This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I started in 2007 with a thesis that my primary investment decision would be about the team (70%) and only afterward about the market opportunity (30%). But they are also a tax on your time with portfolio companies, looking for new investments, running your shop and honestly they are a tax on your family life. I don’t.

In normal times investors will look for “traction&# before investing. I spoke about this more in depth in these two posts: 4 things I look for in an investment & how to manage VC relationships. I didn’t invest in Orgoo but by the time he launched Ad.ly This is happening with both angels and VCs.

The VC market has right-sized (returned back to mid 90′s levels & less competition). But it still takes VC to scale a business (thus large capital into industry winners like Uber, Airbnb, SnapChat, etc). But it still takes VC to scale a business (thus large capital into industry winners like Uber, Airbnb, SnapChat, etc).

I usually direct people to this post --still hanging atop the search rankings for " How to be a VC analyst" years later. That''s kind of like what it''s like being on board with these companies after you make an early stage investment. In VC, no one''s investment gets bought on the first day, or the second day, or the third day.

Lots of discussion these days about the changes in the VC industry. The VC industry grew dramatically as a result of the Internet bubble - Before the Internet bubble the people who invested in VC funds (called LPs or Limited Partners) put about $50 billion into the industry and by 2001 this had grown precipitously to around $250 billion.

I recently got an email from a friend who had been approached by a well known VC. I’m an investor at [Big Name, Large Fund VC] and recently came across [Your Company]. It's big, well known & we've invested in all of these really cool companies]. Why do VCs send generic outbound emails like this?

Learn how to pass a VC associate screen in under 10 minutes! Alana suggests that before speaking to an associate, you gain a basic understanding of the fund’s focus and stages they invest in. It means you haven’t properly framed this deal in the associate’s mind and that makes it hard for us to come to a definitive conclusion.

I believe the rise in angel investing is here to stay and the professionalization of this class (aka “super angels&# or “micro VC&# ) is a good thing for the VC industry and for entrepreneurs. But I fear that for most angel investors who invest over the long haul angel investing will not be a profitable endeavor.

A few years ago it became fashionable for large VC’s to do seed funding. If the large VC doesn’t agree to do your A round then you’re in a bit of trouble. But I’m no longer an entrepreneur – I’m a VC at a $200 million fund called GRP Ventures , the largest active fund in Southern California.

By definition?—?I’m I’m over-paying for every check I write into the VC ecosystem and valuations are being pushed up to absurd levels and many of these valuations and companies won’t hold in the long term. However, to be a great VC you have to hold two conflicting ideas in your head at the same time.

How about as a VC? He hasn't founded or built either a successful, let alone innovative company, and he hasn't raised $ to invest in those entrepreneurs. Fred has basically always been a VC, Mike was a reporter, and Jim worked in product marketing and management consulting. "Charlie is a nice guy, but his company failed.".

If you want a very quick primer on all the stuff nobody ever tells you about raising venture capital check out this video where Mark Jeffrey & I break it down on This Week in VC. All of this is covered in more detail on the TWiVC video above (and much of it is covered in text on this blog on the “ Raising VC &# tab).

And we all know that Ron Conway is considered the savviest of angel investors and yet by definition not all of his investments succeed. I like to invest where I have a personally strong connection with the entrepreneur and/or a strong intuition on the market from prior experience. Who ultimately invested in FourSquare?

Because it is a “series&# I plan to get into some of the deeper complexities of funds such as “cross over funds&# and “why VC’s hate to price their own deals&# at a later stage. First, if the VC does 15-20 of these under one partner then it is certain he can’t spend any time with these investments.

.” From the hyperbolic Jason Calacanis weighing in that “The petty VC’s did everything to deride [Naval, the co-founder of AngelList]” as though the industry was collectively s g its pants that AngelList was going to put us out of business. This is the same way VC firms, by the way. So there you have it.

Three companies most definitely makes a pattern. You're going to miss some stuff, and just because others invested doesn't make any of these companies winners quite yet, but I'm all about continuous improvement. Linden's a cool dude and being the interchange between the internet of things, our social services, etc.

When you get an investment from Brooklyn Bridge Ventures—you get me. My investment thesis is shaped by the sum of my personal experience and so are my values. My goal is to make Brooklyn Bridge Ventures the most accessible VC firm not just because I think it’s good business, but because I think it’s a based on good values.

” This is a frequent theme of mine when asked to speak to audience about the VC industry. And this is fueled by the VC culture in Silicon Valley. I was recently talking to a VC about a business I was looking at and I was asking whether he found the business interesting, too. It is VC math, like it or not.

I became a VC 12 years ago in 2007 when the pace of deals was much slower. As I was trying to figure out the role I wanted to play in the VC world I decided I wanted to focus on businesses that were building deeply technical products to solve problems for business users. We not only have our Series A funds that can write $500k?—?$15

Marc Andreessen kicked off another great debate on Twitter last night, one that I’ve been talking about incessantly in private circles for the past 2-3 years – what actually IS the definition of a seed vs. A-round. My view: “Spending any time or energy trying to game the ‘definition’ of your round of fund raising is a total waste.

Then I realized that it's probably not obvious what the dynamics are around how VCs tend to get introduced to companies and what works best for people, so I figured I'd blog about it. A lot of VCs ask to be introduced through someone. And these represent some of our most successful investments. Would you invest in it.

Age, gender, sexual orientation, religion, etc are all topics that are deeply emotional for people--and, by definition, personal. Of course, you don't always need that experience from a VC. If you make a comment about age, it will always be taken in the context of how old you are versus how old your audience is.

When this first ran on TechCrunch I got the greatest comment in the world that I had to repeat here, “VC’s are like martinis: the first is good, the second one great, and the third is a headache.&# I understand the appeal of having many VC firms on your cap table. These are all dumb reason to invest – of course.

Whilst there are a wide range of LPs and you could have first meetings for months (and many VCs do), there is probably a much smaller number of LPs who want to invest in a fund your size, with your focus, and whose minimum or maximum check size lines up with what you’re seeking. Why Buy Me? For Upfront, it’s about Los Angeles.

I''m just trying to invest in the best opportunities. I can definitely think of a few people I met with and said, "Well, that person was kind of a jerk" or they just had a bad personality--and they went on to build seemingly successful businesses. You''ve been in VC long enough to see lots of different funds, partners and deals.

A recurring theme in a lot of my BSList posts is that, if an investor thinks they can make a boatload of money with you, they’ll go to all sorts of lengths to invest. That includes investing way earlier than they would normally, investing outside of scope, investing with their personal capital outside of the fund, etc.

And that was evident on today’s Angel vs. VC panel. The VC industry is segmenting – I have spoken about this many times before. The VC industry has different segments in it that have different fund sizes, different investment amounts and different risk / return expectations. Answer: Not much.

Last week, there was a Business Insider article measuring the percent of female founded companies that NYC seed funds invest in. That means you actually have a *better* shot, statistically, of getting VCinvestment at these firms, statistically, once you actually pitch. In truth, that''s what''s actually driving my investments.

Ok, back to the VC content marketing. As a result I’ve seen hundreds of VC decks, all certain they will be among the top performers. Most strategies are some combination of innovation and best practices along the classic five steps of venture investing: See, Pick, Win, Service, Exit. This post is about ‘seeing.’

I was having a conversation last night with another VC who was suggesting I monetize the pro-ratas that I don't take by creating SPVs. It made me think of an investment I just made where the entrepreneur found an extremely profitable niche that he is already taking advantage of. But you could charge fees or at least carry for that.

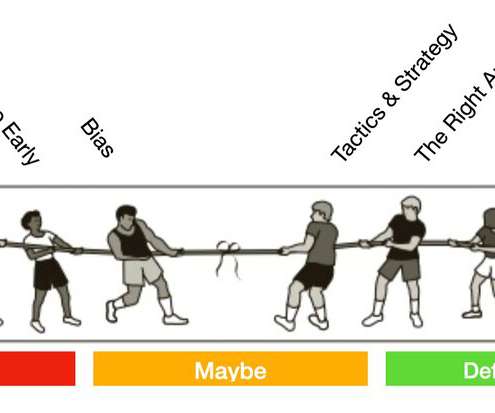

Any VC will tell you that the ones they said yes to, they mostly got there right away—and that there are very few “maybe” deals that get tipped over the fence. Here’s the way I look at the math: Let’s go over the structural bias first—the “pipeline” that happens before you ever even get near a VC. First is network bias.

I spoke about how Amazon Web Services deserves far more credit for the last 5 years of innovation than it gets credit for and how I believe they spawned the micro-VC category. I said that I felt that Micro-VCs were the most important change in our industry. It is great for entrepreneurs and great for VCs. I believe that.

When I described to people why I initially invested my calls went something like this, “He’s taken kicks to the face for nearly 2 years and is still standing. I was sick of hyperbole articles pronouncing that VCs were “scared or AngelList&# or “it was disrupting VC&# or some other BS exaggeration like that.

But in my experience as an entrepreneur and now spending my time amongst investors I can generalize that almost all VCinvestments in early stage technology & Internet investments come down to just four key factors. And VC’s are tough customers. I obviously don’t speak for all investors.

I’ve been meeting with LPs (those who invest in VC funds) over the past year and discussing trends I see in the market and where I think we need to be as a firm to be near to and meet the needs of our customers. I think NY has always – by definition – been urban. These days it’s Santa Monica and Venice.

The interview was wide ranging and discussed everything from USVs investment thesis over the past 10 years to what some emerging themes are around blockchain and artificial intelligence. Dan asked Fred about “generational change” at USV and in the VC industry more broadly.

If the deal is from out of your geography and/or out of your focus area or a deal is being referred by a well-know investor who normally co-invests with similar syndicates – at least ask yourself, “Why am I so lucky to be getting this call.” Fred Wilson said it best in his post about loss ratios in VC.

Since then, I’ve founded several startups, was employee #3 at a $65m VC firm in San Francisco, and realized that there is a similar phenomenon to what Robert Kiyosaki is talking about in Rich Dad, Poor Dad currently occurring in Silicon Valley. Wealth My definition of rich is having a passive income that’s greater than your burn.

One of the least understood parts of the venture capital industry and venture capital firms is how investment decisions actually get made. For anything that would be considered a normal investment for the partnership most firms try to make sure every partner has seen the deal and has a chance to weigh in.

Remember that we're lucky to be investing in your company, because ideas as good as yours don't come around too often, and that will change your approach as you try to gather your first check. There was a time not too long ago when VC bios read "Fab investor", "Quirky investor", and "Gilt investor". No one is perfect.

There was a brief, beautiful moment for a few months in 2021 when it felt like robotic investments might be immune from broader market forces. Image Credits: Crunchbase A couple of top line points: 2022 was the second worst year for robotics investments over the past five years. Uncertainty doesn’t breed investing confidence.

Recently I wrote a post arguing to make the definition of a Startup more inclusive than that to which Silicon Valley, fueled by Venture Capital return profiles, would sometimes like to attach to the word. Think USV is only invested around Union Square in NYC? This article originally appeared on TechCrunch. Think again. Angry Birds?

I’m enjoying being a VC. I thought I’d talk a bit about the differences I’ve experienced between being an entrepreneur & a VC – you know, from “both sides of the table.&#. I’m sure everybody has their own definition of the attributes of an entrepreneur. VC meetings going well. 2 million in VC.

Understand what investors are looking for , what they usually invest in, and why. There is a vast gulf between a ‘cool product’ and an ‘investable company’ and if you don’t understand the difference, you will be doomed before you start. Now, and only now, are you prepared to start fundraising.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content