This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

What Alan recognized was that most IRL forums and networking events are absolutely awful places to pitch and here’s why: 1) When a VC shows up in person, they’re looking to replicate the kind of top of the funnel they would get in an hour or two’s worth of e-mail, and that’s not going to happen if you corral them into a corner for 30 minutes.

If you’re pitching a VC, you must do the bare minimum of looking at their website, knowing their previous investments, and learning about the background of the partners you will be pitching. Has the founder done his homework before his pitch?

During Q&A, both sides start engaging in a sort of conversational dance - with one side leading (VC/customer) and the other side following (founder). Most of that time goes to the meat of the conversion: the question-and-answer portion.

Pitchbook estimates that there is about $290 billion of VC “overhang” (money waiting to be deployed into tech startups) in the US alone and that’s up more than 4x in just the past decade. What is a VC To Do? I can’t speak for every VC, obviously. What Does the Post Crash VC Market Look Like? super size or super focus.

Time and time again i hear about founders that have bigger egos then anything else rejecting offers from top tier VC's (like YC ) and eventually leading thier companies to fail. If you do get and offer from top US VC's take them, dont be greedy and stay humble. Dont have a big ego.

I realized a long time ago that the VC’s customer is the founder/CEO/portfolio company and that our investors (called LPs in VC speak) are our “shareholders” That was a very defining moment for me and has clarified what matters the most in a VC firm. That can work too.

Learn how to pass a VC associate screen in under 10 minutes! In this Dreamit Dose, associates Alana Hill and I, Elliot Levy , offer five things we wish founders knew after screening over 1,000 startups in the last year. These are easy tips if you know what to look out for.

Recently, Lightspeeds Mercedes Bent offered founders some reasons why a VC might ghost a founder. It was a perfectly reasonable explanation that basically boiled down to VCs are busy and theres no upside to hurting your feelings or getting into a debate. Never end a VC call without an immediate next step.

A decade or two ago, most of the new funds were traditional VC funds located in technology hubs in the US and a few other countries around the globe. One of the biggest trends we witnessed over the past few years is the rapid pace of new early stage venture fund formation combined with significant growth in the amount of capital invested.

Sometime in the next few weeks, I’ll complete my next investment. It will be the 105th deal out of Brooklyn Bridge Ventures, the firm I started back in September 2012, and it will be the last deal I’ll be making out of my third fund. It will also be my last venture capital deal.

To a VC, $50,000 a pre-sale isn’t really that much. VCs are less interested that you sold 10 customers, 20, or 100—they want to understand how many you’re selling per week and whether or not that kind of pace would be profitable for your sales & marketing efforts.

I cant tell you how many times I got announced as a successful VC when I was introduced on a panel or sat across the room from a potential limited partner telling them I was. This is what I know it feels like for a lot of founders and investors alikefloating in the rarified air of extremely successful people defined by their outcomes.

In Part I of this article we discussed several key concepts of fund investment strategy and how funds are categorized, whether it be by industry, geography, stage, specialty (e.g. social impact, corporate, etc.) or some other criteria. Now let's take a closer look at capital allocation strategy and the life cycle of a venture fund.

I wrote yesterday , about the quarterly numbers for VC investing activity: If this was a student coming home with a report card, it would be straight As. I have not seen the data to back that up but if it is true, that is also a failing grade for the VC sector. It feels like positive change is happening.

As a newly minted manager of a venture fund, your initial response to the question “what are we busy about?” might be, “finding great companies, investing in them and waiting for big financial returns.” And, while your response would be directionally correct, it would be woefully incomplete.

Alicia Castillo Holley is an active angel investor in Silicon Valley and the Founder and CEO of The Wealthing VC Club, a boutique investment group of accredited investors that fills rounds led by VCs. This profile is the eighth in a series of interviews highlighting the work of interesting female investors.

I’m over-paying for every check I write into the VC ecosystem and valuations are being pushed up to absurd levels and many of these valuations and companies won’t hold in the long term. However, to be a great VC you have to hold two conflicting ideas in your head at the same time. Where are Things Headed for VC in 2031?

This is something I talk about a lot with my VC coaching clients. It signals expertise—because the best founders like talking to someone they don’t have to explain remedial things to, let alone someone who at least has an interest in what they’re doing. The question is what to focus on.

The NVCA and Pitch Book are out with their Q3 report on the VC industry and what they report is that the VC industry continues to be very active throughout the pandemic. Deal counts and deal values are stable to up over last year. The massive expansion of later-stage private capital continues unabated. Valuations continue to rise.

In the most recent Pitchbook 2021 predictions , they project that Silicon Valley will make up less than 20% of all VC deals in 2021. If there is one megachange in VC from the pandemic (there may be many), I think it is the comfort with making investments over video without the founder or the VC traveling to meet each other.

Of the first four investments I made as a VC in 2009, two have exited and two (Invoca & GumGum) still are independent and likely to produce $billion++ outcomes . My first ever investment as a VC was Invoca. He then went on the create an early-stage VC that I track closely?—? Maker Studios?—?sold Entrada Ventures? —?that

When you look at the recent Q3 numbers on seed and early-stage VC fundraising, you might think we are in the late stages of a VC bubble: The words I would use to describe the current environment in early-stage VC are “fast and furious.”

There has been this narrative about investing in VC funds that you have to get into the top quartile (25%) or possibly the top decile (10%) in order to generate good returns. I have heard that for as long as I have been in VC and probably have written it here a few times. As you can see, investing in VC funds can be very profitable.

VCs are notorious for kicking tires. VCs take a meeting just to learn about an area. If deal flow is slow, a VC will take a meeting if you and your team seem mildly interesting even if your product isn’t. Some VCs have no money left in their funds, but they still like playing VC. Do you have dry powder for this?

Join Seraf for an engaging and informative webinar on VC investing in BRICS countries, with an emphasis on the exciting opportunities in Brazil. This event is tailored for venture capitalists, startup founders, and investors eager to delve into the high-growth potential within Brazil's dynamic market.

Between 2006–2008 I sold both companies that I had started and became a VC. SEEING THINGS FROM THE VC SIDE OF THE TABLE While I was a VC in 2007 & 2008 those were dead years because the market again evaporated due the the Global Financial Crisis (GFC). THE VC VALUATION GOD Valuation obsession wasn’t restricted to startups.

In almost twenty years of producing some of the highest performing VC funds in the business, USV has never had a portfolio company become worth over $100 billion. The exit values in VC have increased significantly over the last decade leading to escalating entry values. So it can happen, but it is very unlikely. That makes sense.

I remember about fifteen years ago, a well-known VC said to me “you need to sell a company within a few years of the founder leaving. ” I told that VC that my experience has been different on that measure and that I did not agree. Companies can’t sustain their innovation after a founder leaves.”

In this case, a VC would have every right, having seen lots of products get built and succeed or fail, to want to observe and discuss that process. What’s harder to notice for a founder is all of the things that a founder isn’t being asked to review in detail that a VC has no problem trusting the founder on.

If you’re a VC raising your first fund, and you think you fit either of these descriptions, please let us know. And how quickly the firm can process new information and adjust if portions of their hypothesis need tuning once in market. But we’re interested in taking this risk when the person and opportunity warrants it.

Syndication allows multiple investors -- whether they be individuals, angel groups, VC funds, etc. -- to join together and provide the funding resources needed by one company. Syndication has been a common practice amongst VC firms for decades. A very common practice in the investment world is syndication.

That all being said, new VC markets are emerging—and during the pandemic, lots of New Yorkers and folks from the Valley decamped to Miami or Austin. I know of one deal where the significant other of a VC was the head of a staunchly anti-LGBTQ+ lobbying organization—and the investor was offering money to a gay founder. Plenty of bros.

That’s what every VC is telling their portfolio companies these days. If you don’t realize that, just imagine you’re a VC fund with some dry powder in the second half of 2023. The one question every VC needs to be able to answer on the way to getting to a “yes” is, “Can this return a big chunk of my fund one day?”

million in Series A funding led by Unusu al VC , with participation from Wing VC, Founder Collective, XFund, Alt Capital, Lauryn Motamedi, David Rogier, and JD Ross. The startup has been embraced by marketing agencies and in-house teams who are now building AI-growth as a core competency.

A well-known entrepreneur turned VC, who will go unnamed because I am not sure he would want me to share this conversation publicly, once told me “if you remove a founder, you must sell the company within a couple of years or it will start to decline in value.”

VC firms are not blameless — over 1.8K VC investors wrote checks into proptech deals over the last five years. These strategics have fundamentally different models and objectives for investing in proptech startups compared to a VC that is focused on generating returns through scaling tech companies.

So I saw this tweet by Semil Shah yesterday: A friend who works in an industry far from tech startups & VC asked what would be the single article I’d share to read on each topic. It is about how a VC can compete and win a deal that many others want. That is a failure of the system. But this post is not about that.

As I wrote then: I don’t think a VC firm should manage to a pacing number. In the last two years, the VC business has been operating at a blistering pace, the fastest I’ve witnessed in my 35 years in the business (including the 99/00 era). But even so, the VC business has turned into a sprint.

So today, I will write about 2020 in the context of tech/startups/VC/crypto. So when we look back at 2020 in a few years, we will see that it was the year that everything changed for tech/startups/VC/crypto and set the stage for a decade of transformational change. And god knows that the world needs a lot of that right now.

Does the VC think that a designer needs to be on the team from day one if you’re going to build a better version of Instagram? Does the VC think that a machine learning engineer needs to be there to build a real version of Tony Stark’s Jarvis? That’s fair. Let’s first talk about the definition of a co-founder.

I saw Dan Primack assert that the venture capitalist’s customer is their limited partners in this tweet about the Citizen app, the recap, and their VCs: Regular reminder that, ultimately, VC funds works for their limited partners, not for their portfolio companies. link] I encourage everyone to read that post. USV TEAM POSTS:

But VC bubbles deflate slowly. Building a generational company from scratch is the hardest thing you can do in capitalism. It’s not, or at least it shouldn’t be, a YOLO lark with other people’s money. With private markups hard to come by and liquidity drying up, it can take years for LPs to figure out the J curve is actually an L curve.

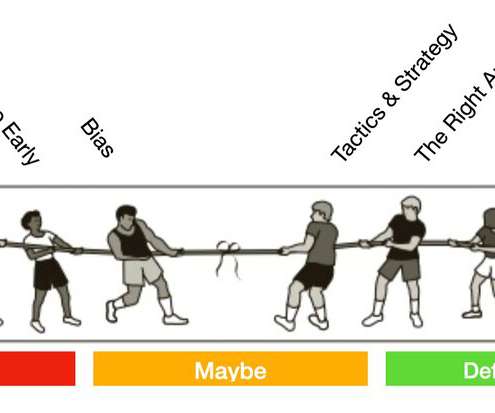

Any VC will tell you that the ones they said yes to, they mostly got there right away—and that there are very few “maybe” deals that get tipped over the fence. Here’s the way I look at the math: Let’s go over the structural bias first—the “pipeline” that happens before you ever even get near a VC. First is network bias.

At the time, restaurants and food tech were on the margins of most investors’ minds and there was skepticism around VC-backed food concepts. When Revolution Growth first invested in Sweetgreen in 2013, the whisperings of food and wellness were present but sparse, and the bulk of lunchtime options focused more on convenience than ingredients.

We organize all of the trending information in your field so you don't have to. Join 24,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content