This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

There’s a growing market for private cellular networks, or dedicated cell networks configured to support a company’s specific requirements within a confined area (think a warehouse or wind farm). But that hasn’t stopped new ventures from cropping up to challenge the incumbents.

We look at huge markets where there are large incumbents that might not be incented to innovate or react to what they perceive as an insurgent. It had the audience, the people, the network, everything! The networks seem to be emphatic about monetization for the present. I run Revolution’s VC investments.

First, they believe that the current offerings from the financial incumbents are lacking. banking system is the Automated Clearing House network, broadly known as ACH. This supposedly “electronic” network enables people to transfer funds from one bank account to another. The basis of this argument is really two fold.

Monzo’s culture of customer obsession allowed it to use the crisis to thoughtfully build a beloved consumer and SMB product that has changed personal finance in the UK. 2 Incumbent banks miss the mark in two crucial areas: The banking experience has not evolved to match modern consumer. This did not happen by magic. expectations.

venture capital deals, a spike in mega-financings where it’s common to see not only $100M private rounds, but companies that raise two or three types of financings like this in the same calendar year!

individuals give money and personal data to network operators in exchange for access to information. “In In Web3 there is a possibility — not saying that it’s going to actually 100% gonna happen — but there is a possibility where the network owns the network,” said Rubin. In today’s Web 2.0,

” Going up against incumbents. Third-party providers, mostly fintechs, have tried to capture some market share from these incumbents. ” The Dakar-based platform is akin to PayPal (with mobile money accounts, not bank accounts) runs an agent network that uses their cash on hand to service Wave users. .”

50B) due to the network effects it has created with its unique merchant loyalty program.”. Chau, Adamson and Simair all also co-founded SkipTheDishes, which Chau says has gone on to become the “largest food delivery network in Canada,” with 3,000 employees; it was acquired by Just Eat for approximately $86 million.

The team soon saw issues: “One of the largest modals of failure of the previous iteration was that payments and payment networks only interact with one user account.” Many standard joint accounts just give every user entire access to other users’ finances, while Zeta wants to give folks a more flexible way to share money.

Tile , the maker of Bluetooth-powered lost item finder beacons and, more recently, a staunch Apple critic , announced today it has raised $40 million in non-dilutive debt financing from Capital IP. When items go missing, the Tile app leverages Bluetooth to find the items and can make them play a sound. Image Credits: Tile.

It also plans to soon offer embedded finance products. Additionally, Melonn works with a range of transportation providers, including incumbents such as FedEx or DHL and last-mile startups, to reduce shipping times and costs. . And in January, fulfillment is up 20% compared to November of 2021. So, just how does it work?

As Paul Uhrig, Chief Legal and Digital Health Officer of Bassett Healthcare Network and Executive Director of Bassett Innovation Center told us, “if we can get the ultimate user excited and to be champions about this, that I found to be very much the winning strategy.”

Local payment methods account for 68% of online sales, and, depending on the region and merchant networks, merchants must integrate dozens of payment service providers. Meanwhile, cash voucher systems like Brazil’s boleto bancário and Mexico’s Oxxo payment network account for a significant share of Latin American consumer transactions.

T he startup uses blockchain with the aim of creating a richer network effect of data that allows credit bureaus and others to predict the creditworthiness of people who are not in the traditional credit bureau system. We’re exploring standing up unique information sharing networks.”.

For example, a sense of needing to keep up with these technology advancements from leadership can be translated down to a VP of Consumer Finance who needs to grow a consumer banking app while battling fintech upstarts and who may be thinking about using AI products to do so–which your product could help enable.

Challenger banks continue to make significant waves in the world of finance, with smaller outfits luring customers away from incumbents by providing an easier way for them to not only engage with basic banking services, but to tap into a wave of technology that brings more personalization and often better deals into the equation.

We don’t want to be elitist, we don’t want to do this for a very small category of people because we really want to become the incumbent bank in the U.S.,” Mos’ initial debit card has a few key features, including zero overdraft fees, late fees, or in-network ATM fees. Yahyaoui said, starting with students. Image Credits: Mos.

TechCrunch’s Kate Clark has done a round-up of the largest “private VC” rounds of 2018, and there’s a whole other list for just $100M+ financings led by Softbank’s Vision Fund. Speaking of acquisitions — many leaders of larger VC funds have privately given up on the incumbents buying their companies.

And save from mPharma, which has a network of Mutti pharmacies and recently raised $35 million to build out its telehealth and e-commerce offerings, funding has been few and far between for B2B distribution healthtech startups. However, a direct path to multi-national telemedicine scale through these chains is not clear, the report contended.

Jarkata-based Astro, which provides 15-minute grocery delivery, has recently closed a $60 million Series B financing round, lifting its total funding to $90 million since the business launched just nine months ago. The startup is competing with incumbents like Sayurbox, HappyFresh and TaniHub to win over users.

Sila will use the new funding to increase headcount, target additional partners and expand product features, including its Ethereum MainNet stablecoin issuance and interoperability between FedWire and the Nacha Automated Clearing House network. There is a massive wave of fintechs emerging in the U.S.,

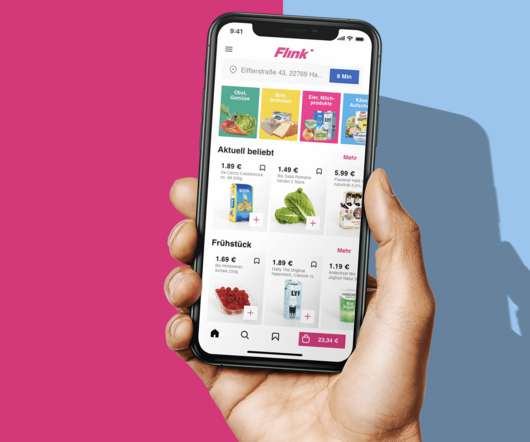

The latest to show its hand is Berlin-based Flink , which today is announcing that it has raised a hefty $52 million in seed financing. Officially launched just six weeks ago, Flink, which means “quick” in German, claims to deliver groceries from its own network of fulfilment centres in under 10 minutes.

But there is an even better vision of softPOS acceptance that goes beyond Apple’s: one that is built on an open platform, where all devices and all card networks are welcome, payment data is truly secured to the highest standards, and platforms are easily scalable. The meteor is about to hit. And we’ll all be better off for it.

Led by Lindsay Holden, the startup had raised more than $20 million in funding and had built a gamified finance mobile app that aims to help people “save, learn and engage” with their finances. In other words, incumbents in some cases need fintechs even as they compete with them. million in a round led by Firebrand Ventures.

With the latest Series A financing, Nelo has raised a total of $25.6 This captive consumer base is crucial to building the network that is Nelo.”. Two Sigma Ventures Partner Frances Schwiep believes that Nelo has the potential to emerge as the leading financing option for consumers in LatAm, starting with BNPL.

What’s really impressive with this round is that it is primarily financed by existing investors,” Lydia co-founder and CEO Cyril Chiche told me. Users can get a virtual or physical debit card that works on the Visa network. He doesn’t think it’s a duel between neobanks and incumbents. Times are changing. Image Credits: Lydia.

These platforms have become popular with neobanks or upstarts in different segments trying to embed financial services into their offerings because large, incumbent banks have been relatively slow to bring their services up to speed with the pace of change in the world of tech and banking.

Snafus can happen even when incumbents and fintechs partner. On outage tracker DownDetector.com, irate customers reported missing funds and unexpected negative balances due to problems with the digital payment network.” Reports Fintech Finance News: Turkish fintech company “ Papara. Reports CFO Dive : “Wilmington N.C.

Execs from the two startups say the combined company will have processed over $5 billion in payments and built a network of over 500,000 connected businesses by creating B2B DeFi payment networks in both the U.S. Apple alum’s finance operations startup Bluecopa raises funds to expand globally. and Mexico. Seen on TechCrunch.

Plaid is Current’s first partner on the product, which the two companies say will give Current’s customers access to more than 6,000 apps and services powered by the data aggregator’s network. . But he almost didn’t, when he had trouble securing the necessary financing to pay his tuition. Ali Heron, Petal CTO. Funding and M&A.

Shoykhet acknowledges that there’s formidable competition in the payments space — not only from incumbents like Venmo, Amazon and PayPal but from buy now, pay later vendors such as Afterpay and Klarna. based electronic money and finance data transfers — increased 8.7% But Shoykhet welcomes the rivalry. currently. .”

Earlier this week, we examined the trends in the major categories of startup investment including eCommerce, Software, Social Networking and Education. In addition, investors will seek under-explored areas to finance, looking for great returns. But which lesser known startup sectors are starting to raise venture dollars?

There are dozens, maybe even hundreds, of companies playing in the cross-border remittances field, from incumbents like Western Union through a myriad of tech players, some of which have gone public and some of which remain privately held.

If you can map every oasis in a desert, you’ve created a transportation network. Today’s investment showcases, if anything, how important Axie’s precedent is to the development of the broader ecosystem – and how willing VCs and crypto incumbents are to bend over backward to make sure it succeeds.”.

“They are the strongest company in the segment and well financed in this growing market,” said Forrester analyst Craig Le Clair. Did UiPath’s valuation get hit by the same shrink ray affecting other software companies, or are other factors at work? H1 2022 cybersecurity product-led growth market map.

Monzo’s culture of customer obsession allowed it to use the crisis to thoughtfully build a beloved consumer and SMB product that has changed personal finance in the UK. 2 Incumbent banks miss the mark in two crucial areas: The banking experience has not evolved to match modern consumer expectations. This did not happen by magic.

Founders : Before beU delivery, Hao Zheng, who leads the team as chief executive, was the founder and CEO of Yooul, a social networking app in China. Founders : Alphas Sinja, Boya’s chief executive officer, has over eight years of experience in the banking and finance sectors. Robert Nyangate is the company’s CTO.

Any area that needs to compete both with incumbents and also a set of already successful “new age” companies that made the first step of meaningful disruption. Fintech (specifically embedded finance or financial SaaS), synthetic bio. Many personal and professional networks are the result of army service.

ETH killers, BTC killers and all kinds of other projects with lofty promises and ambitious roadmaps to build better blockchains than the incumbents. To me, decentralized finance or “DeFi” is the most fascinating part of the cryptocurrency space today. Which means they have paid gas fees and used the Ethereum network.

Narrow Networks — Narrow networks are an interesting response to the above market prices that the large hospitals and groups are pushing on the broader market. Obviously, if narrow networks increase in popularity, more and more market share shifts to providers that are willing to respond to competitive market-based price demands.

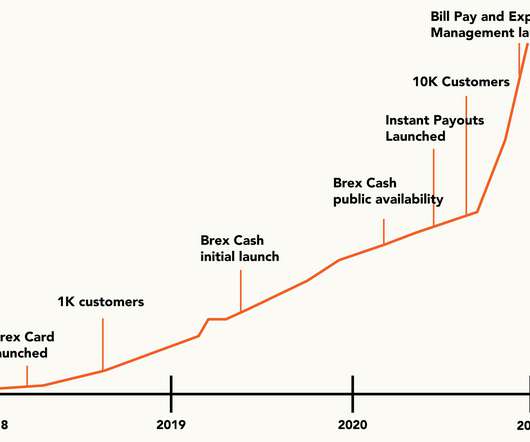

Even with $125K from YC and $1–2M in venture funding, a startup’s credit limit is still likely to tap out at $20K from an incumbent creditor—which is not nearly enough to cover software, marketing, and other expenses. incumbent offerings which only offered end-of-month reconciliation). As Brex has scaled, so have their customers.

But it feels like we have written far less about fintechs that exist solely to help the incumbents better compete with fintechs. The latest financing brings Extend’s total raised since its 2017 inception to $55 million. . We help the incumbents close the gap relative to those players.”. Extend is one such company.

It runs an agent network that uses cash on hand to service customers who can make free deposits and withdrawals and get charged a 1% fee whenever they send money. And despite its continuous squabble with these incumbents due to eating into their market share, Wave claims to serve over 10 million users monthly across its operating markets.

Problems & Ideas: Financing as a service for building electrification Contractor enablement Finding ways (at scale) to add trust as well as ensure accountability Improving the quote lifecycle to reduce time spent (and truck rolls), automate system design, and improve installed system performance. short haul aviation and shipping).

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content