This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

To see the video of This Week in VC click on this link. We spent the first 45 minutes or so talking about industry trends (in this order): The history and background of True Ventures, one of my favorite early-stage VC’s (and the one with whom Om is a venture partner). first vertical to launch by 2010 Holiday Season.

There are obvious reasons the industry has had less-than-desirable returns, including: massive over-funding of the sector, huge increases in inexperienced venture capitalists that took a decade to peter out, and the massive correction in the value of the public stock markets that closed many exit opportunities for half a decade.

But I guess you could say the same about VC. Stock market declines would bring back dog days of VC. If you want a comprehensive summary of the industry in this era it’s worth a read: VC Ice Age Part 1 – What Happens When a Market Comes to a Standstill? VC Ice Age Part 2 – Why the Market Started Moving Again?

The biggest question I think VC''s face right now is whether or not, in the future, the best founders will look and act like the best founders of the past. My own track record as a VC across First Round Capital and Brooklyn Bridge Ventures actually starts in January of 2010, *after* the Airbnb class of Winter 2009.

Our first Opportunity Fund, raised two years later in 2010, has generated only 3.9x And our second Opportunity Fund, raised in 2014, has generated 7.3x Our Opportunity Funds invest in the later stage rounds of our top-performing portfolio companies plus a few later-stage investments in companies that are new to USV.

So I saw this tweet by Semil Shah yesterday: A friend who works in an industry far from tech startups & VC asked what would be the single article I’d share to read on each topic. So I clicked on the link to my Competing To Win Deals post, which I wrote in 2010, and read it. That is a failure of the system.

Now that he’s become a VC he’s promising me he’ll provide way more public information and discourse so please welcome him by following him on Twitter and better yet welcoming him with a Tweet of your own linking to his Twitter handle or this post. And he followed through. So he had had a taste of it.

It all started in 2010 with Klout. From this debate about Klout John and I have had a series of in person meetings and debates about our industry (both VC & tech) and what is changing. 2:00 Why don’t you like the term VC? 7:00 80% of the VC funds last year went to a small handful of funds. SHOW NOTES.

In January of 2010, just a few months after I joined First Round Capital, I got to back my friend Rob May and his company, Backupify. Yesterday, I closed on this "golden" opportunity and so I thought I'd reflect a bit on how the 50 looked as a group. Well, most of them are still alive, so that's cool. Others, not so much.

It highlights important events in the continent’s tech ecosystem until this point, compares its journey with other emerging markets and provides guidance into the opportunities within various sectors. And though they are inclined to follow the money, Endeavor wants them to look beyond usual market opportunities and map out exit pathways.

I saw a few friends politely suggesting that “now was a great stock buying opportunity” meaning that given the stock market is off by 10% it was a great chance to buy and lock in presumably low prices before the market rises again. The impact hits VCs in an immediate way that most entrepreneurs don’t realize.

According to PitchBook , VC investments were down 30% in Q2 2022 compared with 2021, and IPOs hit a 50-year low. When deal-making slows, VC dollars typically favor the perceived market leader, starving other venture-backed businesses in the same space of capital. This is your opportunity to establish the narrative.

Part of our mission at Draper Esprit is to democratize venture capital, as Simon would say; and [being listed on the main market] increases that opportunity. If you go back to 2010, we launched our [Enterprise Investment Scheme] product — in the U.K., funds with an angle on technology. It’s the former.

They wanted opportunity. I know because I went back a second time with 75 or so tech executives and VCs and my inbox is flooded this morning. Catherine (Cat) Hoke founded the program in 2010 and launched the business plan competition in 2012. And they didn’t want pity. They wanted to learn. I made a mistake when I was 19.

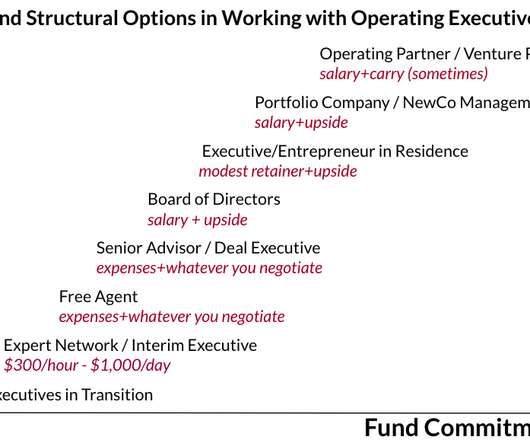

See How to negotiate a partner role at a VC or private equity firm.) At Versatile VC , we’ve used all these models. Thank you to my co-author for this essay, Paulina Symala, a Consultant at Oliver Wyman and a past intern of Versatile VC. Would you like to work with private equity and venture capital funds? Expert Networks.

Despite the growth in awarded venture capital (VC) funds, a staggering disparity remains between the amount of total VC funds invested in entrepreneurs and the portion of those funds invested in ventures founded and/or led by women—particularly women of color. I am no stranger to this gender gap within the VC space.

Just two years later, in 2009, we worked out a deal to create the Techstars Seattle program, with our first program running in 2010. As the YC example shows, Techstars had the opportunity to build one of the world’s top investing platforms for technical founders in every major tech hub outside the Bay Area.

The organization managed to land a $5 million prize, due in part to research Beth Zotter had begun in 2010. Given the the generally horrifying trajectory the planet has been on for the last several decades, most VC firms are looking for some positive climate investments. But the tricky bit is always the “C” in “VC.”

In fact, Heddleston worked for Dropbox as a summer in intern in 2010. In fact, among the earliest use cases for the company was helping startups track engagement with their pitch decks at VC firms. Houston and DocSend co-founder and CEO Russ Heddleston have known each for other years, and have an established relationship.

According to the Center for Venture Research, The Angel Investor Market in 2010 was about $20 billion and funded about 60,000 companies, with about one-third of that capital committed to seed/startup stage companies. Total angel funding in 2010 was up somewhat, but has ranged from $15 to $20 billion for several years.

Founded in 2010, Pipedrive’s calling card has always been that it is sales software designed to serve first and foremost the needs of sales people not their managers — built by sales people, for sales people, if you like — but has since matured into a more comprehensive CRM platform play also spanning marketing.

As operators, we were lucky to raise from some pretty amazing VC role models, people like Brad Feld at Foundry Group, Ethan Kurzweil at Bessemer Venture Partners, and Karan Mehandru at Trinity Ventures. But along the way we experienced many of the behaviors Fred’s post talks about, so we know how awful the experience of raising VC can be.

Brett Calhoun Contributor Share on Twitter Brett Calhoun is the managing director and general partner at Redbud VC. Amid these turbulent times, the VC accelerator industry has emerged as a stalwart player. Concurrently, the number of funds raised in the eight-year period up to 2022 was 2,700 , up from 883 in 2010.

Investors are excited about the opportunities in the space market that are being unlocked by exit events and continued interest and private investment in the biggest and most successful space companies, including SpaceX.

In 2010, we were first hearing about the iPad, Facebook had just turned cash flow positive, and most people were celebrating (rather than criticizing) the growth of Silicon Valley and what was starting to be known as Big Tech. And entrepreneurs see the opportunity, creating tools and services to help consumers stay fit.

The only model of institutional seed funding was the “business incubator” model, where VC firms would fund well-connected founders they knew and incubate them in their office. This was the key insight that led to the creation of YC, and also to the hundreds of institutional seed funds that sprung up to take advantage of the new opportunity.

Maybe this is reverse “hanging around the rim” where if you keep you VC process going long enough you’ll eventually get to “yes?” I once had a potential LP back in 2010 (when fund-raising as a VC was harder for me) tell me that he thought he was a better fit to look at our next fund rather than this one.

He joined Goldman Sachs in 2010 and grew out the department’s strategy from a London office to back companies that could make good returns on the continent. South African fintech startup Jumo raises second $50M+ VC round. What we know (and don’t) about Goldman Sachs’ Africa VC investing.

We also learn how, under his watch and as the company began to scale, Klarna missed the next big opportunity in fintech, instead being usurped by Adyen and Stripe. But whatever the intent, it would be another two years before the firm eventually had the opportunity to invest in Klarna at what was almost certainly a much higher valuation.

So, with that Disclaimer, here are the main reasons seed stage firms have grown in size over the past decade, along with some risks and opportunities these conditions create: 1/ Catching Ambition – When some seed stage funds started, perhaps they didn’t know what their fund would turn into.

Including a substantial number of investments with smaller opportunities only reduces the possible return on the entire portfolio. We also have data points for VC investments in seed/startup companies (but not necessarily pre-revenue companies). Size of the Opportunity 0-25%.

Greycroft in 2010 also had an experienced team, but didn’t either. Many VC LPs are investing not just for returns, but because they want to learn more about the space, get access to co-investment opportunities, network with disrupters, etc. Emerging managers are not a commodity, especially in VC.

The argument threaded through Fred’s posts above is that significant venture-scale opportunities for VCs existed outside the Bay Area. Just like Sequoia with their franchise model, or Accel, or the other larger funs, the top-tier venture capital firms have scaled up and out to grab these opportunities.

This morning marked the kickoff of VC firm 500 Global’s Fall 2022 Demo Day, which saw over a dozen startups give their best pitches to prospective investors — and customers. It is a key vantage…but now it’s helped unlock other opportunities for us as a firm that we’re exploring with a lot of enthusiasm.”

Watch my interview from the SALT Abu Dhabi conference, where I was the first Israeli VC to speak publicly in the Gulf. . Exits inked throughout the 2010-2019 decade amount to $111 billion. Participate in a unique learning opportunity which will take place during the week of the 2020 OurCrowd Global Investor Summit.

But Ojansuu says that his view was shaped by his experiences working with customers at Gapps, a Finland-based Google Workspace reseller he helped to co-found in 2010. . ” Using Happeo’s editing tools to build an intranet portal.

Lerer Hippeau has invested in 400 portfolio companies since it was founded in 2010. TechCrunch: Ben, how does it feel to come back to VC full-time? Lerer: It’s nice of you to say “back to VC full-time.” VC still requires in-person connection, argues Madrona’s Matt McIlwain.

In 2010, Bastian Gotter invested up to $200,000 into IROKOtv, an African video-on-demand company Jason Njoku, his friend and co-founder, launched in Lagos, Nigeria. For Gotter, it was more of the latter, and so this January, he began to explore other opportunities in the mobile money payments space, specifically relating to small businesses.

s SB Opportunity Fund. TTV Capital led Welcome Tech’s latest capital infusion, which brings the company’s total raised to date to $70 million since its 2010 inception. Joining TTV in doubling down on their investment in the company were Owl Ventures, SoftBank’s Opportunity Fund, Mubadala Capital and Next Play Capital.

BoxGroup Strive is its second opportunity fund that will back companies in their subsequent follow-on rounds. The opportunity fund occasionally makes later-stage investments in new companies, but mostly just continues to support companies it invested in at an earlier stage. Each fund amounts to $127.5

in 2010 to €9.6B For instance, an increasing volume of genomics data coming out from large governmental projects creates an opportunity for biotech enthusiasts to launch startups. Investments in European deep tech grew in absolute numbers, however during 2015–2020 it remained between 20–26% of all VC investments.

We also learn how, under his watch and as the company began to scale, Klarna missed the next big opportunity in fintech, instead being usurped by Adyen and Stripe. But whatever the intent, it would be another two years before the firm eventually had the opportunity to invest in Klarna at what was almost certainly a much higher valuation.

Venture investment in renewables has soared as global investment in energy transition more than doubled from $235 billion in 2010 to $501 billion in 2020, according to Bloomberg NEF. Exciting Opportunities. These developments are creating exciting opportunities for investors. The rush to renewables is not a passing fad.

While several marketplace unicorns prepare IPOs, a VC digs into the data (EC). We also learn how, under his watch and as the company began to scale, Klarna missed the next big opportunity in fintech, instead being usurped by Adyen and Stripe. Wish wants to be the Amazon for the rest of us; will retail investors buy it? DoorDash, C3.ai

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content