This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I’m over-paying for every check I write into the VC ecosystem and valuations are being pushed up to absurd levels and many of these valuations and companies won’t hold in the long term. However, to be a great VC you have to hold two conflicting ideas in your head at the same time. dot-com bonanza. Ten years on much has changed.

I’d rather be Roger Ehrenberg with a thesis around data-centric companies and base my investment decisions on the skills I’ve developed in my career. To some extent Keith Rabois agreed with me about domain knowledge and argued that most of his investments are in the consumer Internet space as a result. Always have been.

In the first post in this three part series I described why I believe the VC market froze between September 2008 – April 2009. I obviously don’t have a crystal ball so the economy could fare better than my gut, but here’s why I’m cautious for some time in 2010 or early 2011: Why is the future still so unpredictable?

If you want a very quick primer on all the stuff nobody ever tells you about raising venture capital check out this video where Mark Jeffrey & I break it down on This Week in VC. All of this is covered in more detail on the TWiVC video above (and much of it is covered in text on this blog on the “ Raising VC &# tab).

I woke up to a dream this morning where I was playing a game that was very similar to Turntable.fm , a failed effort to create a social music experience that had a moment back in 2011 and that I had invested in via USV. Investments that don’t work haunt me. It comes with the territory in VC. Then I woke up.

I’m writing this series because if you better understand how VC firms work you can better target which firms make sense for you to speak with. It in not uncommon to see a VC talk about “total assets under management&# as in “We have $1.5 What is a VC fund? VC’s don’t invest 100% of their own money.

This morning we heard from Jamie Montgomery, CEO of the venerable Montgomery & Co investment bank who is at the heart of what is going on in M&A for venture backed companies. They do around 7% of the total VC-backed deals in the US per year or just under 40 deals / year on average (present year excluded!). per year.

Greycroft is an early-stage VC. Closing a VC fund in 2009/10 is a major achievement in and of itself. In the intro section of the show we talked a lot about why VC funds are becoming smaller again and where Greycroft fits. CEO hinted to WSJ that it may go public in early 2011. Total raised: $16.5mm.

In March of 2011, I asked Pat from GroupMe to introduce me to Linden Tibbets of IFTTT. You're going to miss some stuff, and just because others invested doesn't make any of these companies winners quite yet, but I'm all about continuous improvement. Just a few days ago, he added a monster $10mm raise. I'm impressed.

I can’t help feel a bit of rear-view mirror analysis in all of “VC model is broken” bears in our industry. Looking ahead at the next decade I am excited by what I believe will be viewed as one of the best and most rational investment periods for venture capital due to seven discrete factors: 1. The Funding Problem. The Exit Problem.

I joined Upfront Ventures in 2007 and took over as co-Managing Partner in 2011 along with the founder, Yves Sisteron. I laid out the following goals: Hire investment partners with operating experience combined with investment experience and deeply committed to LA Tech, but with strong relationships in SF, NYC and beyond.

Because my role as a VC requires me to take and endless stream of meetings I long ago decided I need to learn as much as I can from the meetings I attend so I often just ask tons of questions and assimilate knowledge. When I think about what defines us as a VC I think: Operationally knowledgeable / strong startup competence.

I’d rather be Roger Ehrenberg with a thesis around data-centric companies and base my investment decisions on my background. I should say that I agree that naive optimism in entrepreneurs can produce higher beta (upside or flops) and that’s good from an investment standpoint if you’re looking for big returns.

With our 2020 Robotics + AI sessions event on the horizon in early March, we’re diving back into the sector to learn about the attributes of construction attracting robotics VCs the most and which types of startups VCs are actually writing checks for in 2020. How much time are you spending on construction robotics right now?

By 2011 the market had started to change dramatically. Throughout all of these years I was a full-time VC so Launchpad really came out of evenings and weekends for me. Throughout all of these years I was a full-time VC so Launchpad really came out of evenings and weekends for me. We announced Fund I in 2011.

She worked for 5 years as a VC at Battery Ventures and co-headed M&A at IAC working with Barry Diller. The core of the investing job of course is investing dollars into startup companies and helping as a mentor, advisor and board member on the companies in which you’ve invested. So What Does All This Mean?

The interview was wide ranging and discussed everything from USVs investment thesis over the past 10 years to what some emerging themes are around blockchain and artificial intelligence. Dan asked Fred about “generational change” at USV and in the VC industry more broadly. We as an industry have seen this.

” I found myself nodding through all of it with quotes like, “Seed investing is the status symbol of Silicon Valley,” said Sam Altman. I myself coined the term ENIFA (everyone now is a f **g angel) in 2011 but it didn’t stick as well as the term Unicorn did. All of my partners at Upfront do. Hua of Apptimize. ” Uhhuh.

It’s the whole basis of my investment philosophy, which I call “ The Entrepreneur Thesis.&#. I believe that over capitalizing companies too early often favors the VC. Talking about whether to raise more money or not, their VC allegedly said to them: “If you had more capital, could you get to the future faster?

The VC partner, somebody I greatly respect said, “Yeah, we like Gil and what they’re doing. And this Silicon Valley bias isn’t limited to any single meeting – it has been a recurring theme in my time as a VC. When you’re one fund and have $600 million to invest it’s easier to take that kind of risk.

If you invested in the first angel round of a startup company it is usually very hard to sell your stock – usually for many years if ever at all. The earlier you invest the higher the chances the company won’t work out and thus you pay a lower price than later-stage investors. Private markets for stocks are the opposite.

In 2008 I started VC blogging. In 2011 I started using Instagram. But how can you invest in technology unless you’re going to use the tools and understand them? In 2007 I started using Twitter and most of my friends & colleagues wondered why people would care what I ate for lunch. I had blogged when I was an entrepreneur.

Transitions do happen in VC funds but many fail to make the move in a timely fashion and lose key younger personnel who break off and do their own funds or else the strong personalities of senior partners make it harder for new partners to flourish. Fred & Brad aren’t leaving but wanted Andy & Albert to take over management.

You have to understand whether they’re likely to yield revenue growth in the near term OR whether you have access to cheap enough capital to fund your losses until your investments pay off. If you have a market lead then raising capital and making investments now will help you as others enter the market. ” The Details.

Our investment in Kickstarter back in 2009 is an excellent example of that. Our interest in web3 which started back in 2011 was also grounded in the idea that new forms of funding are necessary to finance innovation and creative work. That has led to all sorts of interesting projects which are too numerous to mention here.

I spoke about how Amazon Web Services deserves far more credit for the last 5 years of innovation than it gets credit for and how I believe they spawned the micro-VC category. I said that I felt that Micro-VCs were the most important change in our industry. It is great for entrepreneurs and great for VCs. I believe that.

Monique Villa is an investor at Mucker Capital , an early-stage VC fund investing in startups across the U.S. Getting a seat at the VC table. Meanwhile, VCs will approach founders saying, “We are now looking into markets beyond Silicon Valley.”. America is the opportunity and we are worthy of investment, aren’t we? “We”

So, if you''re going to argue that the process of venture capital is inherently unfair to women, here''s the logic that you *should not* use: "Less than 3 percent of the 6,793 companies that received venture capital from 2011-2013 were headed by a woman, according to a study from Babson College released Tuesday.

Not an investment philosophy “ I understand the sentiment of this post and it’s how I view AngelList (like email), but I feel like it loses a nuance about AngelList. Still, as a VC I value proprietary dealflow & long term relationships. That’s less interesting for me as a VC. I worry about that.&#.

Investing is humbling. At 60, with 35 years of venture investing experience, I still get most things wrong. I told him the story of how I bumped into Rikki Tahta walking through the garment district in NYC in the spring of 2011 and Rikki told me he was working on a Bitcoin startup. Which is why I like to keep things simple.

That was USV’s initial web2 thesis: USV in 140 characters: invest in large networks of engaged users, differentiated by user experience, and defensible though network effects — Brad Burnham (@BradUSV) June 8, 2011.

When Marc and I started the firm in 2009, the conventional wisdom in Venture Capital was that in any given year, only 15 companies would ever generate $100M in revenue and those 15 companies would drive almost all of VC returns. At that time, the conventional wisdom was right. Shortly after we started the firm, all that began to change.

Mattermark just posted a short report full of such statements and the former 21 year old institutional LP analyst in me (the job I got my VC start in over 15 years ago) flipped his s**t upon close review. VC funds raise money, on average, between every 3-4 years--and many more often than that. So what percent of the market is that?

I maintained an active Tumblog from before we invested in 2007 until October 2016, when I stopped posting there. never figured out how to turn Tumblr into a business and ending up losing its shirt on the investment. There was a time around 2010 and 2011 when Tumblr was the most engaging social platform that I was on. I just did.

Here are some of the takeaways: Some readers interpreted the post as arguing for only investing in high gross margin businesses. Bill Gurley tweeted his blog post from 2011 that “ all revenue is not created equal.” One of the best things about writing is all of the feedback you get.

When I moved back to the Bay Area in early 2011, the technology and startup sector didn’t feel as big or expansive as it does today. Now, contrast 2011 with 2019, and we have an entirely different situation. Now, contrast 2011 with 2019, and we have an entirely different situation.

Business writer Gordon Pitts pinpoints 2011 as the game-changing year for the Atlantic startup scene. In his book “Unicorn in the Woods: How East Coast Geeks and Dreamers are Changing the Game , ” Pitts recounts how in March 2011 Salesforce purchased New Brunswick-based social media monitoring company Radian6 for approximately $300 million.

These angel investors generally invest $25,000 to $100,000 in a round totaling $250,000 to $1,000,000. In 2011, the valuation of pre-revenue, start-up companies is typically in the range of $1.5–$2.5 Active angels invest in a diversified portfolio of 10 or more companies, usually spreading their investments over a few years.

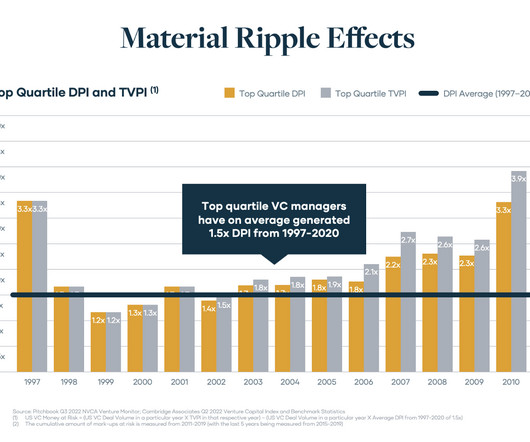

VC dollars are at risk, we conducted a historical analysis of top quartile fund managers over the past quarter century (as far back as we could access reliable Cambridge Associates data). We looked at the analysis in two parts: the 1997–2010 time period and the 2011–2020 time period. since 2011. since 2011.

Long before SoftBank launched its $2 billion Innovation Fund in Latin America, and before Andreessen Horowitz began actively investing in the region , Sao Paulo-based Kaszek has been putting money into promising startups since 2011, helping spawn nine unicorns along the way.

Brett Calhoun Contributor Share on Twitter Brett Calhoun is the managing director and general partner at Redbud VC. Amid these turbulent times, the VC accelerator industry has emerged as a stalwart player. Angel investments in 2022 equaled those from 2006 to 2011 combined. Crowdfunding witnessed a 2.4x

He is also the founder and managing partner of HartBeat Ventures, an early-stage VC firm with a focus on lifestyle, media and technology. What’s more, Hart’s investment company seems to accomplish this while maintaining a focus on inclusion — financial inclusion specifically. Venture funding inequity remains a big issue.

Transportation editor Kirsten Korosec reached out to 10 investors to learn more “about the state of mobility, which trends they’re most excited about and what they’re looking for in their next investments.” HubStop introduced usage-based pricing in 2011 to boost its retention rate, then near 70%. I, II and III.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content