This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Many observers of the venture capital industry have questioned whether its best days are behind it. I can’t help feel a bit of rear-view mirror analysis in all of “VC model is broken” bears in our industry. The most successful of these businesses will still need venture capital to scale their businesses. The Funding Problem.

how on Earth could the venture capital market stand still? One of the most common questions I’m asked by people intrigued by but also scared by venture capital and technology markets is some variant of, “Aren’t technology markets way overvalued? The market today would barely be recognizable by a time traveler from 2011.

In the first post in this three part series I described why I believe the VC market froze between September 2008 – April 2009. I obviously don’t have a crystal ball so the economy could fare better than my gut, but here’s why I’m cautious for some time in 2010 or early 2011: Why is the future still so unpredictable?

If you want a very quick primer on all the stuff nobody ever tells you about raising venture capital check out this video where Mark Jeffrey & I break it down on This Week in VC. All of this is covered in more detail on the TWiVC video above (and much of it is covered in text on this blog on the “ Raising VC &# tab).

Our guest this week on #TWiVC was Dana Settle , partner at Greycroft Partners , a venture capital firm with offices in New York and Los Angeles. Greycroft is an early-stage VC. Closing a VC fund in 2009/10 is a major achievement in and of itself. CEO hinted to WSJ that it may go public in early 2011. Go Boulder!

On the third Wednesday of every month I co-chair a meeting called the SoCal VCA (venture capital alliance), which represents participants from all of the top venture capital firms in Southern California as well as prominent members of the Tech Coast Angels (TCA). per year.

It took almost two years for the company to raise their first outside capital from RTP and Greycroft--and honestly, my bad for not staying close to the company. It would be over two years until he took his first round of capital earlier in 2012. In March of 2011, I asked Pat from GroupMe to introduce me to Linden Tibbets of IFTTT.

This is part of my series on Understanding Venture Capital. I’m writing this series because if you better understand how VC firms work you can better target which firms make sense for you to speak with. It in not uncommon to see a VC talk about “total assets under management&# as in “We have $1.5

We all have our inherent biases and what I am not arguing here is that the venture capital world is a fair playing field for anyone. I repeat: I AM NOT ARGUING THAT VENTURE CAPITAL IS FAIR TO ANYONE. We really don''t know, because we''re missing some critical information: HOW MANY WOMEN ARE SEEKING VENTURE CAPITAL?

This is where VC comes in and why it’s needed in the industry no matter how much populist sentiment exists against the VC industry. got picked up early without raising a lot of VC. If 2011 & 2012 look like 2010 then the current crop of angel investments will look great. So where are we now? It’s hard to say.

My partner Greg Bettinelli (worth following on Twitter) was recently named by The LA Business Journal as the “ Top deal maker in Los Angeles in Venture Capital.” I joined Upfront Ventures in 2007 and took over as co-Managing Partner in 2011 along with the founder, Yves Sisteron. ” Numero uno.

Because my role as a VC requires me to take and endless stream of meetings I long ago decided I need to learn as much as I can from the meetings I attend so I often just ask tons of questions and assimilate knowledge. When I think about what defines us as a VC I think: Operationally knowledgeable / strong startup competence.

I had witnessed a number of early-stage tech startups in LA raise seed capital from the Bay Area and relocate. By 2011 the market had started to change dramatically. Throughout all of these years I was a full-time VC so Launchpad really came out of evenings and weekends for me. We announced Fund I in 2011. And Jamie hers.

The part of the movement that resonates the most with me (in my words) is that entrepreneurs should keep their capital expenditures really low while they’re experimenting with their product and determining whether there is a large market for what they do. I believe that over capitalizing companies too early often favors the VC.

.&# That’s how it felt then and a bit how it feels in May 2011. I think that’s the beauty of both capitalism and innovation. People who comment to me privately about how surprised they are by how rapidly I’ve “built a name for myself in VC&# remind me of this fallacy. So which is it? Feast or famine?

There aren't many people who get the chance to analyze venture capital fund return data. Mattermark just posted a short report full of such statements and the former 21 year old institutional LP analyst in me (the job I got my VC start in over 15 years ago) flipped his s**t upon close review. So what percent of the market is that?

She worked for 5 years as a VC at Battery Ventures and co-headed M&A at IAC working with Barry Diller. Venture capital is about backing the leaders of tomorrow who imagine the world as it should be and aren’t constrained by what it is today. I promise you, he really said this out loud.) Wait, What About Yves?

I woke up to a dream this morning where I was playing a game that was very similar to Turntable.fm , a failed effort to create a social music experience that had a moment back in 2011 and that I had invested in via USV. It comes with the territory in VC. It was as fun to play it as it was to play Turntable back in the day.

Last year I was on Sand Hill Road in Silicon Valley meeting with one of the most prominent venture capital firms in the country. The VC partner, somebody I greatly respect said, “Yeah, we like Gil and what they’re doing. That’s convenience when your VC is hoping to write the next $20 million check.

2007, 2011) and for the hottest of companies and in bad markets for fund raising (2003, 2008) prices test the bottom end of the range. Prices have definitely gone up in 2011 as depicted in the anecdotal chart below. I’m a VC so I have an obvious bias. I saw this kind of pricing when I first entered the VC market in 2007.

Union Square Ventures (USV) has been one of the most successful venture capital firms of the past 10–15 years and continues to be a leader in our industry. Lindel is no stranger to thorny venture capital issues — he was arguably amongst the most successful LPs of his generation. Maybe that’s USV, too.

Monique Villa is an investor at Mucker Capital , an early-stage VC fund investing in startups across the U.S. Getting a seat at the VC table. The wave of venture capital interest in geographies other than Silicon Valley has been building momentum over the past 5+ years. VC deals by region, as of June 2019.

You have to understand whether they’re likely to yield revenue growth in the near term OR whether you have access to cheap enough capital to fund your losses until your investments pay off. Have easy access to capital by investors who are committed to building businesses at Interent scale. Internet scale.

I spoke about how Amazon Web Services deserves far more credit for the last 5 years of innovation than it gets credit for and how I believe they spawned the micro-VC category. I said that I felt that Micro-VCs were the most important change in our industry. It is great for entrepreneurs and great for VCs. source: Capital IQ.

This is where VC comes in and why it’s needed in the industry no matter how much populist sentiment exists agains the industry. got picked up early without raising a lot of VC. If 2011 & 2012 look like 2010 then the current crop of angel investors will look great. So where are we now? It’s hard to say.

For years there has been a pervasive opinion across the entrepreneurial landscape that the US has a shortage of capital required to startup and grow new ventures. But, what evidence do we have of this shortage of capital? Let’s take a closer look at trends in government grants, angel investment and venture capital financings.

When Marc and I started the firm in 2009, the conventional wisdom in Venture Capital was that in any given year, only 15 companies would ever generate $100M in revenue and those 15 companies would drive almost all of VC returns. Venture Capital firms configured themselves to address a market of 15 important companies.

Business writer Gordon Pitts pinpoints 2011 as the game-changing year for the Atlantic startup scene. In his book “Unicorn in the Woods: How East Coast Geeks and Dreamers are Changing the Game , ” Pitts recounts how in March 2011 Salesforce purchased New Brunswick-based social media monitoring company Radian6 for approximately $300 million.

The better takeaway is that high margin businesses are often less dependent on capital markets because they can internally generate cash more easily. Bill Gurley tweeted his blog post from 2011 that “ all revenue is not created equal.” That is not the case with low margin businesses.

When I moved back to the Bay Area in early 2011, the technology and startup sector didn’t feel as big or expansive as it does today. Now, contrast 2011 with 2019, and we have an entirely different situation. Today in 2019, this deal information among the top VC brands is only really moving through smaller, trusted networks.

Long before SoftBank launched its $2 billion Innovation Fund in Latin America, and before Andreessen Horowitz began actively investing in the region , Sao Paulo-based Kaszek has been putting money into promising startups since 2011, helping spawn nine unicorns along the way.

Brett Calhoun Contributor Share on Twitter Brett Calhoun is the managing director and general partner at Redbud VC. Amid these turbulent times, the VC accelerator industry has emerged as a stalwart player. Angel investments in 2022 equaled those from 2006 to 2011 combined. Crowdfunding witnessed a 2.4x growth from 2020 to 2021.

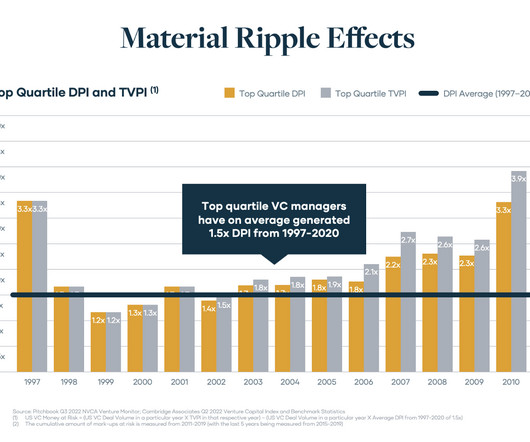

VC dollars are at risk, we conducted a historical analysis of top quartile fund managers over the past quarter century (as far back as we could access reliable Cambridge Associates data). We looked at the analysis in two parts: the 1997–2010 time period and the 2011–2020 time period. since 2011. But what could that look like?

You might not know yet of XYZ Venture Capital , a four-year-old, San Francisco-based seed-stage venture firm, but many veterans of Palantir are surely aware of it. At the same time, Fubini began raising his own pool of capital under the brand XYZ Ventures, eventually launching a $70 million fund.

Individual accredited investors in typical angel deals put personal capital at risk for an equity share of growth-oriented, start-up companies. In 2011, the valuation of pre-revenue, start-up companies is typically in the range of $1.5–$2.5 – Need venture capital. million, indicating a somewhat normal distribution.

Rachel Holt, co-founder and general partner, Construct Capital. HubStop introduced usage-based pricing in 2011 to boost its retention rate, then near 70%. “You have to wonder if every VC worth a damn in the future will have their own raft of SPAC offerings,” says Alex. Shawn Carolan, partner, Menlo Ventures.

He is also the founder and managing partner of HartBeat Ventures, an early-stage VC firm with a focus on lifestyle, media and technology. Forbes reports that while companies with white founders receive 77% of VC dollars, less than 10% go to women founders and less than 1% to Black founders. Venture funding inequity remains a big issue.

Medicai founder Mircea Popa’s journey in healthcare started in 2011 when, with a friend of his, he co-founded a company that is now called SkinVision, a skin cancer screening app that detects melanoma (skin cancer) through ML algorithms applied on images taken with smartphones. million), among others.

The Series D is being led by Qumra Capital, a late-stage VC firm based out of Israel ( Augury was founded in Haifa and now has a second HQ in New York), with participation also from Insight Venture Partners, Eclipse Ventures, Munich Re Venture Capital, Qualcomm Ventures and Lerer Hippeau Ventures — all past backers of the startup.

James covers the genesis of Ministry of Awesome following the Christchurch earthquakes in 2011, and provides updates on Ministry of Awesome approaches to startup founder support and programming. So it’s much less about raising capital, it’s much more about business fundamentals.

For example, Leading Edge Capital closed on nearly $2 billion for its sixth fund, Base10 Partners brought in $460 million for its third fund, Founders Fund secured $5 billion for two funds, Freestyle raised $130 million for its sixth fund and the list goes on and on. That’s new.”. Image Credits: Overlooked Ventures.

million in a Series B funding led by Finnish VC fund Evli Growth Partners, alongside previous investors Karma Ventures and LVV Group. We first covered the Vilnius-based company when it raised €200,000 from Practica Capital. 3D model provider CGTrader has raised $9.5 Ex-Rovio CEO Mikael Hed also invested and joins as board chairman.

The region’s startup scene saw a boom, with a large spike of fundraises in 2021 with VCcapital deployed totaling $15.9 Since 2011, Kaszek has backed more than 120 companies, which the firm says collectively have raised more than $15.5 billion in capital. billion in capital.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content