’s one of my favorites). Founded in 2008 by Mehdi Maghsoodnia. Content, of course, is the same!]. Total raised: $16.0mm.

If you want to raise venture capital more easily the advice could be quite practical and counter-intuitive. Many companies that are raising B or C venture capital rounds right now raised their initial money in 2005-2008. They often have “dead&# or “tired&# investors who have stranded capital. It is 2010.

I guess that makes USV, Spark Capital, Foundry Group, Accel, Benchmark, Revolution (along with several others) pretty happy right now. million pre-money valuation is now raising $1 million at a $12 million valuation the next investor has nowhere to go but up (or sit out the investment). source: Capital IQ. source: Capital IQ.

The VC industry grew dramatically as a result of the Internet bubble - Before the Internet bubble the people who invested in VC funds (called LPs or Limited Partners) put about $50 billion into the industry and by 2001 this had grown precipitously to around $250 billion. So as of 2008 total LP commitments were still at nearly $250 billion.

Well, they did ask David Chao of Doll Capital, who said that the " frothy bubble is over ". The last closed market we had was from about September 2008 until June 2009--10 months. We're seeing, for the first time, investment and some disruption in huge areas like education, food, healthcare, government and even hardware based startups.

Via TechCrunch by Arman Tabatabai: Venture capital has been flooding the various subverticals under the robotics umbrella in recent years, and the construction space is one of the largest beneficiaries. Matt Murphy and Grace Ge, Menlo Ventures Which trends are you most excited about in construction robotics from an investing perspective?

We have previously raised funds in 1996 ($200 million), 2000 ($400 million) and 2008/9 ($200 million). Well, the venture capital industry has changed a lot in the past 20 years … and we have too. Like many modern VCs, we’re committed to investing in the community and in our portfolio companies. What’s up with that?

But I am also someone who is very colored by my past experience of seeing the venture implosion after the first bubble and walking through the fundraising tumbleweed of late 2008. I'm all for people putting $25k to work to try something out--and if it works, having the momentum to raise more capital. Angels: Focus and pace.

Investments in innovation can often have unforeseen positive ripple effects. Back at the end of 2008, when the economy was in the tank, and funding was tough to come by, NYC Seed, a small local fund with some government and local academic backing supported my startup, Path 101.

There has been much discussion in the past few years of the changing structure of the venture capital industry. The rise of alternative sources of capital (crowd funding and the like). 15 years ago we were at the peak of Internet hype with the launch of many over-capitalized businesses with a market size & opportunity was limited.

In fact, much of the groundwork of the NYC tech community''s growth came before the late 2008 economic crash--when the city started paying attention to the tech community as the economic savior poster child. City money didn''t spur on the massive venture capitalinvestments that have been made by the private sector.

Paul Martino, General Partner at Bullpen Capital. During our recent Dreamit Kickoff week, Bullpen Capital Founder and General Partner Paul Martino ( @ahpah ) spoke with our Spring 2020 cohort about the state of the VC ecosystem in the current economic crisis. Will a financial crisis affect how venture funds deploy capital?

Our 2008 vintage early-stage fund has generated about 5x cash on cash but only generated a 22.5% Our Opportunity Funds invest in the later stage rounds of our top-performing portfolio companies plus a few later-stage investments in companies that are new to USV. cash on cash but generated a 58.6% cash on cash but only 46.7%

I’d rather be Roger Ehrenberg with a thesis around data-centric companies and base my investment decisions on my background. I should say that I agree that naive optimism in entrepreneurs can produce higher beta (upside or flops) and that’s good from an investment standpoint if you’re looking for big returns.

I''m super proud of Rob, Ben and the whole Backupify team--and this is particularly special for me because Backupify was the first investment I ever made as a VC, and the first board I ever sat on. Rob messed around with some local video thing in 2008, which everyone but Rob thought was a pretty terrible idea.

We’ve been dying to tell you all for a while that we had raised a new venture capital fund and of course given SEC filing requirements the story was somewhat already scooped by the always-in-the-know Dan Primack a few weeks ago. Our last fund we raised was in 2012 and we began investing it in April of 2012.

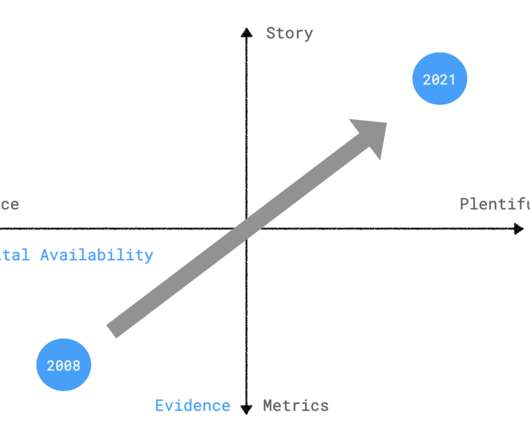

When I asked him what he meant, he replied because capital was so plentiful and accessible today, he hired more expensive people, spent more time developing a product, and invested with a longer time horizon before demonstrating evidence of success. Capital availability on the x-axis and evidence on the y-axis to illustrate his point.

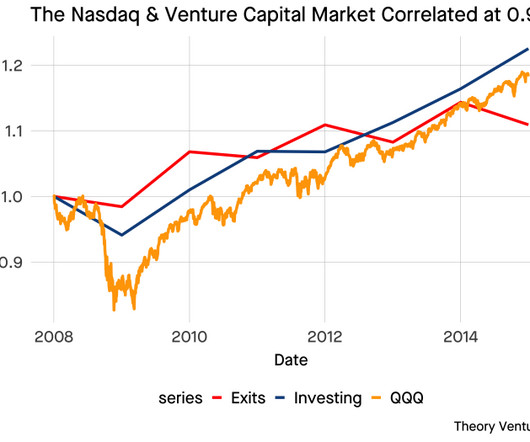

What will a venture capital turnaround feel like? In 2008, I had just become a venture capitalist. With 15 years’ perspective, I plotted the QQQ (Nasdaq) value against venture Investing activity & venture Exits activity (all log normalized). for QQQ/Investing & 0.93 Will it be gradual or sudden?

I spent my first year developing proprietary deal flow and learning the business and then the Sept 2008 / Lehman Bros collapse / financial meltdown happened. As a result I didn’t write my first venture capital check until March 2009 – exactly 5 years ago. I have done 6 VC investments – all within the past 20 months.

Company plans to use the capital to build out sales and marketing and r&d. -a led by Altos Ventures and Maverick Capital, with Larry Braitman. Founded in 2008 in Santa Monica by Ron Goldman (former CRO of shopping.com) and Rahul Sonnad. Incubated by Clearstone Ventures in 2008. a fbFund winner. Current round: $4.

At the Upfront Summit in early February, we had a chance to have many off-the-record conversations with Limited Partners (LPs) who fund Venture Capital (VC) funds about their views of the market. However, they have been sending VCs far more investment checks in the last ten years than they’ve gotten back as distributions.

In my previous post, The VC Ice Age is Thawing (for now) I wrote about the reasons why the VC market came to a screeching halt in September 2008 and remained largely shut until at least April 2009. But there are many zombie VC’s with no more investments left in their portfolios so it’s hard to know which trend has more impact.

I can't take credit for this meme, even though I've already invested in it.twice. The seminal application of the collaborative web--Github--was launched in April 2008. Once with Docracy, once with a super cool company launching in the first quarter of 2013.). It's a web where 1+1 really does equal more than 2.

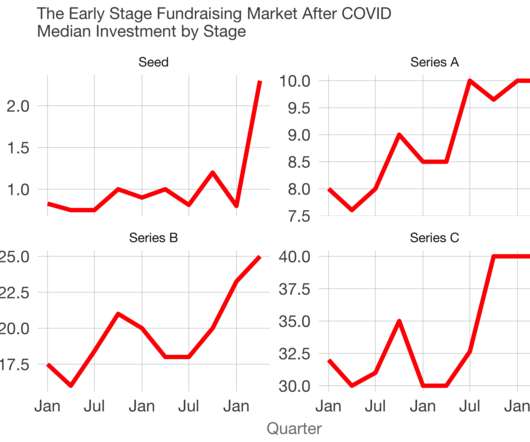

We reviewed the data in May and compared it to the effects of the financial crisis in 2008 on startup fundraising. As a reminder, 2008 saw a 40% reduction in venture dollars invested in startups. These corrections match 2008. The amount of available dollars to invest is high. The fundraising market is contracting.

I’ve seen friends (and family members) lose much of their savings that way over the years because “Black Swans” happen and in 1987, 2001, 2003 & 2008 (just to name a few from my memory) huge market gyrations caused much financial distress to people seeking short-term gains. So, too, investments.

In the first post in this three part series I described why I believe the VC market froze between September 2008 – April 2009. This has a tangible impact on the valuation of start-ups and the pace of investment. If Stanford has to cut back on VC investing, you can imagine how bad it is getting.

As we enter 2024, the capital markets have found their footing and are moving higher. That is good news for the innovation economy because healthy capital markets are a necessary support system. However, optimistic capital markets are necessary but not sufficient for a healthy innovation economy. But it eventually gets it.

This was really a fun week at TWiVC because we decided to have an entrepreneur come and talk about raising capital rather than having a VC come on. Raised angel money from Rob Lord, Reid Hoffman, Benchmark Capital and others. And the broader question of whether VC’s will continue to invest in the Twitter ecosystem.

There are real changes in the venture capital industry and it would have been fun to talk about them. The VC industry has different segments in it that have different fund sizes, different investment amounts and different risk / return expectations. If you invest it in startups you’re a VC professional money manager.

When venture capitalists scale back investing activities it can be very swift and leave many companies that are in the process of fund raising hung out to dry. But any entrepreneurs raising capital should keep in mind that this opening of the markets could possibly be temporary. Why did the VC markets freeze so quickly?

Here are the trends in venture capital financings from 2006 through 2010 – the number of seed stage deals funded and total investment by region in millions of dollars. . VCs in NYC invested, on average, only $2.4 US Angel Investment – All Regions. Investment. All Seed-VC. Silicon Valley. New England.

Our guest this week on #TWiVC was Dana Settle , partner at Greycroft Partners , a venture capital firm with offices in New York and Los Angeles. Founded in August 2008 in Palo Alto, CA, by Sam Christiansen and Keith Lee. Jelli - I went on record saying that I wanted to invest and that I think this company will create a big success.

Finch Capital , the early-stage fintech VC with a presence in London and Amsterdam, is acquiring Wirecard Turkey, a subsidiary of Wirecard, the disgraced fintech out of Germany. Finch’s managing partner Radboud Vlaar tells me Noma Pay’s larger plan is to invest in payments infrastructure in Turkey and the Middle East region.

Since then Mike his built his career by investing in early-stage companies (seed or series A), which is remarkable given that Polaris Ventures is a $1 billion fund. Simple: according to Mike Polaris has followed on nearly every seed investment that they’ve done. Spun off from Freewebs in 2008, based in Palo Alto.

Clearstone currently invests out of a $200 million fund based in LA with offices in Menlo Park and in India. Segment One: Jim’s background and Clearstone’s investment strategy. We also talked about Elevation Partners who invested in Palm and how this deal really salvaged their investment, which was a VERY big bet on Palm.

What a pleasure that I got to spend an hour talking with both Om Malik (whom I’ve always respected his views) and Paul Jozefak , a venture capital partner at Neuhaus Partners in Germany (and formerly the head of Europe for SAP Ventures). DST invested $180mm last fall. To see the video of This Week in VC click on this link.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content