This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In the first post in this three part series I described why I believe the VC market froze between September 2008 – April 2009. I obviously don’t have a crystal ball so the economy could fare better than my gut, but here’s why I’m cautious for some time in 2010 or early 2011: Why is the future still so unpredictable?

There has been much discussion in the past few years of the changing structure of the venture capital industry. The rise of “micro VCs” or seed-stage funds. The rise of alternative sources of capital (crowd funding and the like). On the surface the narratives have been. Where are we today? 50x more Internet users (2.4

Many observers of the venture capital industry have questioned whether its best days are behind it. I can’t help feel a bit of rear-view mirror analysis in all of “VC model is broken” bears in our industry. The most successful of these businesses will still need venture capital to scale their businesses. The Funding Problem.

We had a special edition of This Week in Venture Capital this week shooting out of the Next New Networks offices in New York. Our guest was Mo Koyfman of Spark Capital. Topics we discussed in the first 45 minutes of the video include: What is VC like in NY? The Spark Capital website (it’s one of my favorites).

Our guest this week on #TWiVC was Dana Settle , partner at Greycroft Partners , a venture capital firm with offices in New York and Los Angeles. Greycroft is an early-stage VC. Closing a VC fund in 2009/10 is a major achievement in and of itself. When the show has been processed it will be available here (estimated 8pm PDT).

How long does it take from first meeting a VC to getting cash in the bank? I went back across the 21 investments I''ve made both at First Round and at Brooklyn Bridge Ventures --a period that dates back to January 28, 2010, when I closed on Backupify. Venture Capital & Technology' That''s an interesting question.

I was on This Week in Venture Capital (TWiVC) again this week with Jason Calacanis. I don’t believe that search is the only answer in 2010 as it was in 2000. mm in Series A; IdealLab ( Bill Gross ), Index Ventures ( Danny Rimer ), Revolution LLC ( Steve Case ), First Round Capital , BetaWorks , Jason Calcanis.

This was the first episode where Jason wasn’t on the show, which gave me the chance to have another VC on the show to discuss deals. Rustic Canyon is an LA-based, but geography-agnostic VC that is currently investing from a $200 million fund. VC Financings: 1. I keep meaning to get him drunk to spill the stories.

It will also be my last venture capital deal. Venture capital is a pretty opaque industry and if I can shed some light on what it’s like to do this, or to decide to stop doing it, I’m happy to help. I’ve decided that this is long enough for me—especially given the fact that when you’re in venture capital, you don’t just stop.

At the time almost nobody had heard of the following funds: FirstRound Capital, TrueVentures, Floodgate and SoftTech. But back in 2005 there were a few people who spotted the trend before others and one of the true pioneers was (and continues to be) Jeff Clavier who founded SoftTech VC. Each VC raises money – say $90 million.

This is part of my series on Understanding Venture Capital. I’m writing this series because if you better understand how VC firms work you can better target which firms make sense for you to speak with. It in not uncommon to see a VC talk about “total assets under management&# as in “We have $1.5

To see the video of This Week in VC click on this link. What a pleasure that I got to spend an hour talking with both Om Malik (whom I’ve always respected his views) and Paul Jozefak , a venture capital partner at Neuhaus Partners in Germany (and formerly the head of Europe for SAP Ventures). But it’s a real phenomenon.

The truth is that I’ve been warning about convertible notes since 2010 it was first declared that “convertible notes have won.” ” Today I want to talk about how a VC thinks about equity pricing on your round and particularly if you’re coming off of a convertible note. It’s very simple.

Peer-to-peer lending service; started on FaceBook; claim to own 79% of the US peer lending market in March 2010 with a whopping $8,664,750. Investors: Foundation Capital (lead), with existing investors: Morgenthaler Ventures, Norwest Venture Partners, Canaan Partners. Investors: Union Square (lead), Spark Capital (lead).

It’s always fun chatting with Jason because he’s knowledgeable about the market, quick on topics and pushes me to talk more about VC / entrepreneur issues. Next Wednesday we’ll have Dana Settle of Greycroft Partners, a New York / LA early-stage venture capital fund. I’d link to it but it’s behind a paywall.

On the third Wednesday of every month I co-chair a meeting called the SoCal VCA (venture capital alliance), which represents participants from all of the top venture capital firms in Southern California as well as prominent members of the Tech Coast Angels (TCA). with only 19% saying they would decrease levels.

This is where VC comes in and why it’s needed in the industry no matter how much populist sentiment exists against the VC industry. I know that in late 2010 it’s not as popular to say this because we’re in the era of “super angels&# and feel-good startups. It’s hard to say.

I met him in April of 2010--almost two years before he got a venture round. It took almost two years for the company to raise their first outside capital from RTP and Greycroft--and honestly, my bad for not staying close to the company. It would be over two years until he took his first round of capital earlier in 2012.

There has been this narrative about investing in VC funds that you have to get into the top quartile (25%) or possibly the top decile (10%) in order to generate good returns. I have heard that for as long as I have been in VC and probably have written it here a few times. As you can see, investing in VC funds can be very profitable.

It was especially fun for me because we got the chance to talk about the VC industry and how entrepreneurs should think about the VC industry in addition to discussing deals. Segment Three: “VC Deals Funded this Week”. 14mm in Series C; $25mm in Series B raised in March 2010; $44mm raised in total. LivingSocial.

This was really a fun week at TWiVC because we decided to have an entrepreneur come and talk about raising capital rather than having a VC come on. In particular I tried to do most of the “entrepreneur advice on VC” up front so that if you don’t want to watch our views on the deals you don’t have to. OTHER DEALS: 1.

If you want to raise venture capital more easily the advice could be quite practical and counter-intuitive. It is 2010. Many companies that are raising B or C venture capital rounds right now raised their initial money in 2005-2008. That means that they likely raised money at a particularly high price relative to 2010 prices.

However, in this moment, I think one''s career in venture capital depends on changing your perspective. The biggest question I think VC''s face right now is whether or not, in the future, the best founders will look and act like the best founders of the past. Venture Capital & Technology' That''s 25%.

As a result I didn’t write my first venture capital check until March 2009 – exactly 5 years ago. In 2010 somebody posed the question on Quora, “Is Mark Suster a Successful Venture Capitalist?” Helping companies get to next financing round successfully: I was just beginning this phase in Sept 2010 and said so.

Over the past month a colleague ( Chang Xu ) and I sifted through data on the venture capital industry (as we do every year) and made a bunch of calls to VCs and LPs to confirm our hypotheses. As a result of the IPO window shifting we saw a massive inflow of public-market capital into the latest stages of venture.

And that was evident on today’s Angel vs. VC panel. There are real changes in the venture capital industry and it would have been fun to talk about them. The VC industry is segmenting – I have spoken about this many times before. So in the past we needed VC to really get a startup going. Answer: Not much.

This is part of my ongoing series “ Start Up Advice &# but I’d really like to call this post, “VC Advice.&#. We exchanged ideas when I was an entrepreneur along side him in NorCal in 05-07 and my point-of-view on founder / VC relationships hasn’t shifted even 1% since I went to the dark side. You lose the dream.

Having spent time around and then in the world of VC in the Bay Area during the last decade, I’ve been reflecting on how different norms in the industry have changed. At the start of 2010, there was some unwritten VC industry conventions that have been tested, challenged, and upended in the last decade.

I’m often asked about the differences between being at a VC and being an entrepreneur and whether I prefer one or the other. The biggest difference I cite is that Venture Capital often feels like an “individual sport” while startups are a “team sport.” It was more hedge fund than venture capital.

Our first Opportunity Fund, raised two years later in 2010, has generated only 3.9x That explains why our 2010 Opportunity Fund has a lower cash on cash return but a much higher IRR than our 2008 early-stage fund. Our 2014 Opportunity Fund has a higher cash on cash return but a lower IRR than our 2010 Opportunity Fund.

They have marked-up paper gains propped up by an over excited venture capital market that has validated their investments. We haven’t hit that wall yet for three reasons: 1) not enough elapsed time, 2) the VC market is frenzied now, too and 3) we haven’t seen a market downturn since the volume picked up.

So I saw this tweet by Semil Shah yesterday: A friend who works in an industry far from tech startups & VC asked what would be the single article I’d share to read on each topic. So I clicked on the link to my Competing To Win Deals post, which I wrote in 2010, and read it. That is a failure of the system.

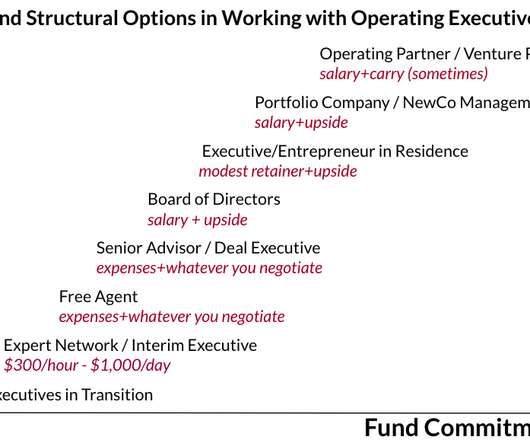

Would you like to work with private equity and venture capital funds? There are relatively few jobs directly inside private equity and venture capital funds, and those jobs are highly competitive. See How to negotiate a partner role at a VC or private equity firm.) At Versatile VC , we’ve used all these models.

This is where VC comes in and why it’s needed in the industry no matter how much populist sentiment exists agains the industry. I know that in late 2010 it’s not as popular to say this because we’re in the era of “super angels&# and feel good startups. got picked up early without raising a lot of VC.

Now that he’s become a VC he’s promising me he’ll provide way more public information and discourse so please welcome him by following him on Twitter and better yet welcoming him with a Tweet of your own linking to his Twitter handle or this post. And he followed through. So he had had a taste of it.

I recently read a blog post by Beezer Clarkson, Managing Director of Sapphire Ventures about why entrepreneurs should care about from whom their VC funds raise their capital. There are a lot of things I think entrepreneurs should care about when raising from a VC: How big or small their fund is? Beezer did.

This is part of a series that I’ve been working on called Understanding Venture Capital. This led Roy Rodenstein (whose company Going.com was sold to AOL ) and others to discuss , what happens when VC’s need to invest across multiple funds. And VC’s don’t like to invest across multiple funds.

For years there has been a pervasive opinion across the entrepreneurial landscape that the US has a shortage of capital required to startup and grow new ventures. But, what evidence do we have of this shortage of capital? Let’s take a closer look at trends in government grants, angel investment and venture capital financings.

2/ The massive experiment in using capital as a moat to build startups into sustainable businesses has now played out and we can call it a failure for the most part. When I look back at the 2010s, I see a decade during which massive capital flowed into startups and much of it was wasted chasing the “capital as a moat” model.

Despite the growth in awarded venture capital (VC) funds, a staggering disparity remains between the amount of total VC funds invested in entrepreneurs and the portion of those funds invested in ventures founded and/or led by women—particularly women of color. I am no stranger to this gender gap within the VC space.

We raised a seed round of capital in 1999 and our first venture capital round was the first week of March 2000 (e.g. We were now set to close at $46 million in new capital. We found a way to get a round of venture capital closed after all of this. So no prizes for guessing my New Year’s resolution for 2010.

Paul Martino, General Partner at Bullpen Capital. During our recent Dreamit Kickoff week, Bullpen Capital Founder and General Partner Paul Martino ( @ahpah ) spoke with our Spring 2020 cohort about the state of the VC ecosystem in the current economic crisis. Will a financial crisis affect how venture funds deploy capital?

In 2014, I published a post called Do Startup Require Less Capital to Succeed than 10 Years Ago ? In the analysis, I created a metric, the return on invested capital (ROIC). In other words, at IPO, how much revenue per VC dollar did the company generate. In 2010, one venture dollar bought $1.24 of revenue at IPO.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content